How to Get a 7-Day HELOC in California, Florida, or Georgia (The Easy Guide)

Home equity is sitting at record highs across the United States. If you live in California, Florida, or Georgia, you are likely sitting on a goldmine of untapped wealth. In the past, accessing that cash meant waiting 45 to 60 days for a traditional bank to shuffle through paperwork.

The landscape changed. Today, modern homeowners and investors can access a 7-Day HELOC by leveraging digital platforms and streamlined appraisal methods.

Whether you want to renovate your kitchen in Atlanta, consolidate high-interest debt in Miami, or fund a down payment for an investment property in Los Angeles, speed is a critical factor. This guide explores how to navigate the fast-track process for a Home Equity Line of Credit in these three powerhouse states.

Core Definitions for Homeowners

HELOC (Home Equity Line of Credit): A revolving credit line secured by the equity in your primary residence or investment property.

Application: Use it like a credit card to draw funds as needed and pay interest only on what you use.

CLTV (Combined Loan-to-Value): The sum of all your mortgage balances divided by the current market value of the property.

Application: Lenders use this percentage to decide the maximum amount you can borrow.

DTI (Debt-to-Income Ratio): Your monthly recurring debt payments divided by your gross monthly income.

Application: This helps the lender verify that you can comfortably handle a new line of credit.

AVM (Automated Valuation Model): A technology-driven property valuation that uses local sales data rather than a physical inspection.

Application: This is the secret sauce that allows for a 7-day closing timeline.

Why Speed is Essential in Today’s Market

Waiting two months for a loan approval does not work for everyone. If you are a real estate investor looking at a fix and flip opportunity in Georgia, you need cash immediately to secure the deal.

Homeowners in California and Florida often face rising costs for contractors. Locking in your funding quickly ensures you can start your renovations before prices shift again. A 7-day timeline provides the liquidity you need without the traditional red tape.

The 7-Day HELOC Roadmap

To hit a one-week closing, the process must be digital. Traditional banks often require physical appraisals and manual underwriting, which adds weeks to the timeline. Modern mortgage strategists use automated systems to verify income, credit, and property value.

Submit Your Digital Application

Everything starts with an online portal. You will provide your basic information, property address, and estimated mortgage balance. You can access our online forms to start this initial step.

Sync Your Financial Data

Instead of mailing stacks of paper, you will link your bank accounts or upload digital PDFs of your W-2s and pay stubs. To hit the 7-day mark, you must provide these documents within the first 24 hours of your application.

Automated Valuation

For many 7-day programs, a full interior appraisal is not required. The lender uses an AVM to determine your home’s value. This eliminates the need to schedule an appraiser and wait for a written report.

Virtual Notary or Mobile Closing

Once approved, you sign your closing documents. In many states, this can be done via a remote online notary or a mobile notary who comes to your home.

California HELOC: Navigating High-Value Equity

California remains one of the most robust real estate markets in the world. Homeowners in cities like San Diego, San Francisco, and Los Angeles have seen massive equity growth over the last five years.

Explore ADU Opportunities

Many California homeowners use a California HELOC to fund the construction of Accessory Dwelling Units (ADUs). With new state laws making it easier to build these units, a HELOC provides the capital to add value and rental income to your property.

Manage High Property Values

Because California home values are often significantly higher than the national average, the equity available is substantial. Even with a 75% or 85% CLTV limit, a California homeowner can often access six figures in credit to fund other investments or clear out high-interest credit cards.

Florida HELOC: Leveraging Sunshine State Growth

From Jacksonville down to the Keys, Florida has experienced an influx of new residents and capital. This migration has sent property values soaring, creating a perfect environment for a Florida HELOC.

Renovations and Resilience

Florida homeowners often use equity for "hard" renovations, such as impact-resistant windows or new roofing systems. These improvements are not just about aesthetics; they can help lower insurance premiums and increase the home's resale value in a competitive market.

Investment Property Down Payments

Florida is a hub for short-term rentals and Airbnb investing. Savvy owners use a HELOC on their primary home to secure the down payment for a DSCR loan on a coastal rental property. This strategy allows you to grow your portfolio without depleting your cash reserves.

Georgia HELOC Lender: The Atlanta Advantage

The Georgia market, particularly the Atlanta metro area, has become a tech and film industry powerhouse. As a Georgia HELOC lender, we see many homeowners looking to tap into their suburban equity.

Debt Consolidation Strategy

With interest rates on credit cards remaining high, Georgia homeowners are using HELOCs to consolidate debt. By moving high-interest balances to a lower-interest HELOC, you can significantly reduce your monthly outflow and improve your credit profile.

Bridging the Gap

Investors in Georgia often use HELOCs as a "bridge" to fund the acquisition of distressed properties. Once the property is renovated, they can refinance into a long-term rental loan and pay back the HELOC.

