How to Choose the Best Chicago DSCR Loan Lender (Compared)

SEO Title: How to Choose the Best Chicago DSCR Loan Lender (Compared)

Meta Description: Compare the best Chicago DSCR loan lenders for real estate investors. Learn how to evaluate rates, terms, and LTV for Chicago rental properties and Airbnb.

URL Slug: how-to-choose-best-chicago-dscr-loan-lender

Featured Image Recommendation: A landscape photograph of classic Chicago brownstone properties with the Chicago city skyline in the background, branded with the REI Vault Pro URL.

SEO Alt Text: Chicago residential real estate with city skyline background for DSCR loan lender comparison guide.

Social Media Excerpt: Scaling a real estate portfolio in Chicago requires the right financing. Our latest guide compares top DSCR lenders and breaks down a real-world Chicago investment calculation.

SEO Tags: Chicago DSCR Loans, Real Estate Investing Illinois, DSCR Lender Comparison, Rental Property Financing, Chicago Airbnb Loans, Non-QM Loans Chicago, REI Vault Pro

Navigating the Chicago real estate market requires more than just finding the right property; it requires securing the right financing strategy. For many investors in the Windy City, the DSCR loan has become the primary tool for scaling rental portfolios without the hurdles of traditional income verification.

A DSCR Loan (Debt Service Coverage Ratio Loan) is a mortgage program that qualifies a borrower based on the cash flow of the subject property rather than personal income or tax returns. You can explore various mortgage solutions to see how non-traditional lending compares to standard programs.

Choosing a lender for a Chicago investment property is significant because the local landscape involves high property taxes, specific short-term rental (STR) ordinances, and a high concentration of multi-unit buildings. This guide compares the leading lender types and provides a framework for selecting the best partner for your Chicago real estate goals.

Understanding DSCR Loans in the Chicago Market

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to determine if a property's rental income covers its debt obligations.

Practical Application: Investors use this to qualify for loans using the property’s projected or actual rent, allowing them to bypass Debt-to-Income (DTI) ratio requirements.

In Chicago, the DSCR calculation is particularly sensitive to property taxes and insurance. Because Cook County taxes can be higher than in neighboring regions, the "T" in your PITI (Principal, Interest, Taxes, and Insurance) carries significant weight. A lender with experience in the Illinois market will understand how to accurately estimate these costs during the pre-approval phase.

