How to Choose the Best Chicago DSCR Loan Lender (Compared)

SEO Title: How to Choose the Best Chicago DSCR Loan Lender (Compared)

Meta Description: Compare top Chicago DSCR loan lenders for 2026. Learn requirements for LTV, rates, and credit scores to fund your next Chicago rental property investment.

URL Slug: best-chicago-dscr-loan-lenders-compared

Featured Image Recommendation: A professional landscape shot of the Chicago skyline with financial data overlays and the REI Vault Pro website URL.

SEO Alt Text: Chicago real estate investment skyline with DSCR loan financial data and www.REIVaultPro.com branding.

Social Media Excerpt: Looking for the best DSCR loan in Chicago? We compare top lenders and requirements so you can scale your rental portfolio with confidence.

SEO Tags: Chicago DSCR Loans, Real Estate Investing Chicago, DSCR Lender Comparison, Landlord Loans Chicago, REI Vault Pro

Chicago remains one of the most dynamic markets for real estate investors in the Midwest. From the iconic brick three-flats in Logan Square to the growing rental demand in the South Side, the city offers diverse opportunities for building long term wealth.

Accessing the right capital is the most critical step for any landlord or portfolio builder. Debt Service Coverage Ratio (DSCR) loans have become the preferred choice for Chicago investors because they prioritize property performance over personal income.

What is a DSCR Loan?

DSCR Loan: A mortgage product for investment properties that qualifies borrowers based on the property’s rental income rather than personal debt to income ratios.

This financing structure allows you to acquire or refinance properties without providing tax returns or W-2s. It is particularly effective for self-employed investors or those with complex financial profiles who need to move quickly in the competitive Chicago market.

Why Chicago Investors Choose DSCR Financing

The Chicago rental market is unique because of its high density of multi-unit buildings. Most traditional lenders struggle with the complexities of Cook County taxes and specific neighborhood rental fluctuations.

DSCR lenders provide a solution by looking strictly at the numbers. If your property generates enough cash flow to cover the debt, you can often secure funding in a fraction of the time required by a traditional bank.

Key Factors to Compare When Choosing a Lender

Selecting a partner for your financing requires looking beyond the interest rate. You must evaluate how each lender handles the specific nuances of the Illinois market.

1. Loan-to-Value (LTV) Limits

The LTV determines how much leverage you can access. Most Chicago DSCR programs offer up to 80% LTV for purchases, though 75% is more common for cash-out refinances. High-leverage options allow you to keep more capital for your next acquisition.

2. Minimum DSCR Requirements

Lenders typically look for a ratio of 1.25x or higher. This means the gross rent is 25% higher than the monthly mortgage payment. However, some specialized lenders will go down to 1.00x or even offer "no-ratio" programs if you have a strong credit profile.

3. Prepayment Penalties

Understand the prepayment structure. Many DSCR loans include a "step-down" penalty (e.g., 5-4-3-2-1). If you plan to sell or refinance within a few years, a shorter penalty period is vital for your exit strategy.

4. Seasoning Requirements

If you are using the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat), seasoning is critical. Some lenders require you to own the property for 6 to 12 months before refinancing based on the new appraised value, while others allow for rapid refinancing.

