How to Navigate Wholesaling Logistics: From Contract Signatures to the Closing Table

Real estate wholesaling is often described as the "entry point" for new investors because it requires little of your own capital.

However, the difference between a successful deal and a legal headache lies entirely in the logistics of your paperwork.

You are not just selling a house; you are selling a legal right to a contract.

Navigating the path from a signed purchase agreement to receiving your assignment fee requires a clear understanding of contracts, local laws in states like California and Florida, and the specific closing customs in markets like Atlanta.

Defining the Wholesaling Toolkit

To move with confidence, you must understand the technical language used at the closing table.

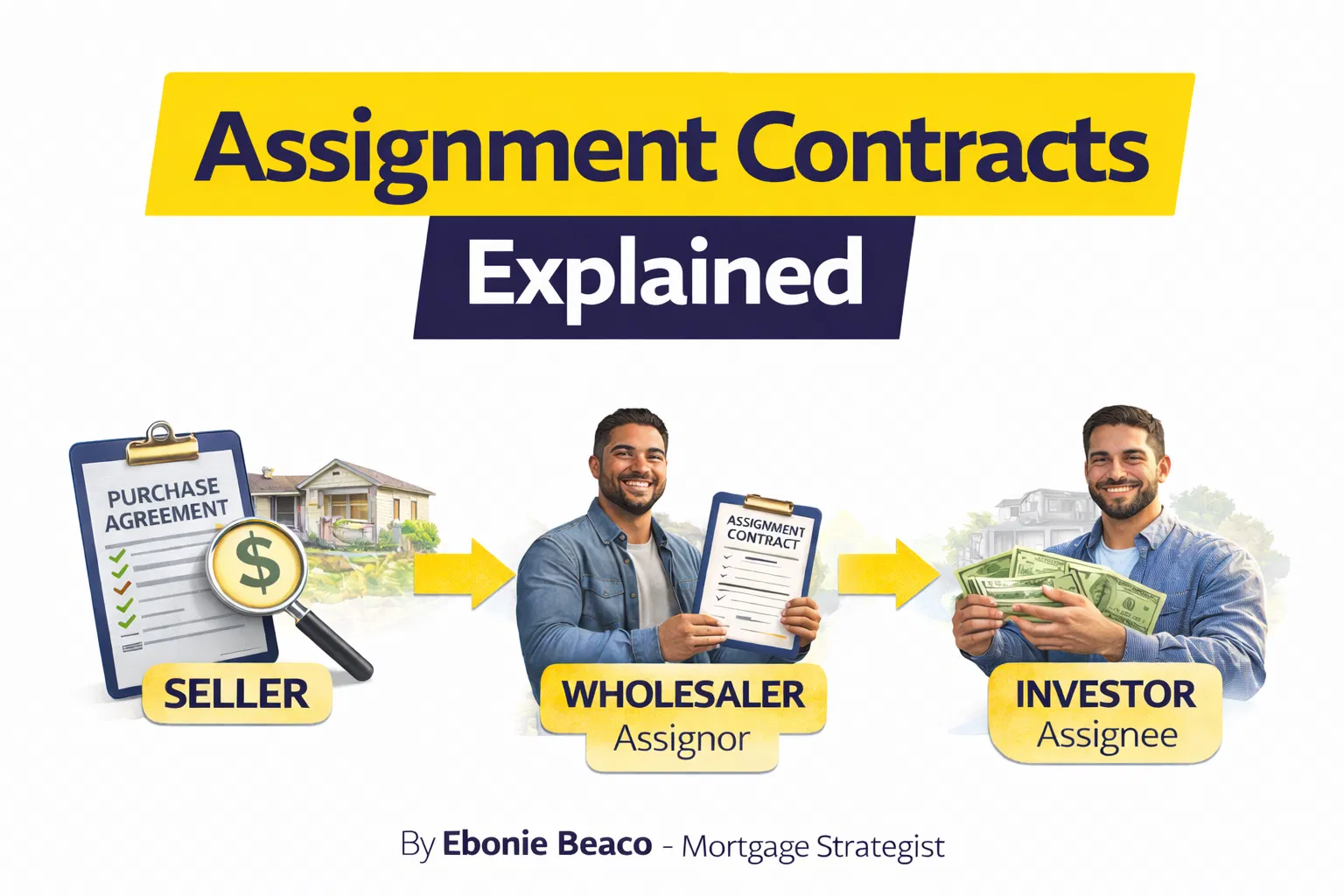

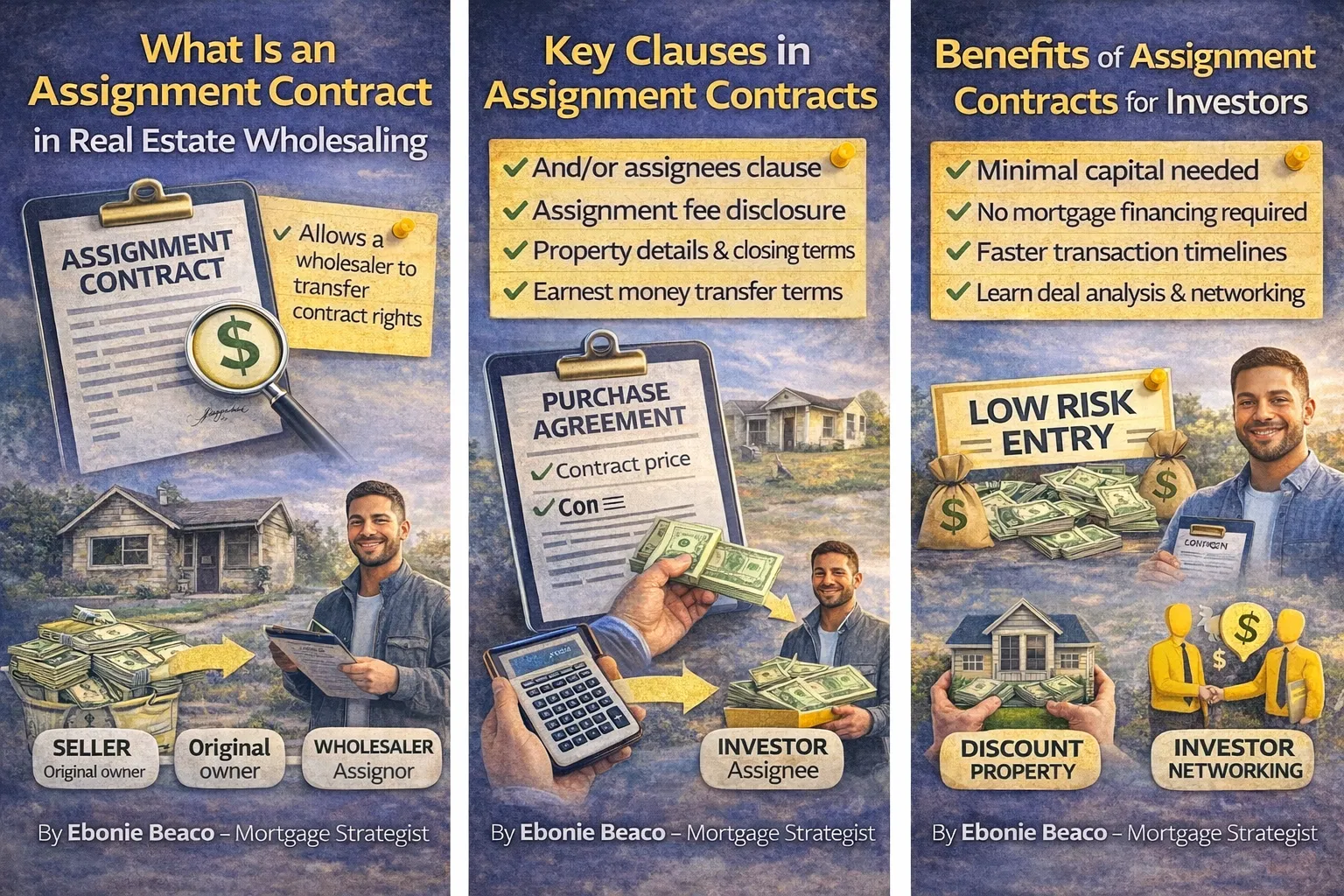

Wholesale Real Estate Contract: A legally binding agreement between a seller and a wholesaler to purchase a property at a specific price within a set timeframe. Practical application: This document gives you "equitable interest" in the property, allowing you to market it to other buyers.