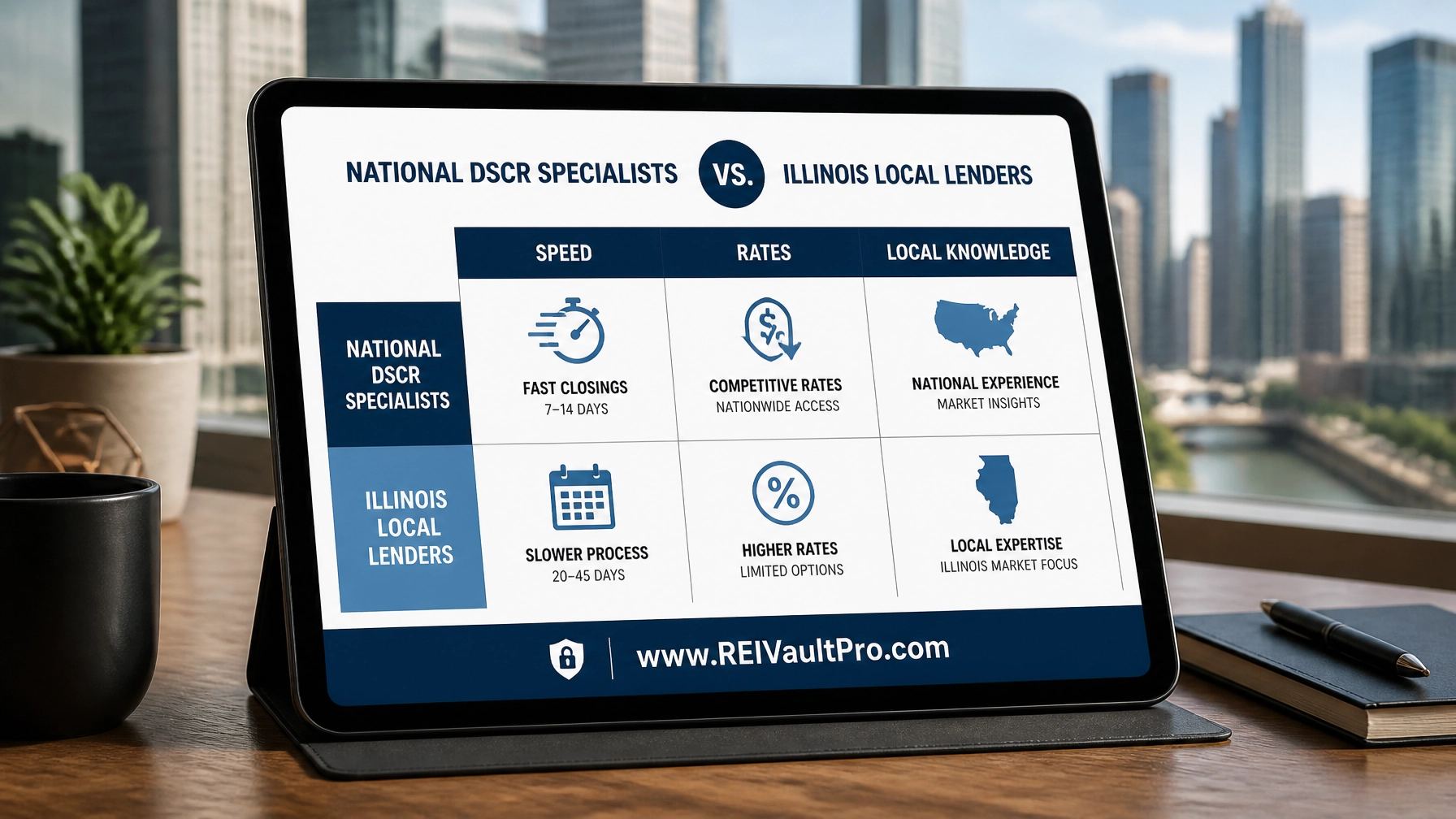

Comparing National vs. Local Chicago DSCR Lenders

When you begin your search, you will generally encounter two types of lending institutions: large national specialists and local Illinois-based firms.

National DSCR Specialists

These lenders operate across the United States and often provide highly standardized, tech-driven processes.

- Strengths: High speed of execution, competitive rates for "cookie-cutter" deals, and robust online portals.

- Best For: Investors looking for a streamlined digital experience for single-family rentals or portfolios across multiple states.

Local Illinois Lenders

These are firms with a physical presence or a deep focus on the Chicago metropolitan area.

- Strengths: Deep knowledge of Chicago neighborhoods, familiarity with local building codes (relevant for 2-4 unit properties), and relationships with local appraisers.

- Best For: Investors purchasing unique Chicago properties like Greystones, legal/non-conforming multi-family units, or properties in emerging neighborhoods.

Comparing these options is easier when you access professional deal analysis tools to see how different loan terms impact your bottom line.

5 Critical Factors for Evaluating Your Financing Partner

To find the best lender for your specific deal, evaluate them based on these five criteria:

- Maximum Loan-to-Value (LTV): Most DSCR lenders cap LTV at 75% or 80%. If you are looking to keep more cash in your pocket, prioritize lenders that offer higher leverage for borrowers with high credit scores.

- Minimum DSCR Ratio: Standard lenders often require a ratio of 1.20 or 1.25. However, if you have a property in a high-tax Chicago area where cash flow is tighter, look for lenders that offer "no-ratio" or "low-ratio" (below 1.0) programs.

- Prepayment Penalty Structure: DSCR loans often come with prepayment penalties (e.g., 5-4-3-2-1). If you plan to sell or refinance within a few years, a flexible or shorter penalty period is essential.

- Short-Term Rental (STR) Friendly: Not all DSCR lenders allow Airbnb or VRBO income to be used for qualification. In Chicago, where STR regulations are strict, you need a lender that understands how to use AirDNA data or historical STR ledgers.

- Closing Speed: In a competitive market like Chicago, the ability to close in 21 to 30 days can be the difference between a winning offer and a rejected one.

