Illinois Realtors: How to Close More Deals When Affordability Constrains Buyers

Current Date: March 25, 2026

The Illinois housing market is currently navigating a period of significant recalibration. As of late March 2026, mortgage rates have climbed back above the 6.1% threshold, creating what many industry experts call an "affordability cliff." For Realtors in Chicago and across the state, this shift often translates to hesitant buyers, stalled pipelines, and deals that fall apart at the finish line due to debt to income (DTI) ratios.

Navigating this environment requires more than just showing properties; it requires a sophisticated mortgage strategy. When the cost of borrowing increases, the traditional approach to financing often fails to meet the needs of modern buyers and investors. To maintain transaction volume, real estate professionals must pivot from viewing mortgages as a commodity to utilizing them as a strategic tool to bridge the gap between price and monthly affordability.

According to recent data from Redfin, while sales volume has shown signs of improvement, the rise in rates remains a primary headwind for many households. This is where the partnership between a Realtor and a Mortgage Strategist becomes the deciding factor in whether a deal closes or collapses.

Understanding the Affordability Cliff in Illinois

The term "affordability cliff" refers to the point where incremental increases in interest rates push the monthly mortgage payment beyond the qualifying limit for a borrower. In markets like Chicago, where property taxes and insurance costs are already substantial, even a 0.25% move in rates can disqualify a buyer who was previously pre-approved.

Explore how these market shifts impact different segments:

- First-Time Homeowners: Frequently operate on thin margins where a $100 increase in monthly payment ends the search.

- Move-Up Buyers: Often hesitate to trade their current low-rate mortgage for a 6% plus rate, leading to "listing paralysis."

- Real Estate Investors: Analyze deals based on cash flow; higher rates compress margins, making many traditional properties non-viable without creative financing.

To solve these challenges, we must look beyond the base interest rate and focus on the net monthly obligation and the total cash-to-close.

Visual: A realistic street view of a Chicago neighborhood featuring a mix of renovated brick two-flats and modern infill housing. Ebonie Beaco - Mortgage Strategist

Visual: A realistic street view of a Chicago neighborhood featuring a mix of renovated brick two-flats and modern infill housing. Ebonie Beaco - Mortgage Strategist

Strategic Tool: The Interest Rate Buy-down

Temporary Buy-down: A financing technique where a lump sum is paid at closing to reduce the borrower's interest rate for the first one to three years of the loan.

- Application: Use a 2-1 or 3-2-1 buy-down to help a buyer "ease into" their mortgage payment while they wait for potential future refinancing opportunities.

For Illinois Realtors, the 2-1 buy-down is a deal-saver. In this scenario, the seller pays a subsidy that lowers the buyer's interest rate by 2% in the first year and 1% in the second year. By year three, the rate returns to the original note rate.

This strategy is particularly effective for Wholesalers and Real Estate Investors who need to move inventory quickly. Instead of a price reduction, which may not significantly impact the buyer's monthly payment, a seller-funded buy-down provides immediate relief and helps the buyer qualify more easily.

Strategic Tool: Lender Credits and Closing Cost Offset

Lender Credit: A credit provided by the mortgage lender to the borrower to cover closing costs, usually in exchange for a slightly higher interest rate.

- Application: Ideal for buyers who have the income to support a higher payment but are short on the liquid cash required to close the deal.

In a market where buyers are squeezed, a Mortgage Strategist can structure a loan with a lender credit to offset the high cost of Illinois transfer taxes or title fees. This keeps more cash in the buyer’s pocket for immediate repairs or furniture, making the purchase feel more attainable despite the higher rate environment.

Leveraging DSCR Loans for Investors and Wholesalers

DSCR (Debt Service Coverage Ratio) Loan: A mortgage product for investment properties that qualifies the borrower based on the property’s rental income rather than their personal income or tax returns.

- Application: Used by investors to scale portfolios quickly without being hindered by personal DTI limits.

For Real Estate Investors and Wholesalers in Illinois, Georgia, and Florida, DSCR loans are essential. When traditional financing is restricted by high rates and strict DTI requirements, DSCR focuses on the asset. If the property’s projected lease income covers the debt service (Principal, Interest, Taxes, Insurance, and Association fees), the loan can move forward.

Analyze the benefits of DSCR in a high-rate market:

- No Employment Verification: Speeds up the closing process for busy investors.

- Scalability: Investors can hold multiple properties under different LLCs without personal income constraints.

- Wholesaler Advantage: Providing a buyer with a pre-vetted DSCR financing option makes a wholesale deal much more attractive.

