How to Age in Place Comfortably with a Reverse Mortgage (and Keep Your Keys!)

For many homeowners, the house is more than just four walls and a roof. It is where you raised your family, celebrated milestones, and built a lifetime of memories. As the years pass, the desire to stay in that familiar environment: often called "Aging in Place": becomes a top priority. However, the financial reality of retirement can sometimes make staying put feel difficult. Between property taxes, maintenance, and the potential need for in-home care, the costs add up quickly.

This is where a reverse mortgage enters the conversation. Far from the old myths of "the bank taking your home," a modern reverse mortgage is a strategic financial tool designed to help you access your home equity while you continue to live in and own your property.

Explore how you can leverage your home’s value to create a more comfortable, secure future without ever having to pack a single box.

What Does it Really Mean to Age in Place?

Aging in Place

Definition: The ability to live in one's own home and community safely, independently, and comfortably, regardless of age, income, or ability level.

Practical Benefit: It allows you to maintain your social connections and daily routines in a familiar setting while bringing necessary services to you instead of moving to an assisted living facility.

The biggest hurdle to successful aging in place is usually liquidity. You might be "house rich and cash poor," meaning you have hundreds of thousands of dollars in equity but struggle to cover monthly bills or unexpected medical expenses. By utilizing a Home Equity Conversion Mortgage (HECM), you can convert that dormant equity into usable funds.

Understanding the Reverse Mortgage Basics

A reverse mortgage is essentially a loan for homeowners aged 62 and older (though some private options allow for age 55) that requires no monthly mortgage payments. Instead of you paying the lender every month, the lender pays you. The loan is eventually repaid when the last surviving borrower moves out, sells the home, or passes away.

Principal Limit

Definition: The total amount of money a borrower can receive from a reverse mortgage after closing costs and liens are paid.

Practical Application: This figure determines your "bucket" of available cash for home repairs, daily living, or a line of credit.

Non-Recourse Loan

Definition: A loan where the borrower (or their heirs) will never owe more than the home’s fair market value at the time of sale.

Practical Benefit: This provides a safety net, ensuring that even if the housing market dips, you are protected.

HECM vs. Proprietary Reverse Mortgages: The Calculation Breakdown

To understand how much you can actually access, we have to look at the Loan-to-Value (LTV) ratios. The amount you can borrow is not 100% of your home's value. It is calculated based on the age of the youngest borrower, current interest rates, and the appraised value of the home.

1. The HECM (FHA-Insured)

The HECM is the most common reverse mortgage. It is insured by the Federal Housing Administration (FHA).

- Maximum Claim Amount (MCA): As of 2024, the FHA limits the home value it will consider to $1,149,825. If your home is worth $2 million, the HECM calculation only uses the first $1.15 million.

- LTV Calculation: Typically, a 72-year-old might see a Principal Limit Factor (PLF) of roughly 42-45% depending on interest rates.

2. Proprietary (Jumbo) Reverse Mortgages

For homeowners in high-value markets like Los Angeles, San Francisco, or Miami, a proprietary reverse mortgage might be a better fit.

- No FHA Limit: These loans can go up to $4 million or more in property value.

- LTV Calculation: While the LTV percentages are often slightly lower than HECMs (perhaps 30-38% for the same 72-year-old), they apply to the entire value of the home, not just the FHA cap.