Practical Example: DSCR Calculation for a Chicago Three-Flat

To understand how a lender will view your deal, let's look at a typical Chicago three-flat acquisition. Multi-unit buildings are a staple of the Chicago market, often providing the best path to achieving a strong DSCR.

The Scenario:

- Property Value: $600,000

- Down Payment (25%): $150,000

- Loan Amount: $450,000

- Total Monthly Rental Income: $6,000 ($2,000 per unit)

- Estimated Monthly PITI: $4,800 (Includes high Chicago property taxes and insurance)

The Calculation:

$6,000 (Income) / $4,800 (Debt Service) = 1.25 DSCR

A DSCR of 1.25 is generally considered the "sweet spot" for most lenders, often qualifying you for the most competitive interest rates. You can use a dedicated rental property analyzer to run these numbers for any Chicago address before you submit an offer.

Specific Considerations for Chicago Airbnb and Short-Term Rentals

The Chicago "House Share" and Short-Term Rental market is highly regulated. When choosing a DSCR lender for an STR, you must ensure their underwriting team accepts "transient" income. Some lenders will only use "Long-Term Market Rent" (comparable to traditional leases) based on an appraiser's 1007 Rent Schedule.

If the market rent is significantly lower than the projected Airbnb income, your DSCR might drop below the required threshold. Working with a lender that specializes in Airbnb and short-term rental financing allows you to use the actual income potential of the property to qualify.

Matching Your Strategy with the Right Lender

Your investment strategy dictates the best lender choice. If you are executing a BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy in Chicago, you need a lender that can transition you seamlessly from a fix and flip loan into a long-term DSCR mortgage.

If you are a self-employed investor, the DSCR loan remains one of the most effective mortgage options for self-employed borrowers, as it ignores the complex personal tax returns that often limit traditional financing.

Before committing to a lender, compare at least three different term sheets. Look beyond just the interest rate; the total cost of the loan, including points and junk fees, influences your overall ROI.

Related REI Vault Pro Resources

- Deal Analyzer: This tool allows you to input property data and loan terms to see instant cash flow and ROI projections for Chicago properties. Access the Deal Analyzer.

- AI Rent Analyzer: Get accurate, real-time rental data for any Chicago neighborhood to ensure your DSCR projections are realistic. Access the AI Rent Analyzer.

- AI Rehab Estimator: Perfect for BRRRR investors, this tool helps you calculate renovation costs before you seek fix-and-flip or bridge financing. Access the AI Rehab Estimator.

- REI Vault Pro Demo: See the full suite of investment tools in action and learn how to integrate financing data into your deal-finding process. Watch the Demo.

- REI Vault Pro Join: Ready to scale your portfolio with the best technology and financing insights? Join the community today. Join Now.

Conclusion

Choosing the best Chicago DSCR loan lender is a process of aligning your specific property type and long-term goals with a lender's unique underwriting strengths. Whether you are focusing on high-cash-flow three-flats in Logan Square or scaling a portfolio of short-term rentals near the lakefront, the right financing partner will provide the leverage you need to build wealth through real estate.

Compare your options carefully and use the right tools to verify every calculation. Jump in and start analyzing your next deal today.

Explore your financing options and see how the right loan structure can accelerate your growth. Start a Free Trial or Join REI Vault Pro to access our full suite of investor tools.

FAQ Section

What is the minimum credit score for a Chicago DSCR loan?

Most lenders require a minimum FICO score of 620 to 660, though the most competitive rates and highest LTVs are typically reserved for borrowers with scores above 720.

Can I get a DSCR loan for a property in Chicago if it is currently vacant?

Yes. Lenders will use the "market rent" determined by an appraiser's comparable rent schedule to calculate the DSCR ratio for a vacant property.

Do Chicago DSCR lenders require a personal guarantee?

While DSCR loans are based on property cash flow, most lenders still require a personal guarantee from the primary members of the LLC or the individual borrower.

Are DSCR loans available for Chicago multi-family properties?

Yes, DSCR loans are very common for 2-4 unit residential properties. For properties with 5 or more units, you would transition into a commercial DSCR or small balance multi-family loan program.

How does Chicago's property tax increase impact my DSCR?

Because property taxes are part of the PITI calculation, an increase in taxes will lower your DSCR ratio. It is essential to use the most recent tax assessments when running your numbers.