Practical Example: The Math of a Deal-Saver Strategy

To understand the impact of these strategies, let’s look at a typical Chicago purchase scenario.

Scenario Details:

- Purchase Price: $450,000

- Down Payment (20%): $90,000

- Loan Amount: $360,000

- Market Interest Rate: 6.5%

- Principal & Interest Payment: $2,275

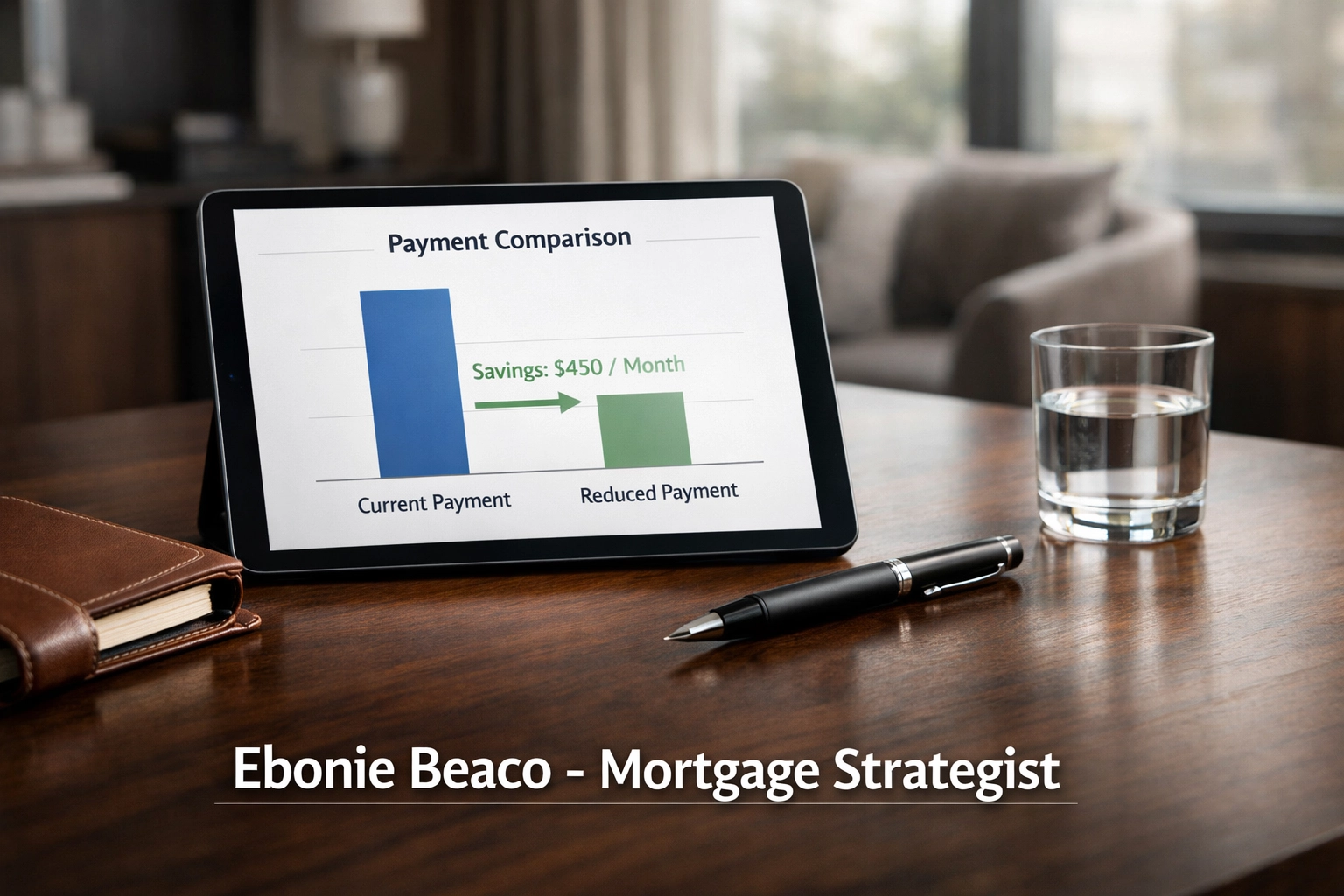

If the buyer is capped at a $2,000 P&I payment due to DTI, this deal is dead at market rates. However, by implementing a 2-1 Buy-down funded by a $8,500 seller concession, the numbers change:

- Year 1 Rate (4.5%): Payment is $1,824 (Savings of $451/month)

- Year 2 Rate (5.5%): Payment is $2,044 (Savings of $231/month)

- Year 3+ Rate (6.5%): Payment is $2,275

By year three, the buyer’s income has likely increased, or they have had the opportunity to execute a home refinance if rates have dipped. This strategy allows the Realtor to close the deal today rather than waiting for a market shift that may not come.

