How to Finance a Short-Term Rental (Airbnb) Property

Short-term rentals (STRs) have completely changed the way people look at real estate investing. Whether you are eyeing a beachfront condo in Florida, a historic row house in Virginia, or a trendy loft in Chicago, the potential for high returns is significant. However, getting the right financing for an Airbnb property is different than buying a standard home.

Lenders view STRs with a different lens because the income can be seasonal or volatile. If you are looking to enter this space, you need a strategy that fits your long-term goals. From conventional loans to specialized investor products, understanding your options is the first step toward building a profitable portfolio.

The Short-Term Rental Financing Landscape

When you decide to purchase a property for Airbnb or Vrbo, the financing you choose will impact your cash flow and your ability to scale. Traditional banks often look at these properties as high-risk assets, but specialized mortgage strategists understand how to navigate the nuances of the STR market.

Before you apply, you should evaluate the property’s potential. Markets like those in Michigan, Indiana, and Arkansas have seen a surge in STR activity, but each area has its own set of rules and demand drivers.

Explore the loan process to see how these steps differ from a standard home purchase.

Conventional Mortgages for STRs

Conventional Loan: A mortgage that is not backed by a government agency, typically following guidelines set by Fannie Mae or Freddie Mac.

Application: This is a common path for investors who have strong credit and a steady personal income.

If you do not plan to live in the property, you will typically need to apply for an investment property loan. These usually require a down payment of 15% to 25%. Lenders will also want to see cash reserves: often six months of mortgage payments: to ensure you can handle the monthly costs if the property sits vacant for a few weeks.

According to research, conventional loans often carry a slightly higher interest rate for investment properties compared to primary residences. However, they remain a reliable choice for those with a debt-to-income (DTI) ratio that can support another mortgage payment.

House Hacking: FHA and VA Loans

House Hacking: A strategy where a homeowner lives in one part of a multi-unit property (like a duplex or fourplex) or rents out spare rooms to cover their mortgage.

Application: This is a powerful way for new investors in states like Kentucky or Missouri to get started with very little money down.

If you purchase a multi-unit building and live in one of the units, you can use an FHA loan (3.5% down) or a VA loan (0% down for eligible veterans). This allows you to list the other units on Airbnb while benefiting from low-down-payment primary residence financing.

Keep in mind that FHA guidelines generally prohibit stays shorter than 30 days for the units you aren't living in, so you must ensure your rental strategy complies with federal rules and local ordinances.

DSCR Loans: The Investor’s Choice

DSCR Loan: A Debt Service Coverage Ratio loan is a mortgage where qualification is based on the property’s rental income rather than the borrower’s personal income or employment history.

Application: This is the go-to tool for investors who want to scale their portfolio without being restricted by their personal tax returns or DTI.

For an Airbnb, lenders use a DSCR calculation to see if the projected rental income covers the monthly mortgage, taxes, insurance, and HOA fees. Instead of looking at your W-2s, the lender looks at data from platforms like AirDNA to estimate what the property will earn. This is particularly useful in high-demand markets like California and Georgia.

Calculating Your Potential Returns

When analyzing a deal, you need to know your Projected Rental Yield. This figure helps you compare different properties to see which one provides the best return on your capital.

