How to Qualify for a Mortgage Using Your Bank Statements

For many self-employed entrepreneurs and freelancers in places like Chicago, Atlanta, or the coastal cities of California, tax season is a time of celebration and strategy. You work hard to maximize your deductions, effectively lowering your taxable income. While this strategy is fantastic for your bottom line, it often creates a significant hurdle when you decide to purchase a home or invest in real estate. Traditional lenders typically look at the "bottom line" on your tax returns, which might not reflect your true purchasing power.

This is where the bank statement mortgage becomes a powerful tool. Instead of focusing on your tax returns, these loans look at the actual cash flowing through your business or personal bank accounts. This approach provides a transparent view of your ability to repay a loan without penalizing you for being a savvy business owner.

Understanding the Bank Statement Loan

A bank statement loan is a type of Non-QM (Non-Qualified Mortgage) program designed specifically for individuals who don't have a traditional W-2 income. This includes small business owners, independent contractors, consultants, and real estate investors who may have complex income structures.

In states like Florida and Virginia, where the entrepreneurial spirit is high, these loans allow borrowers to qualify based on their gross deposits rather than their net income after expenses. This program recognizes that business expenses are often non-cash or one-time events that shouldn't necessarily limit your ability to secure housing.

Explore the mortgage basics to see how different loan types compare to traditional financing.

How Lenders Calculate Your Qualifying Income

The process of determining how much you can borrow is straightforward but requires a specific set of eyes. Lenders typically review either 12 or 24 months of consecutive bank statements. They aren't looking for a specific "profit" number in the traditional sense; they are looking for consistent cash flow.

To calculate your qualifying income, a lender will:

- Total all eligible deposits over the 12 or 24-month period.

- Exclude transfers between accounts, tax refunds, or large one-time personal gifts.

- Calculate the monthly average of these deposits.

- Apply an "expense factor" to account for the costs of running your business.

The expense factor is a standard percentage used to estimate your business overhead. While this varies, 50% is a common benchmark used by many lenders. If your business has very low overhead: like a consultant working from a home office in Michigan: your lender might allow for a lower expense factor with a letter from a CPA.