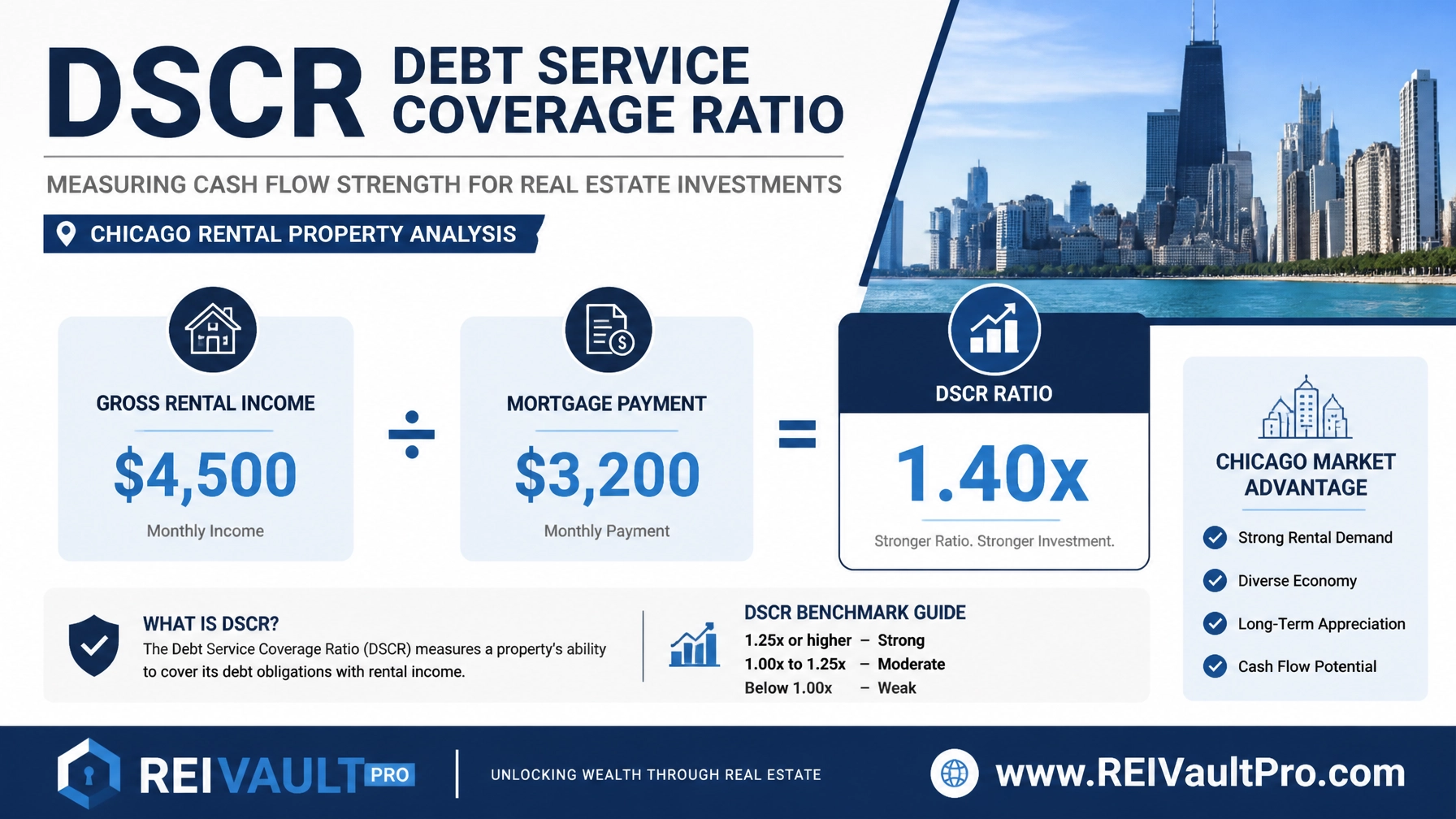

Practical Example: The Chicago 3-Flat Scenario

Consider a brick three-flat in Avondale purchased for $650,000.

- Gross Monthly Rent: $5,100

- Monthly PITIA (Principal, Interest, Taxes, Insurance, Association): $3,800

- Calculation: $5,100 / $3,800 = 1.34 DSCR

In this scenario, a DSCR of 1.34 is well above the typical 1.25 threshold. This strength would likely qualify you for the most competitive interest rates and a higher LTV. You can use the REI Vault Pro DSCR Calculator to run these numbers for your own potential deals.

Comparing Top DSCR Lenders for Chicago (2026)

The following lenders are active in the Chicago market and offer distinct advantages depending on your specific investment goals.

Renovo Financial

Renovo is a Chicago-based private lender with a deep understanding of local neighborhoods. They are highly active in the Midwest and are a top choice for residential investment properties throughout Illinois.

Constructive Capital

Known for high loan volume across the state, Constructive Capital offers streamlined long-term rental loans. They are often a fit for investors looking for standardized processes and competitive market share.