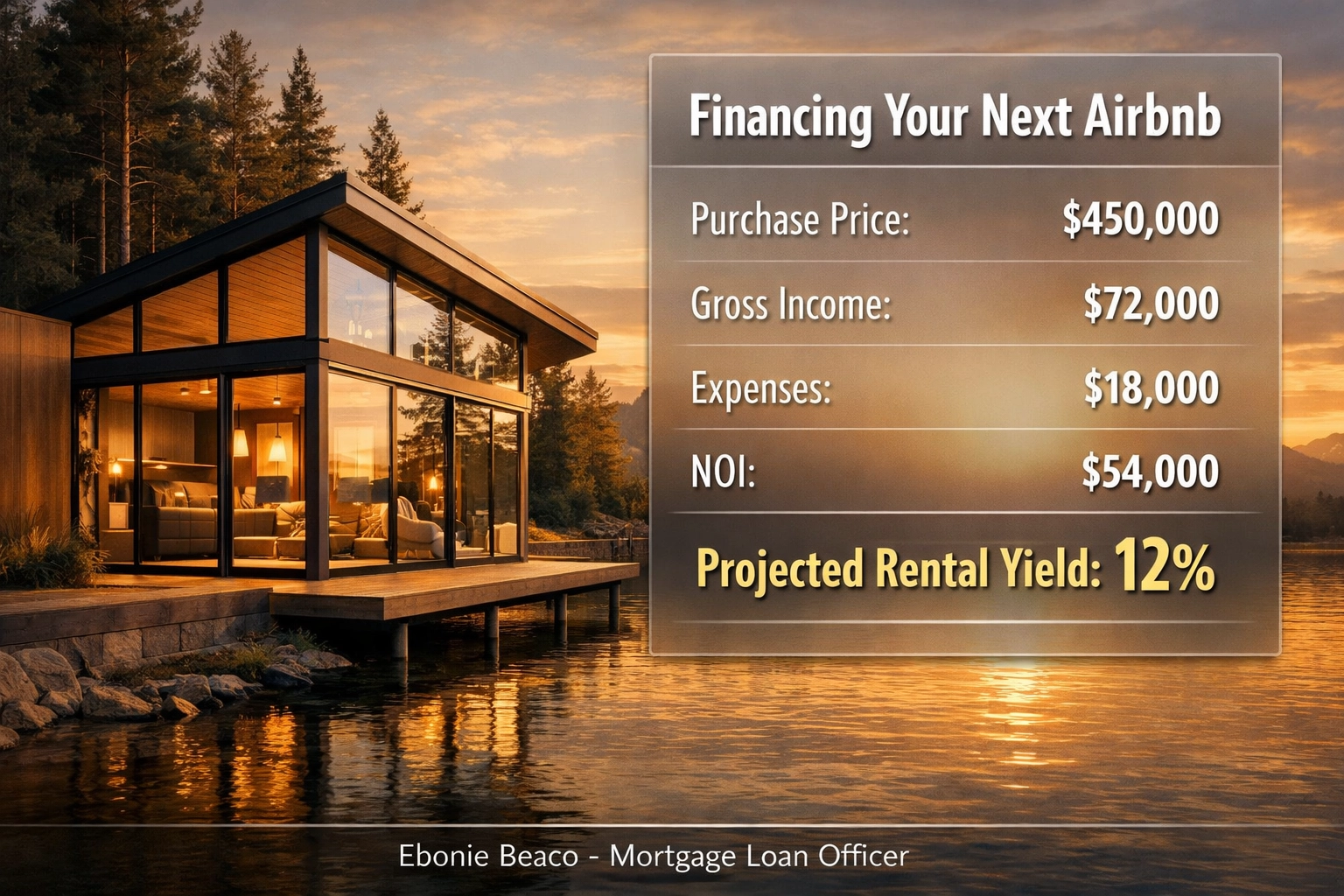

Example Calculation: Projected Rental Yield

- Property Purchase Price: $450,000

- Annual Gross Rental Income (STR): $72,000

- Annual Operating Expenses (Utilities, Cleaning, Taxes, Insurance): $18,000

- Net Operating Income (NOI): $54,000 ($72,000 - $18,000)

- Projected Rental Yield: (NOI / Purchase Price) x 100

- Calculation: ($54,000 / $450,000) x 100 = 12%

Visual Breakdown: Title: Financing Your Next Airbnb. Calculations: Purchase Price $450,000 | Gross Income $72,000 | Expenses $18,000 | NOI $54,000 | Projected Rental Yield 12%. Ebonie Beaco - Mortgage Loan Officer at bottom.

Visual Breakdown: Title: Financing Your Next Airbnb. Calculations: Purchase Price $450,000 | Gross Income $72,000 | Expenses $18,000 | NOI $54,000 | Projected Rental Yield 12%. Ebonie Beaco - Mortgage Loan Officer at bottom.

Using Your Existing Equity

If you already own a home in Alabama or Florida, you might be sitting on the capital you need for your next Airbnb down payment.

Cash-Out Refinance: Replacing your current mortgage with a new, larger loan and taking the difference in cash.

Application: This allows you to tap into your home’s value to fund a new investment without needing to save for years.

HELOC (Home Equity Line of Credit): A revolving line of credit that uses your home as collateral.

Application: This works like a credit card tied to your home's equity, giving you the flexibility to pay for renovations or down payments as needed.

Using equity is a strategic move for landlords who want to grow their footprint. You can use mortgage calculators to see how much equity you can safely withdraw while keeping your monthly payments manageable.

Hard Money and Bridge Loans

Hard Money Loan: A short-term, high-interest loan secured by real estate, typically used for quick acquisitions or fix-and-flip projects.

Application: Use this if you find a distressed property that needs work before it can be listed on Airbnb.

Bridge Loan: A short-term loan used to "bridge" the gap between the purchase of a new property and the securing of permanent financing.

Application: These are excellent for winning deals in competitive markets where you need to close fast and refinance into a long-term DSCR loan later.

Hard money lenders focus on the "After Repair Value" (ARV). If you are looking at a property in a vacation destination that needs a cosmetic facelift, a bridge loan can get you to the finish line quickly.