Real-World Income Calculation Example

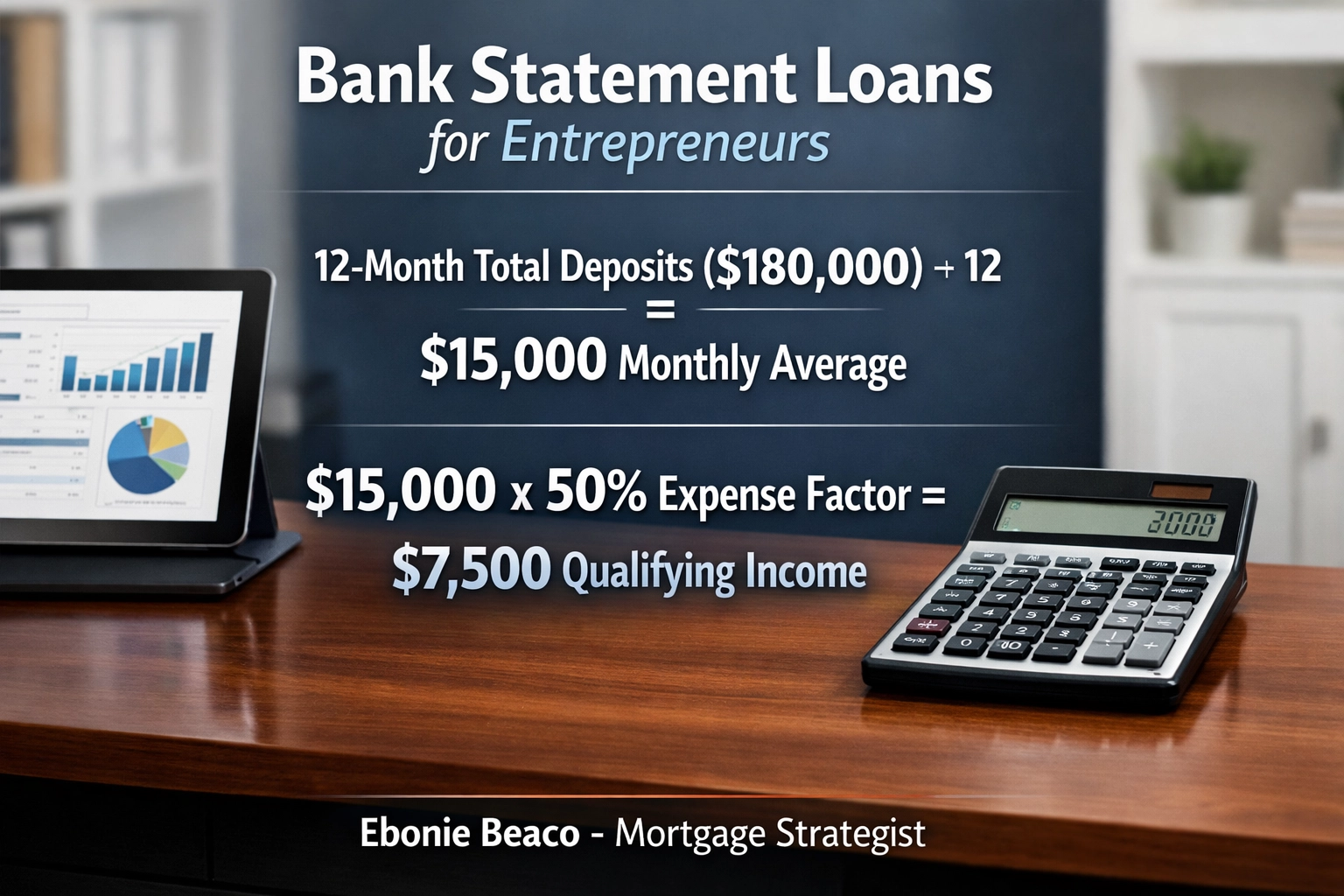

Let’s look at a freelance graphic designer in Indiana who wants to buy a home. Over the last 12 months, their business bank statements show a total of $180,000 in deposits from various clients.

Total Annual Deposits: $180,000 Monthly Average Deposits: $15,000 ($180,000 / 12) Standard Expense Factor (50%): $7,500 Qualifying Monthly Income: $7,500

By using this method, the designer qualifies with a monthly income of $7,500, even if their tax returns show a much lower figure due to equipment depreciation and home office deductions.

Image Instructions: Create a professional financial infographic titled "Bank Statement Loans for Entrepreneurs". Display the following calculation: 12-Month Total Deposits ($180,000) ÷ 12 = $15,000 Monthly Average. $15,000 x 50% Expense Factor = $7,500 Qualifying Income. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. Ensure no images of money or cash are present.

Image Instructions: Create a professional financial infographic titled "Bank Statement Loans for Entrepreneurs". Display the following calculation: 12-Month Total Deposits ($180,000) ÷ 12 = $15,000 Monthly Average. $15,000 x 50% Expense Factor = $7,500 Qualifying Income. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. Ensure no images of money or cash are present.

Core Requirements for Self-Employed Borrowers

While bank statement loans offer flexibility, they still maintain high standards to ensure financial stability. If you are looking to purchase property in Alabama or Arkansas, you should prepare for the following criteria:

Self-Employment History You generally need to show that you have been self-employed in the same industry for at least two years. This demonstrates the stability of your income stream.

Credit Score Thresholds While traditional loans might allow lower scores, bank statement programs often start at a 620 minimum, though a score above 680 will typically secure more favorable interest rates.

Down Payment Expectations Because these loans carry a slightly higher risk for the lender, the down payment requirements are usually higher than an FHA loan. You should expect to put down between 10% and 25%, depending on your credit profile and the property type.

Debt-to-Income (DTI) Ratio Lenders generally look for a DTI ratio between 45% and 50%. This means your total monthly debt payments (including your new mortgage) should not exceed half of your qualifying monthly income.

You can use our mortgage calculators to estimate how your DTI might look based on different purchase prices.