Visual: A financial table showing the year-over-year payment breakdown of a 2-1 buy-down on a $450,000 home, highlighting the monthly savings for the buyer. Ebonie Beaco - Mortgage Strategist

Visual: A financial table showing the year-over-year payment breakdown of a 2-1 buy-down on a $450,000 home, highlighting the monthly savings for the buyer. Ebonie Beaco - Mortgage Strategist

Solutions for Self-Employed Buyers: Bank Statement Loans

Many potential homeowners in Illinois and Michigan are self-employed entrepreneurs or "1099" contractors. Standard mortgage guidelines often require two years of tax returns, which may show significant deductions, lowering the "taxable income" used for qualification.

Bank Statement Loan: A non-QM (Non-Qualified Mortgage) program that uses the average monthly deposits from 12 or 24 months of bank statements to calculate qualifying income.

- Application: Perfect for business owners who have strong cash flow but low taxable income due to legal business write-offs.

Jump in and help your self-employed clients by suggesting a Mortgage Strategist who understands non-QM mortgage loans. This opens up the buyer pool to a massive segment of the population that is currently being underserved by traditional big-box banks.

The Importance of the Consultation

As a Realtor, your time is your most valuable asset. Spending weeks showing homes to a buyer who cannot qualify under current rate conditions is a drain on your resources. This is why the loan process must begin with a deep-dive strategy session.

A true Mortgage Strategist does more than run a credit report. We analyze the following:

- Asset Liquidity: Can we use a HELOC on a current property to fund the down payment?

- Exit Strategies: If the buyer is an investor, what is the plan for a cash-out refinance after the property is stabilized?

- Tax Efficiency: For landlords, how do different loan structures impact their annual tax liability?

By partnering with an expert who understands the nuances of the Illinois, Indiana, and Virginia markets, you ensure that every lead is thoroughly vetted and matched with the right financial product.

Managing the "Wait and See" Mentality

Many homeowners in Missouri and Kentucky are currently sitting on the sidelines, waiting for rates to return to 3% or 4%. As a professional, it is our job to provide the clarity they need to make a move.

Historically, waiting for lower rates often leads to higher home prices as competition increases. If a buyer waits for a 1% drop in rates but the home price increases by 10% during that wait, they have actually lost purchasing power.

Compare the "Buy Now" vs. "Wait" scenario:

- Buy Now: Secure the home at today’s price, utilize a buy-down for immediate affordability, and refinance when rates drop.

- Wait: Face increased competition, higher bidding wars, and potentially higher entry prices that offset any savings from a lower interest rate.

Access our mortgage calculators to show your clients the real-time cost of waiting. Being the voice of reason in a volatile market establishes you as an authority and builds long-term trust with your clients.

Expanding Your Reach: Multi-State Strategy

While Illinois is a core focus, many investors today are looking across state lines for better cap rates or lower entry points. Whether your clients are looking at rental properties in Alabama, fix-and-flip opportunities in Arkansas, or short-term rentals in Florida, having a consistent financing partner is vital.

We provide expert guidance and funding solutions across:

- Alabama & Arkansas: Growing markets for affordable rental portfolios.

- Georgia & Florida: Hotbeds for Airbnb and short-term rental financing.

- Michigan, Indiana, & Kentucky: Strong cash-flow markets for mid-range investors.

- Virginia & Missouri: Diverse economies with stable residential growth.

Visual: A realistic image of a professional workspace with multiple monitors displaying market trends and property maps across several US states. Ebonie Beaco - Mortgage Strategist

Visual: A realistic image of a professional workspace with multiple monitors displaying market trends and property maps across several US states. Ebonie Beaco - Mortgage Strategist

Conclusion: Becoming the Solution

In a market constrained by affordability, the "order taker" loan officer is a liability to your business. To close more deals, you need a Mortgage Strategist who can engineer solutions when the standard "P&I" doesn't fit the buyer's budget.

Whether it’s utilizing DSCR for an investor, a bank statement loan for a business owner, or a strategic buy-down for a first-time buyer, the goal remains the same: helping your clients achieve their real estate goals while ensuring your pipeline continues to move forward.

If you have a deal that is struggling to cross the finish line, or if you want to arm your buyers with more powerful financing options, let’s connect.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664