How to Unlock Cash in 11 States Without Touching Your Current Mortgage Rate

If you are like most homeowners who bought or refinanced a few years ago, you are probably sitting on a goldmine. You have likely seen your property value skyrocket while you enjoy a mortgage rate somewhere in the 2% or 3% range. It feels great until you realize you need cash for a renovation, a new investment property, or to consolidate some high interest debt.

The traditional move was a cash-out refinance. But in 2026, trading a 3% rate for a 6% or 7% rate just to get some cash out feels like a financial step backward. It is the ultimate interest rate trap. You want your equity, but you do not want to lose your low monthly payment.

Fortunately, there is a way to tap into that wealth without touching your primary mortgage. If you live in Alabama, Arkansas, California, Florida, Georgia, Illinois, Indiana, Kentucky, Michigan, Missouri, or Virginia, you have access to a strategy that keeps your low rate intact.

The Secret Home Equity Drain You Might Be Overlooking

Many homeowners assume that their equity is "locked" unless they sell the house or refinance the whole thing. This misconception acts as a drain on your potential wealth. When your money sits idle in the walls of your home, it is not working for you.

For real estate investors and savvy homeowners, idle equity is an opportunity cost. You could be using that capital to fund a DSCR rental property or to execute a BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat). By leaving the equity untouched, you are essentially letting your most significant asset sit on the sidelines of the market.

Accessing this cash is not about spending more; it is about moving your wealth from an illiquid state into a liquid one. Whether you are looking for a California HELOC to fund a backyard ADU or a Florida HELOC to put a down payment on a vacation rental, the goal is the same: liquidity without sacrifice.

Defining the HELOC: Your Secondary Wealth Tool

Before we jump in, let's define the primary tool used for this strategy.

HELOC (Home Equity Line of Credit) Definition: A revolving line of credit secured by your home that allows you to borrow against your equity as needed. Practical Application: You can draw funds, pay them back, and draw them again, similar to a credit card but with much lower interest rates and higher limits.

CLTV (Combined Loan-to-Value) Definition: The ratio of all loans on a property compared to its total appraised value. Practical Application: Lenders use this to determine how much total debt they will allow on your home, which dictates your maximum HELOC limit.

Draw Period Definition: The initial phase of a HELOC where you can withdraw funds and typically make interest-only payments. Practical Application: This provides maximum flexibility for investors who need short-term cash for renovations or down payments.

Why a HELOC Beats a Cash-Out Refinance Right Now

Compare your options clearly. A cash-out refinance replaces your entire first mortgage. If you owe $300,000 at 3% and want $50,000 in cash, you end up with a new $350,000 loan at current market rates. Your monthly payment on the original $300,000 jumps significantly.

A HELOC is a "second lien." It sits behind your first mortgage. Your $300,000 loan stays at 3%. You only pay the current market interest rate on the $50,000 you actually borrow. This surgical approach to borrowing saves you thousands of dollars in interest every year.

Explore the Home Refinance page to see how these structures differ in detail.

Regional Opportunities: From Chicago to the California Coast

The 11 states we serve: AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, VA: each offer unique reasons to tap into equity today.

The Georgia HELOC Lender Perspective

In markets like Atlanta and Savannah, property values have maintained strong momentum. A Georgia HELOC lender can help you leverage that growth to pivot into the rental market. Many investors in Georgia are using equity to fund DSCR investor loans for suburban single-family homes.

California HELOC Strategies

California homeowners often have the largest "equity stacks" in the country. If your home in San Diego or San Jose has increased by $400,000 since you bought it, a HELOC allows you to access a portion of that for an investment elsewhere without giving up your low-rate primary mortgage. This is a common move for those looking into Jumbo Loans for secondary residences.

Florida and the Short-Term Rental Boom

In Florida, homeowners are tapping equity to fund Airbnb and short-term rental financing. The cash from a HELOC provides the "skin in the game" needed to secure financing for a beachside condo or a Disney-area rental.