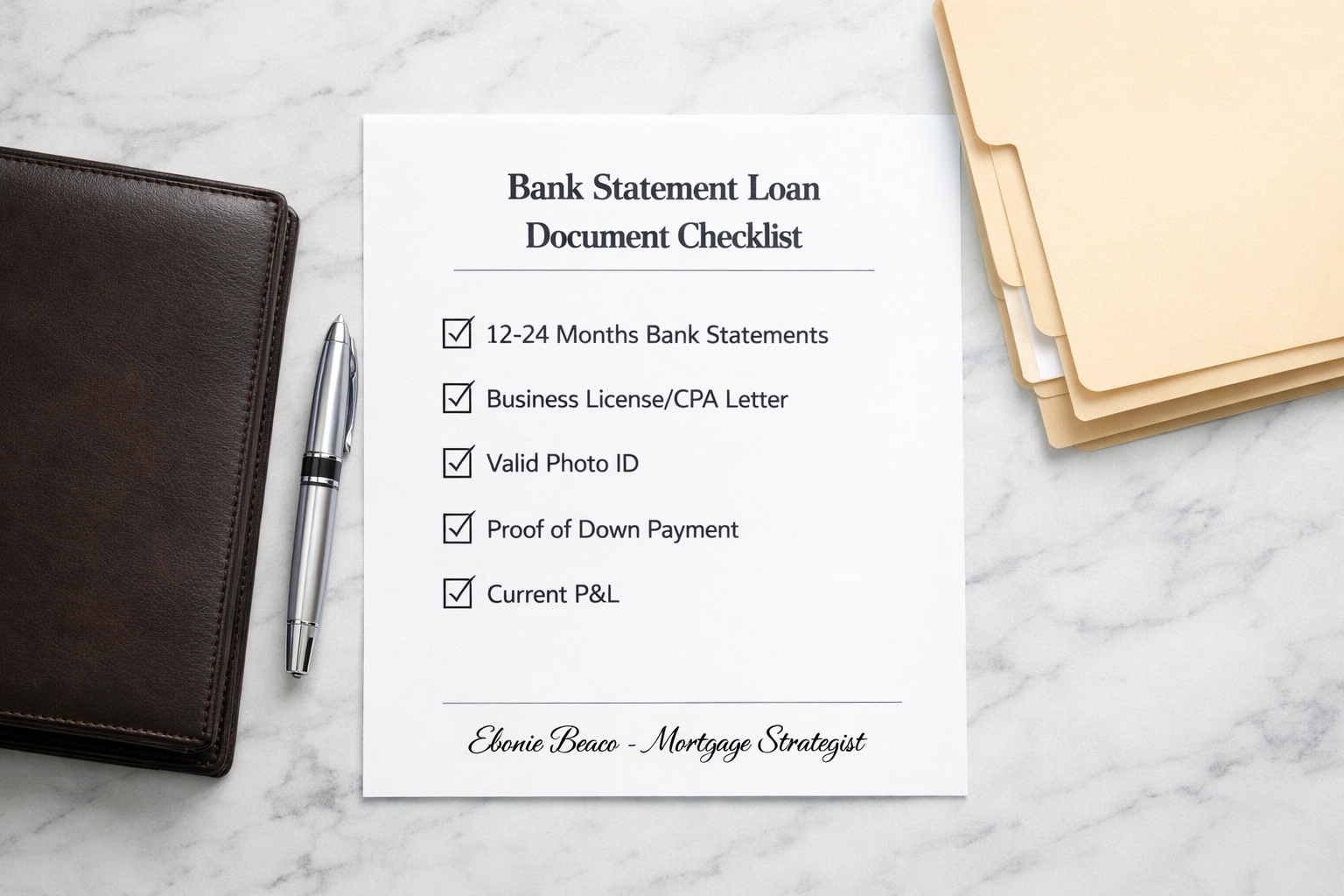

Documentation You Will Need

Transitioning from a "paperwork-heavy" traditional loan doesn't mean there is no documentation. It just means the type of documentation changes. To keep the process moving quickly, have these items ready:

- 12 or 24 Months of Statements: Provide every single page of your consecutive bank statements. No gaps are allowed.

- Business Verification: A business license, articles of incorporation, or a letter from your CPA confirming you have been in business for the required time.

- Proof of Assets: Documentation showing you have the funds for a down payment and closing costs.

- Photo ID: A valid government-issued ID.

- Profit and Loss (P&L) Statement: While not always required for every program, having a current P&L can help clarify your business health to the underwriter.

Image Instructions: Create a clean checklist graphic titled "Bank Statement Loan Document Checklist". List: 12-24 Months Bank Statements, Business License/CPA Letter, Valid Photo ID, Proof of Down Payment, and Current P&L. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. No money or cash icons.

Image Instructions: Create a clean checklist graphic titled "Bank Statement Loan Document Checklist". List: 12-24 Months Bank Statements, Business License/CPA Letter, Valid Photo ID, Proof of Down Payment, and Current P&L. Add "Ebonie Beaco - Mortgage Loan Officer" at the bottom. No money or cash icons.

Why This Strategy Works for Real Estate Investors

Investors often hit a "wall" with traditional financing after they acquire a few properties. Tax returns begin to look complicated with various depreciations and rental expenses. For an investor in Kentucky or Missouri looking to scale their portfolio, bank statement loans provide a path forward.

By focusing on the cash flow of the business or the personal accounts, investors can continue to acquire properties without being limited by the net income shown on their IRS filings. This is particularly useful for those utilizing the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat) or those managing a fleet of short-term rentals in vacation markets like Florida.

If you are an investor, you might also want to compare this to DSCR investor loans which focus entirely on the property's income rather than your personal or business bank statements.

What Lenders Look for in Your Statements

Underwriters will do a deep dive into your banking habits. They aren't just looking at the total deposit amount; they are looking for signs of a healthy financial life.

Consistent Balances Lenders prefer to see that your account balance doesn't frequently dip to zero. Maintaining a "cushion" shows that you can handle the unexpected costs of homeownership.

Overdraft History Frequent non-sufficient funds (NSF) charges can be a red flag. If you have occasional overdrafts, be prepared to provide a written explanation of why they occurred.

Stable Deposits While some seasonality is expected in business, wild swings in monthly deposits can lead to more questions. If your business is seasonal: perhaps a landscaping company in Illinois: providing 24 months of statements instead of 12 can help show a more accurate annual average.

Access our loan process page to understand how we move from statement review to the closing table.

Taking the Next Step in Your Entrepreneurial Journey

Qualifying for a mortgage shouldn't feel like a battle against your own business success. The bank statement loan recognizes the reality of modern entrepreneurship and provides a transparent, fair way to evaluate your financial strength. Whether you are buying a primary residence in Georgia or adding to your investment portfolio in California, using your cash flow as proof of income is a smart, strategic move.

If you are ready to stop letting tax returns dictate your housing options, it is time to look at your bank statements as the asset they truly are.

Ready to use your bank statements to buy a home? Contact Ebonie Beaco for mortgage financing or mentoring.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664