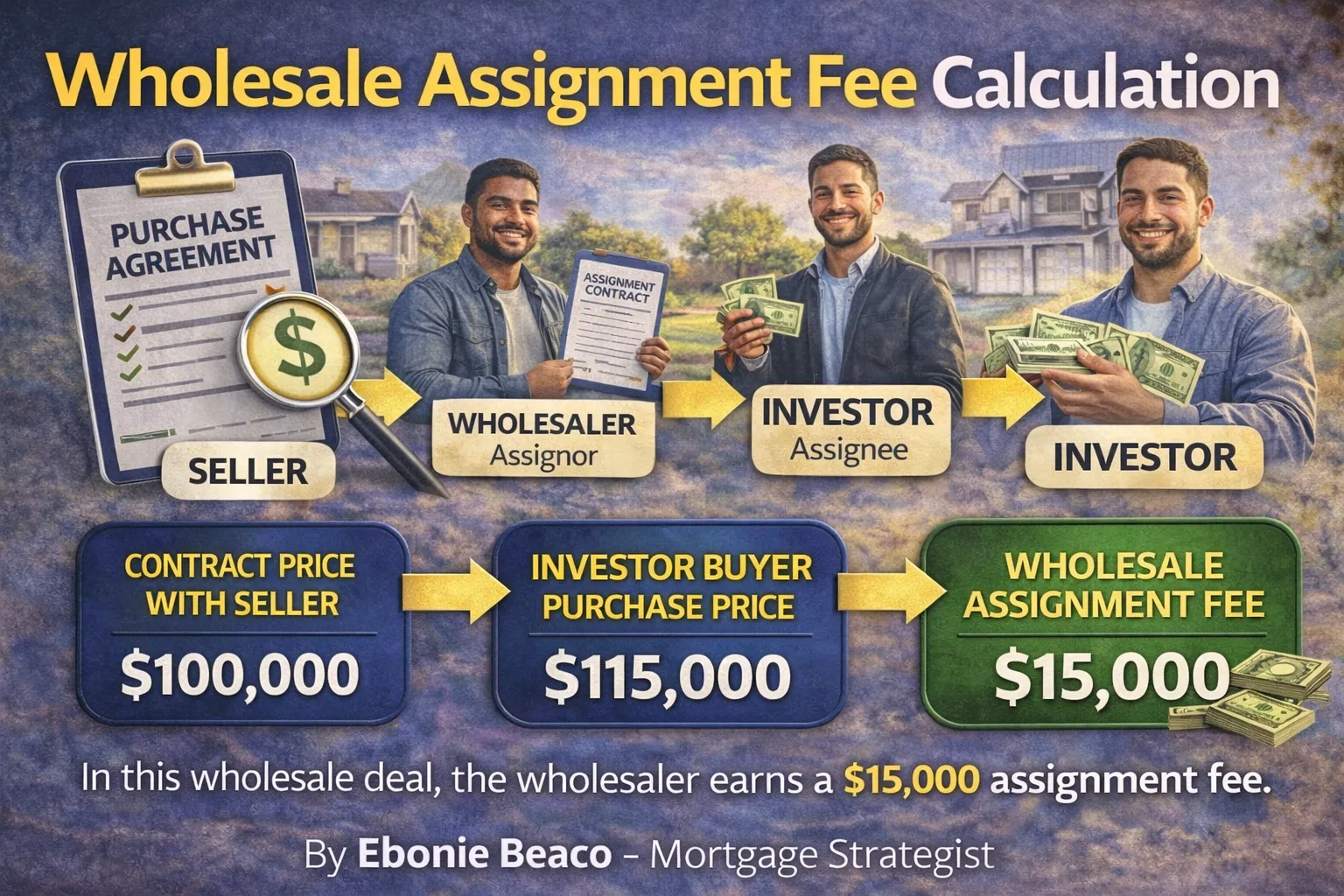

Assignment of Contract: A secondary legal document that transfers your rights and obligations from the original purchase agreement to an end buyer. Benefit: This allows you to exit the deal and collect a fee without ever taking title or managing the property.

Double Closing: A transaction where the wholesaler actually purchases the property from the seller (A-B) and immediately sells it to the end buyer (B-C). Benefit: This keeps your profit margin private from both the seller and the end buyer, which is helpful on high-spread deals.

Earnest Money Deposit (EMD): A sum of money provided by the buyer to demonstrate "good faith" in completing the transaction. Practical application: In wholesaling, your end buyer’s EMD should typically be higher than the EMD you gave the seller to ensure they are committed to the deal.

Phase 1: Securing the Purchase Agreement

Your journey begins when a seller signs your Real Estate Purchase Contract (REP-C).

In competitive markets like Atlanta or Los Angeles, speed is your primary advantage.

You must ensure your contract contains the specific language that allows you to assign the deal.

Use the phrase "and/or assigns" next to your name in the buyer field.

According to standard real estate law, this language signals to the seller that you may pass the contract to another entity or individual before the closing date.

Always include an inspection period or "due diligence" window.

This period, often 7 to 14 days, provides you the time to bring your cash buyers through the property and confirm your repair estimates.

If you cannot find a buyer or the property condition is worse than expected, this clause allows you to cancel the contract and retrieve your EMD.

Phase 2: Choosing Your Exit Strategy

Once you have the property under contract, you must decide how to structure the closing.

Your choice depends on your profit margin and the transparency you want to maintain.