RCN Capital

RCN Capital excels at transitioning investors from fix-and-flip projects into long-term DSCR holds. Their bridge-to-rental programs are ideal if you are rehabilitating distressed Chicago properties.

LendingOne

This lender focuses on portfolio scaling. If you are looking to bundle multiple Chicago rentals into a single loan or scale quickly, their investor-focused model provides significant support.

Kiavi

Kiavi is recognized for its technology-driven approach. If you prioritize speed and a digital application process, they are often the fastest option for securing approval in a hot market.

How to Evaluate Your Chicago Deal

Before reaching out to a lender, you should perform your own underwriting. Understanding the "as-is" value and the potential rental income is essential for a smooth approval process.

Using professional tools like the AI Deal Analyzer allows you to simulate different financing scenarios. You can compare how a 7.5% interest rate versus an 8.2% rate affects your monthly cash flow and total ROI.

For properties requiring renovation, the AI Rehab Estimator helps you accurately project costs, ensuring your total investment stays within the lender's LTV guidelines.

Documentation Needed for a DSCR Loan

While you do not need personal tax returns, lenders still require specific documentation to verify the asset and your experience.

- Appraisal with Rent Schedule (Form 1007): This confirms the market rent for the property.

- Lease Agreements: If the property is currently occupied.

- Entity Documents: Most DSCR loans are closed in the name of an LLC or Corporation.

- Credit Report: Most lenders look for a score of 620 to 700+.

- Bank Statements: Usually two months of statements to verify your down payment and reserves.

Navigating the Chicago Market Complexity

Chicago has specific regulations, such as the Residential Landlord and Tenant Ordinance (RLTO), that influence how you manage properties. Lenders who understand these local laws are more likely to provide realistic underwriting.

When analyzing a deal in a new neighborhood, leverage the AI Market Analysis tool. It provides insights into local trends, vacancy rates, and price appreciation, helping you choose the best pockets for investment.

Related REI Vault Pro Resources

- AI Rent Analyzer: Use this tool to get accurate rental estimates for any Chicago zip code. This ensures your DSCR calculations are based on real-world data. Explore AI Rent Analyzer.

- AI Underwriting: Automate the review of your property’s financials to see if it meets typical lender criteria before you apply. Access AI Underwriting.

- AI Deal Scoring: Quickly rank multiple potential acquisitions based on their cash flow potential and risk profile. Jump into AI Deal Scoring.

- DSCR Calculator: A dedicated tool for calculating your debt service coverage ratio based on current Chicago interest rates and property taxes. Use the DSCR Calculator.

Finding the Right Financing Partner

Choosing the best Chicago DSCR loan lender involves balancing speed, cost, and long-term flexibility. A local specialist like Renovo might offer better neighborhood insight, while a national player like RCN Capital or Kiavi might offer more aggressive tech-driven timelines.

Always compare at least three quotes and pay close attention to the fine print regarding prepayment penalties and reserve requirements. By doing your homework and utilizing the right tools, you can secure the capital needed to grow your Chicago real estate portfolio.

Ready to see how your next deal stacks up? Watch a Demo of the REI Vault Pro platform today.

FAQ Section

What is the minimum credit score for a DSCR loan in Chicago?

Most lenders require a minimum credit score of 620, though you will typically find the most competitive interest rates and higher LTV options with a score of 700 or above.

Can I get a DSCR loan for a 4-unit building in Chicago?

Yes, DSCR loans are ideal for 1-4 unit residential properties. For buildings with 5 or more units, you would typically look at commercial DSCR or multifamily financing options.

How much down payment is required for a Chicago DSCR loan?

The standard down payment is 20% to 25%. Some lenders may offer 15% down for highly experienced investors with strong credit, but this usually comes with higher interest rates.

Do DSCR loans require personal income verification?

No. DSCR loans qualify the property based on its ability to generate rental income. You will not be asked for tax returns, pay stubs, or W-2s, making them an excellent choice for self-employed individuals.

How long does it take to close a DSCR loan?

Because they do not require extensive personal income underwriting, DSCR loans can often close in 21 to 30 days. Some tech-focused lenders can even close in as little as 14 days if the appraisal is completed quickly.