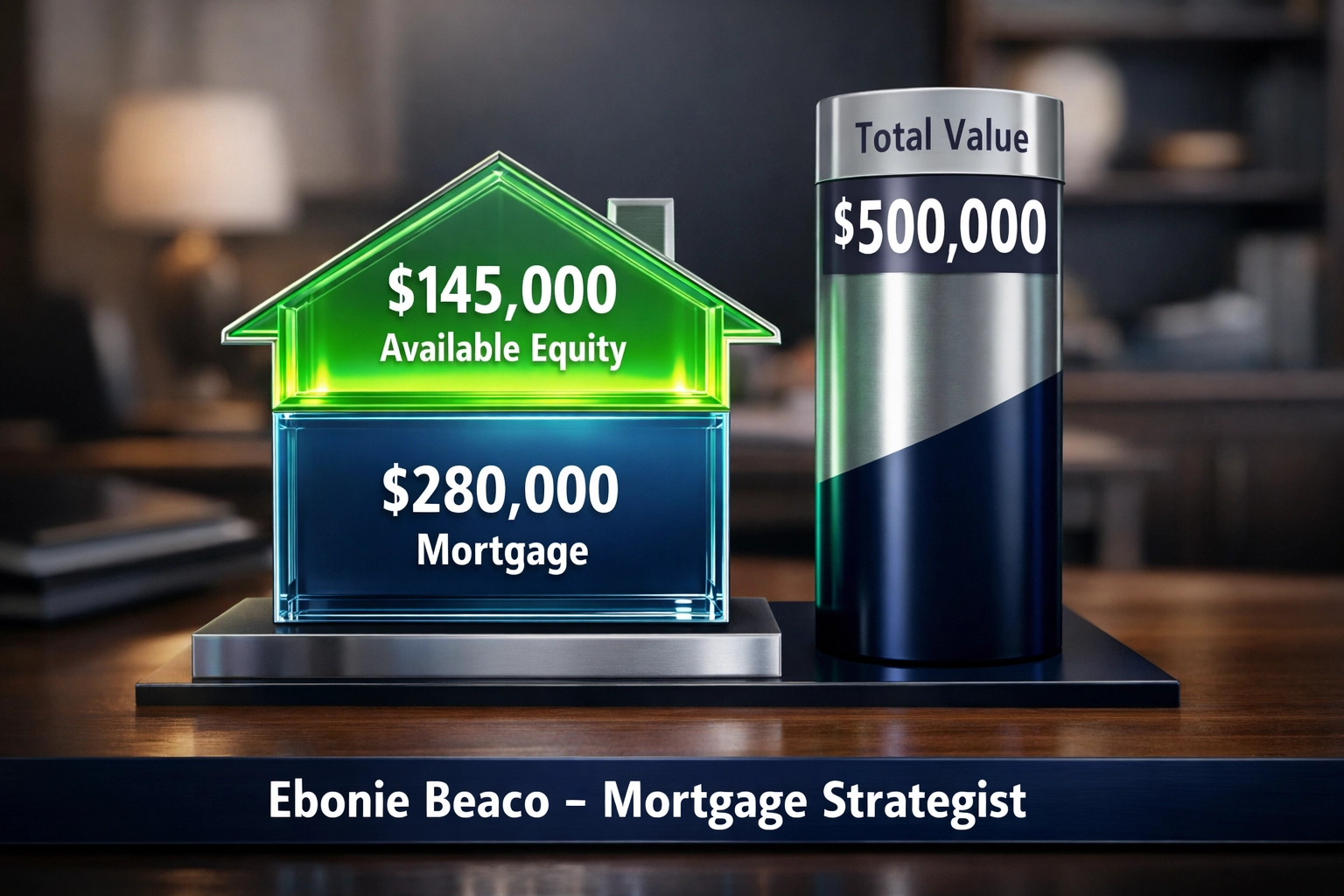

Real-World HELOC Calculation

To understand how much you can access, let’s look at a practical scenario for a homeowner in a market like Atlanta or Orlando.

- Current Home Value: $500,000

- Current Mortgage Balance: $280,000

- Max CLTV (85%): $425,000

- Available HELOC Amount: $145,000 ($425,000 - $280,000)

In this scenario, the homeowner can secure a credit line of $145,000. They do not have to spend all $145,000 at once. They can draw $20,000 for a kitchen refresh, pay it down, and still have the remaining balance available for future needs.

Qualifications for a Rapid Closing

To ensure your loan moves through the system in seven days, you generally need to meet specific criteria.

Credit Score Requirements

While some programs allow for lower scores, a score of 680 or higher is typically required for the fastest approvals. Scores above 720 generally secure the most favorable interest rates.

Loan Amount Caps

Most "expedited" or 7-day HELOC programs cap the loan amount at $400,000. If you need a larger line of credit, the underwriting process may require additional manual reviews which can extend the timeline.

Debt-to-Income Ratios

Keep your DTI below 43% for the smoothest experience. If your debt load is higher, you may need to provide additional explanations or documentation, which can slow down the clock.

Common Uses for Home Equity

Home Improvements

Upgrade your living space or increase your home's value before selling.

Debt Consolidation

Pay off high-interest credit cards or personal loans to save on monthly interest costs.

Real Estate Investing

Use your equity as a down payment for a second home, a rental property, or a fix-and-flip project.

Emergency Fund

Keep a line of credit open as a safety net for unexpected medical bills or major home repairs.

Jump In: How to Prepare

Preparation is the key to speed. Before you apply, gather your most recent mortgage statement, your homeowners insurance declaration page, and your most recent tax returns. Having these ready allows you to respond to lender requests instantly.

If you are unsure about your home’s current value or how much you can borrow, you can use our mortgage calculators to run different scenarios.

Compare your options and look at the long-term benefits of accessing your equity now rather than waiting for traditional bank timelines. The flexibility of a HELOC makes it one of the most powerful financial tools for homeowners in California, Florida, and Georgia.

Secure Your Financial Future

Accessing the equity in your home shouldn't be a months-long ordeal. By choosing a streamlined, digital-first approach, you can put your home's value to work for you in as little as one week. Whether you are looking to build wealth through real estate or simply simplify your monthly finances, a HELOC provides the path to your goals.

Explore your equity options today. If you have questions about specific state requirements or want to see if your property qualifies for an AVM, our team is ready to guide you.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664