The Assignment of Contract Method

The assignment of contract is the most common logistics path for wholesalers.

You sign a one or two-page document with your end buyer.

This document states that they are taking over your position in the original contract for a specific assignment fee.

The end buyer pays the purchase price to the seller and the assignment fee to you.

This method is efficient and keeps closing costs low because there is only one transaction recorded at the county level.

Explore the details of the loan process to see how end buyers often fund these acquisitions.

The Double Closing Strategy

A double closing is more complex but necessary in certain scenarios.

If your assignment fee is exceptionally high (e.g., $50,000+), some sellers or buyers might feel uncomfortable seeing that spread on a single settlement statement.

In a double closing, you have two separate transactions: the A-B (Seller to You) and the B-C (You to End Buyer).

You will pay closing costs on both sides, but your profit remains confidential.

This is common in Florida and California, where high-value flips often involve significant spreads.

Jump in and compare these options based on your specific deal margins.

Phase 3: Navigating State-Specific Logistics

Logistics vary significantly depending on where you are operating.

Wholesaling in Georgia (Atlanta Market)

In Georgia, real estate closings must be conducted by a licensed attorney.

You need to find a "wholesaler-friendly" attorney who understands how to handle assignments and double closings.

Atlanta is a high-velocity market where investors often use hard money or bridge loans to fund their side of a double closing.

If you are looking for local insights, the Atlanta homeowner wealth alert highlights how investors in this region are turning equity into funding machines.

{kind=link}

Wholesaling in Florida

Florida is a popular state for wholesaling due to the high volume of distressed properties.