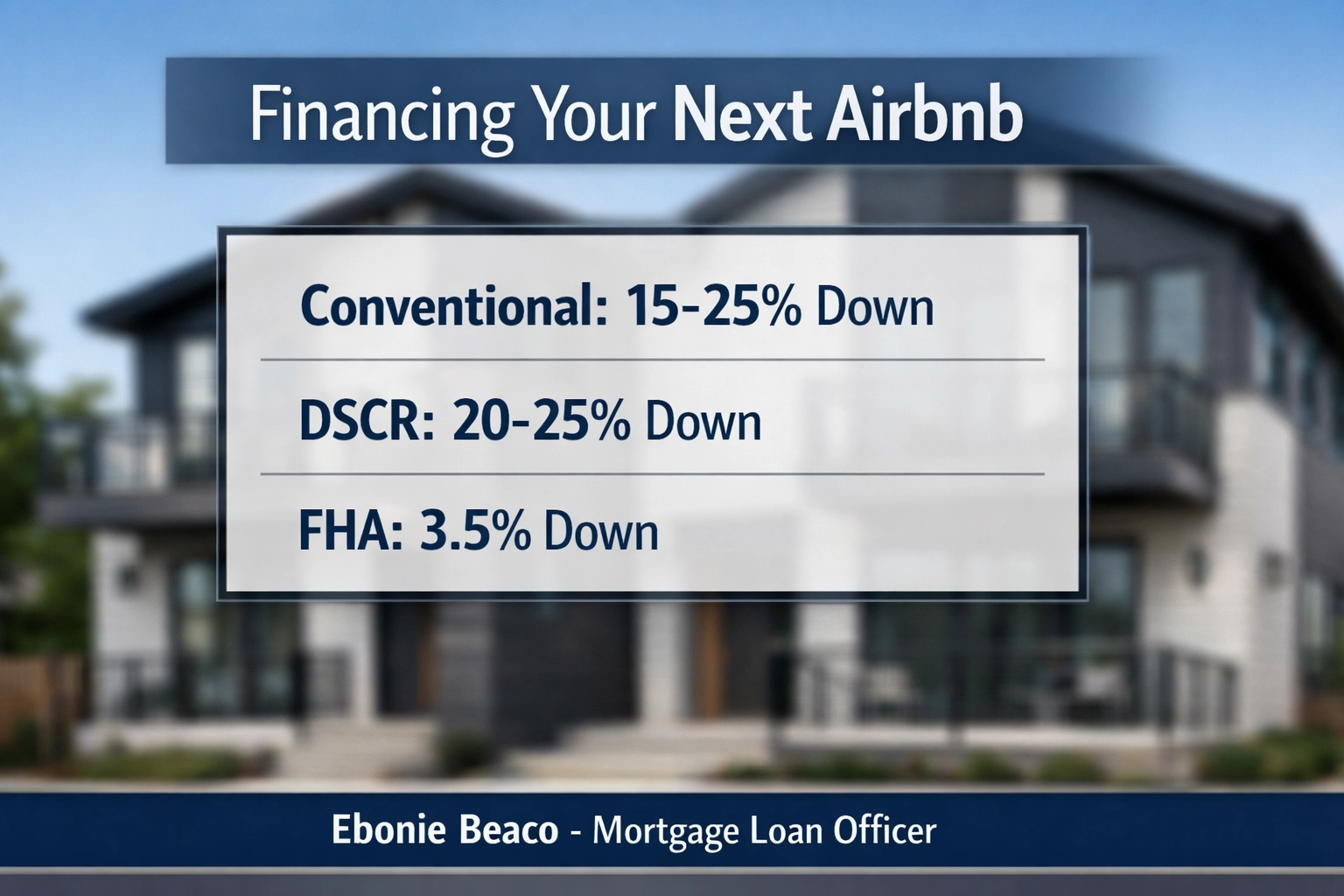

Visual Breakdown: Title: Financing Your Next Airbnb. Comparison Chart: Loan Type vs. Down Payment. Conventional (15-25%), DSCR (20-25%), FHA (3.5%). Ebonie Beaco - Mortgage Loan Officer at bottom.

Visual Breakdown: Title: Financing Your Next Airbnb. Comparison Chart: Loan Type vs. Down Payment. Conventional (15-25%), DSCR (20-25%), FHA (3.5%). Ebonie Beaco - Mortgage Loan Officer at bottom.

Regional Regulations and Market Insights

Financing is only one part of the equation. You must also account for local laws.

- Chicago, IL: Has specific registration requirements and taxes for STR hosts.

- Florida Cities: Many coastal areas have strict zoning, but others are very investor-friendly.

- Virginia: Localities have the power to regulate STRs, so checking the specific county code is vital.

Lenders will want to see that the property you are financing is legally allowed to operate as a short-term rental. If the city bans Airbnbs next year, your income could vanish, which is a risk lenders evaluate during the underwriting process. You can find more details in our FAQ section.

Steps to Secure Your STR Financing

- Analyze the Market: Use data tools to see average nightly rates and occupancy in your target area.

- Check Your Credit: Even for DSCR loans, a higher credit score can get you better interest rates.

- Gather Your Team: Work with a mortgage strategist who understands investor-specific products.

- Review the Title: Ensure there are no deed restrictions or HOA rules against short-term stays.

- Calculate Your Numbers: Never buy based on "gut feeling." Use the Projected Rental Yield formula to ensure the deal makes sense.

Whether you are looking for your first Airbnb or your tenth, the right financing structure can make or break your investment. By leveraging products like DSCR loans or your existing home equity, you can build a sustainable and profitable rental business.

Ready to invest in an Airbnb? Contact Ebonie Beaco for specialized STR financing.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664