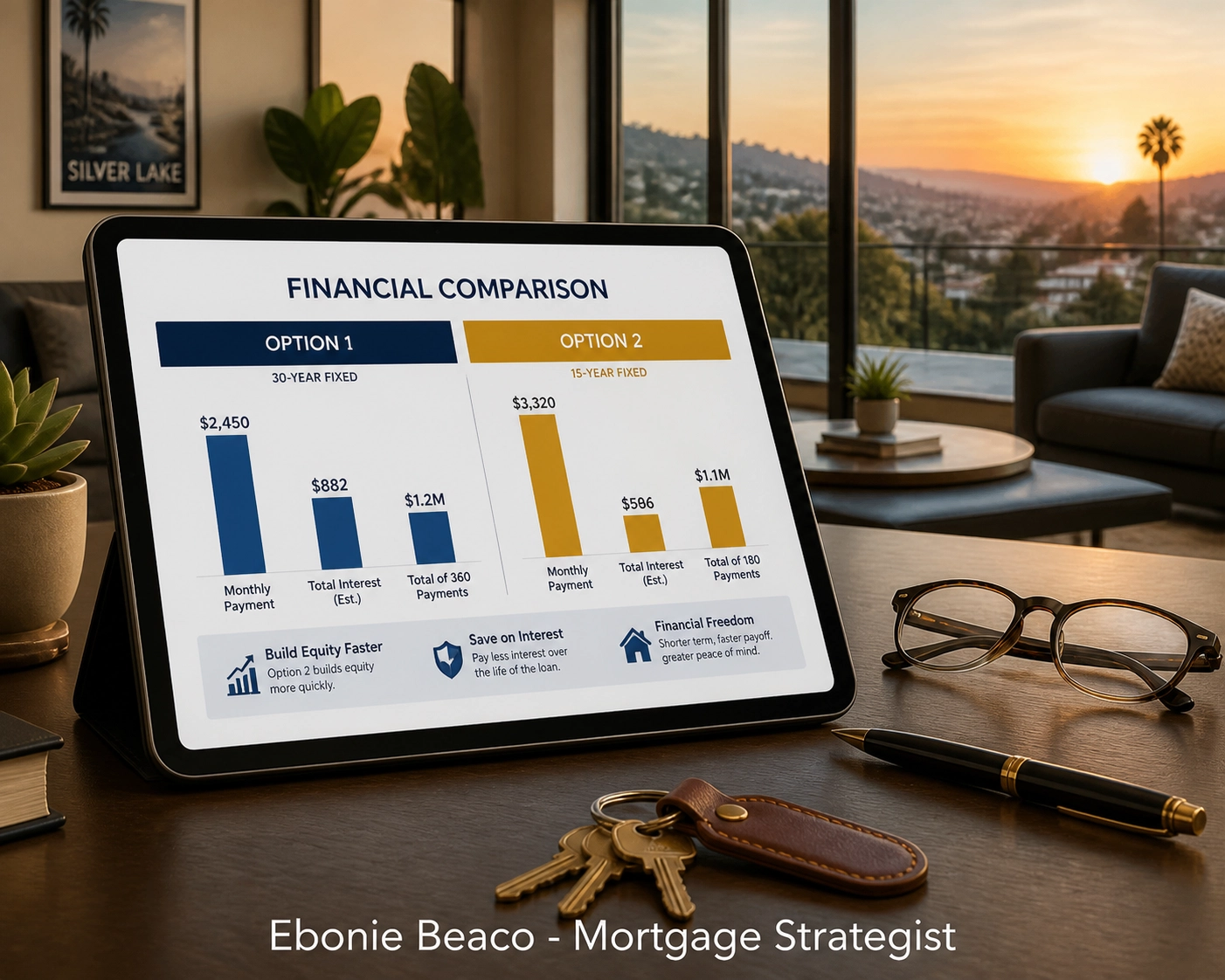

(Visual description: A side-by-side comparison chart showing a HECM loan calculation on a $1.2M home versus a Proprietary Jumbo loan on the same home, highlighting the difference in available funds.)

Case Study: Hana’s Plan for Independence in Los Angeles

Let's look at a real-world scenario. Meet Hana, a 73-year-old Japanese-American widow living in a beautiful home in the Silver Lake neighborhood of Los Angeles.

The Situation:

- Home Value: $1,250,000

- Existing Mortgage: $100,000

- Monthly Income: $2,800 (Social Security and a small pension)

- The Goal: Hana wants to remodel her bathroom for safety (walk-in tub) and hire a part-time caregiver so she can stay in her home.

The Strategy:

Hana chooses a Proprietary Reverse Mortgage because her home value exceeds the FHA limit, and the private loan offers lower upfront mortgage insurance premiums.

The Calculation:

- Age: 73

- LTV Percentage: 38%

- Gross Principal Limit: $475,000 ($1,250,000 x 0.38)

- Mandatory Payoff: -$100,000 (To clear her existing mortgage)

- Closing Costs: -$15,000 (Estimated)

- Net Available Funds: $360,000

Hana uses $40,000 immediately for home modifications. She places the remaining $320,000 into a line of credit. Because she no longer has a $1,200 monthly mortgage payment, her cash flow effectively increases by that amount, and she has a massive "rainy day" fund for her future care.

How to Use Your Funds to Enhance Your Quality of Life

Once you have secured your reverse mortgage, the question is how to best use the money to stay safe and comfortable.

Eliminate Existing Monthly Payments

The first requirement of a reverse mortgage is paying off any existing liens. By removing your monthly mortgage payment, you immediately increase your monthly disposable income. This extra cash can be used for groceries, utilities, and travel to visit grandchildren in Michigan or Florida.

Home Modifications for Longevity

Safety is a huge component of aging in place. Many homeowners use their home equity to:

- Install ramps or stairlifts.

- Update lighting to prevent falls.

- Widen doorways for wheelchair or walker access.

- Convert a bathtub into a zero-threshold shower.

Covering In-Home Care Costs

According to recent surveys, the cost of a full-time assisted living facility can be staggering. hiring a part-time in-home health aide is often more affordable and preferred by seniors. A reverse mortgage line of credit allows you to pay for these services as needed, ensuring you get help with meals, medication, or mobility without moving.

"Keeping Your Keys": The Rules of the Road

The most common fear is that the bank will "take the house." This is simply not true as long as you follow the basic rules of the loan. You remain the owner of the home. To keep your keys and stay in good standing, you must fulfill three main obligations:

- Occupancy: The home must remain your primary residence. You can travel or visit family, but you cannot live elsewhere for more than 12 consecutive months (for example, in a rehab facility).

- Property Taxes and Insurance: You must stay current on your property taxes and homeowners insurance. Failure to do so can result in the loan becoming due.

- Maintenance: You are responsible for keeping the home in good repair. This is why using some of the loan proceeds for a new roof or HVAC system is often a smart move.

As long as you meet these requirements, you can stay in your home for the rest of your life, regardless of how high the loan balance grows or what happens to the market.

Is a Reverse Mortgage Right for You?

While the benefits are significant, a reverse mortgage is a big decision that requires looking at the long-term picture. It is often a great fit if:

- You plan to stay in the home for at least 5 to 10 years.

- You have significant equity (at least 50%).

- You want to preserve other retirement assets, like your 401(k), by using home equity for large expenses.

If you are considering this path, the first step is always education. You can use mortgage calculators to get a rough idea of your numbers, but a 1-on-1 consultation is the best way to see the specific programs available in your state: whether you are in Illinois, Virginia, or California.

Taking the Next Step Toward Comfort

Aging in place is about more than just staying in a building; it is about maintaining your independence and your dignity. By strategically using the wealth you have built in your home, you can create a safety net that protects you for decades to come.

Whether you are looking to renovate, pay for care, or simply enjoy a stress-free retirement, your home equity can be the key to your peace of mind.

Jump in and explore your options today. You have worked hard for your home: now it is time for your home to work for you.

If you have questions about how a reverse mortgage calculation would look for your specific property, reach out for a clear, no-pressure strategy session.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664