Title companies, rather than attorneys, typically handle the closing process here.

You should ensure your title company is familiar with "assignment fee disclosure" requirements on the HUD-1 or ALTA settlement statement.

Wholesaling in California

California has strict disclosure laws and specific requirements for how contracts are structured.

Many California wholesalers prefer double closings to minimize legal friction regarding "brokering without a license" concerns.

Always consult with a professional who understands California’s unique regulatory environment.

Phase 4: Managing the Title and Escrow Process

The title company or closing attorney is the "engine room" of your transaction.

Once you have both the purchase agreement and the assignment contract signed, you must open escrow.

Provide the title officer with:

- The original purchase agreement between you and the seller.

- The assignment of contract between you and the end buyer.

- Contact information for all parties involved.

The Earnest Money Logistics

Your end buyer should deposit their EMD with the title company immediately.

This money acts as security; if the buyer walks away after the inspection period, you (the wholesaler) usually keep that deposit as liquidated damages.

Confirm that the title company is clear on who receives the EMD in the event of a default.

Phase 5: Clearing Title and Solving Problems

Logistics often get messy during the title search.

The title company will look for liens, judgments, or "clouds" on the title that prevent a clean transfer.

Common issues include:

- Unpaid property taxes.

- Mechanic's liens from previous contractors.

- Heirship issues (if the owner is deceased).

As the wholesaler, you are the problem solver.

You may need to track down relatives to sign "quitclaim deeds" or negotiate with lienholders to accept a lower payoff.

Keeping the deal on track during this phase is what earns you your assignment fee.

If your end buyer is using professional financing, like DSCR rental property loans, the lender will require a clear title before they release funds.

You can learn more about how investors qualify for these types of loans by visiting our loan programs page.

Phase 6: The Closing Table

On closing day, the "funding" logistics take center stage.

In an assignment, the end buyer sends the full purchase price plus your assignment fee to the title company.

The title company then pays off the seller's mortgage, pays the seller their proceeds, and cuts a check (or wires funds) to you for your fee.

If you are double closing, the timing is critical.

Some states allow for "dry closings" or "simultaneous closings" where the money from the B-C transaction is used to fund the A-B transaction.

However, many title companies now require "transactional funding" for double closings.

Transactional Funding: A short-term loan (often 24 hours) used by a wholesaler to close on the first part of a double closing. Practical application: This ensures you have the funds to buy the property before you immediately sell it to your end buyer.

Avoiding Common Wholesaling Pitfalls

Even with a great deal, poor logistics can ruin your reputation.

Never handle the money yourself. All EMD and purchase funds should go directly to a third-party escrow account or title company.

Don't overpromise on condition. Be transparent with your end buyers about the repairs needed. If they find a foundation issue you "missed," they will never buy from you again.

Verify your buyer’s proof of funds. Before signing an assignment contract, ask for a bank statement or a pre-approval letter from a reputable lender.

Many investors use mortgage calculators to ensure their numbers work before committing to your deal.

Transitioning from Wholesaler to Investor

Many successful wholesalers eventually decide to keep the best deals for themselves.

Instead of assigning the contract for $10,000, they realize they could make $50,000 by fixing and flipping the property or $500 a month in passive income by keeping it as a rental.

When you transition to "buying and holding," your financing needs change.

You might look into fix and flip financing or DSCR investor loans that don't require personal income verification.

Ebonie Beaco and the team at Home Loans Network specialize in helping investors scale from their first wholesale deal to a massive portfolio.

Access our about us page to learn how we support the growth of real estate professionals across the country.

Final Logistics Checklist

Before you head to your next closing, run through this list:

- Is the "and/or assigns" language in your original contract?

- Has the end buyer deposited their EMD with the title company?

- Is the inspection period clearly defined and has it expired?

- Have you confirmed if the title company requires transactional funding for a double close?

- Are all parties aware of the closing date and location?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664