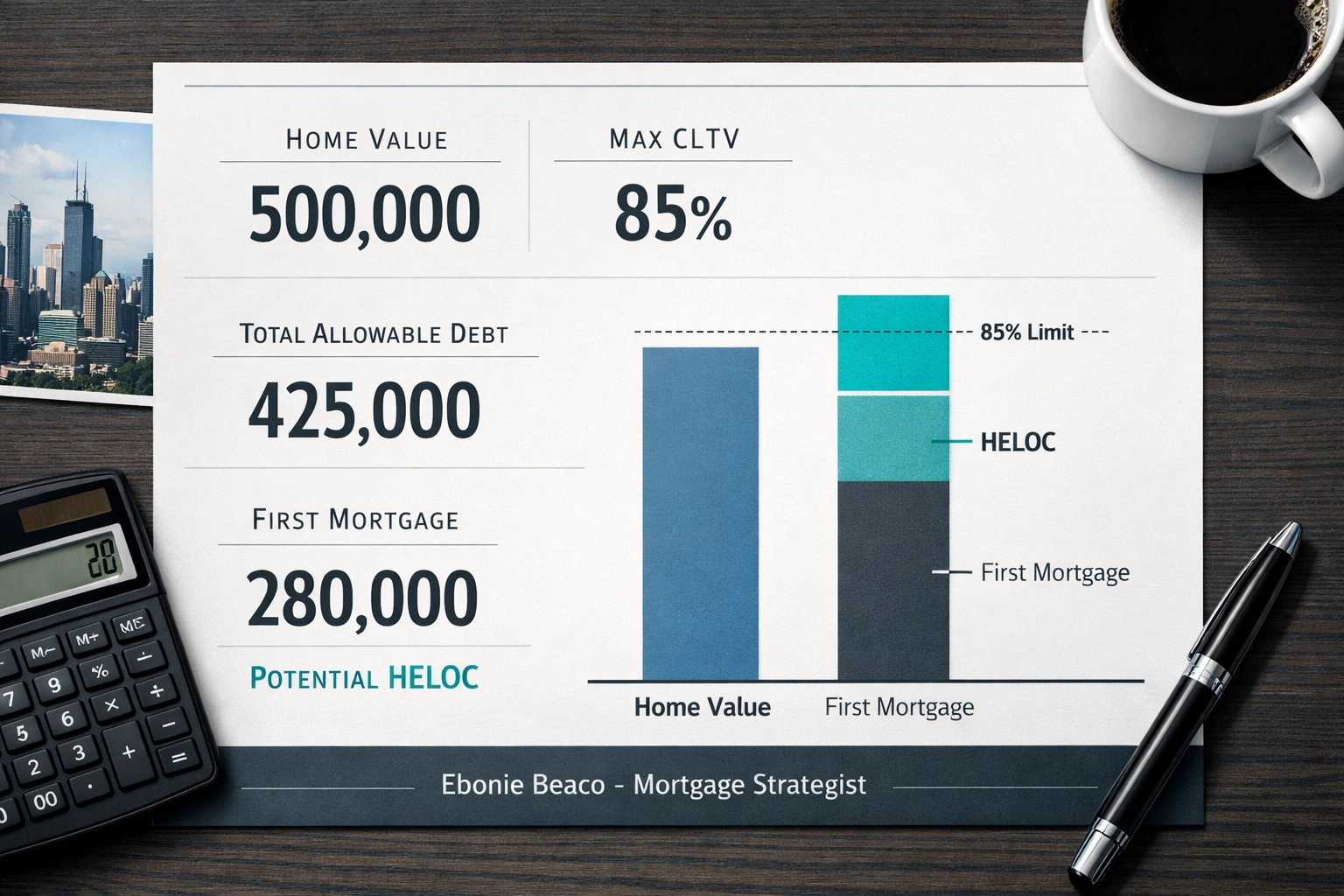

Calculating Your Potential: A Real-World Scenario

Let’s look at how the math works for a homeowner in Chicago or Northern Virginia.

The Scenario:

- Current Home Value: $500,000

- Existing First Mortgage (at 3.25%): $280,000

- Max CLTV allowed by lender: 85%

The Calculation:

- Total allowable debt: $500,000 x 0.85 = $425,000

- Current debt: $280,000

- Available HELOC Limit: $425,000 - $280,000 = $145,000

In this example, the homeowner accesses $145,000 in liquid cash. Their original $280,000 mortgage remains completely untouched. They only pay interest on the portion of the $145,000 they actually spend.

How Investors Use HELOCs to Scale

If you are an investor, a HELOC is more than a safety net; it is a springboard. Here is how professional investors in states like Michigan and Missouri are using these lines of credit:

- Bridge Loans: Use the HELOC to buy a distressed property for cash, renovate it, and then refinance it into a long-term DSCR loan.

- Down Payments: Use the HELOC to cover the 20% or 25% down payment on a new rental property.

- Renovation Costs: Fund a "fix and flip" project in Indiana or Arkansas without taking out high-interest hard money loans.

By using your existing home as the collateral, you often get much better terms than a traditional business line of credit. You can jump in on a deal quickly because the funds are already available in your account.

Review our Loan Process to see how quickly you can get a line of credit established.

Transparency: What You Need to Know

At Home Loans Network, we believe in being transparent about the risks and costs.

- Variable Rates: Most HELOCs have variable interest rates. If market rates go up, your HELOC payment will go up.

- Appraisals: You will likely need a new appraisal to confirm your home's current value.

- Costs: While usually lower than a refinance, there are still closing costs and sometimes annual fees associated with a line of credit.

It is vital to compare these costs against the potential return on investment if you are using the money for real estate. Access the Mortgage Calculators to run your own numbers and see if the math adds up for your specific situation.

Taking the Next Step in Your 11-State Search

Whether you are looking for a Florida HELOC to renovate your kitchen or a Georgia HELOC lender to help start your real estate empire, the process begins with an assessment of your current equity.

We serve homeowners across:

- Alabama and Arkansas

- California and Florida

- Georgia and Virginia

- Illinois (including Chicago) and Indiana

- Kentucky, Michigan, and Missouri

The equity in your home is a powerful financial tool. It is your money; it is time you had access to it without being penalized by losing your record-low interest rate.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

If you are ready to stop letting your equity sit idle and start putting it to work, jump in and explore your options today.

But wait... accessing the cash is only the first step. The real secret isn't just how you get the money: it's how you use it to create a tax-advantaged income stream that could eventually pay off your entire mortgage for you. Are you ready to learn the "Equity Loop" strategy? That is a conversation for our next session.