How to Adjust Your Homebuying Strategy Based on Today’s Mortgage Market Update (May 30 Edition)

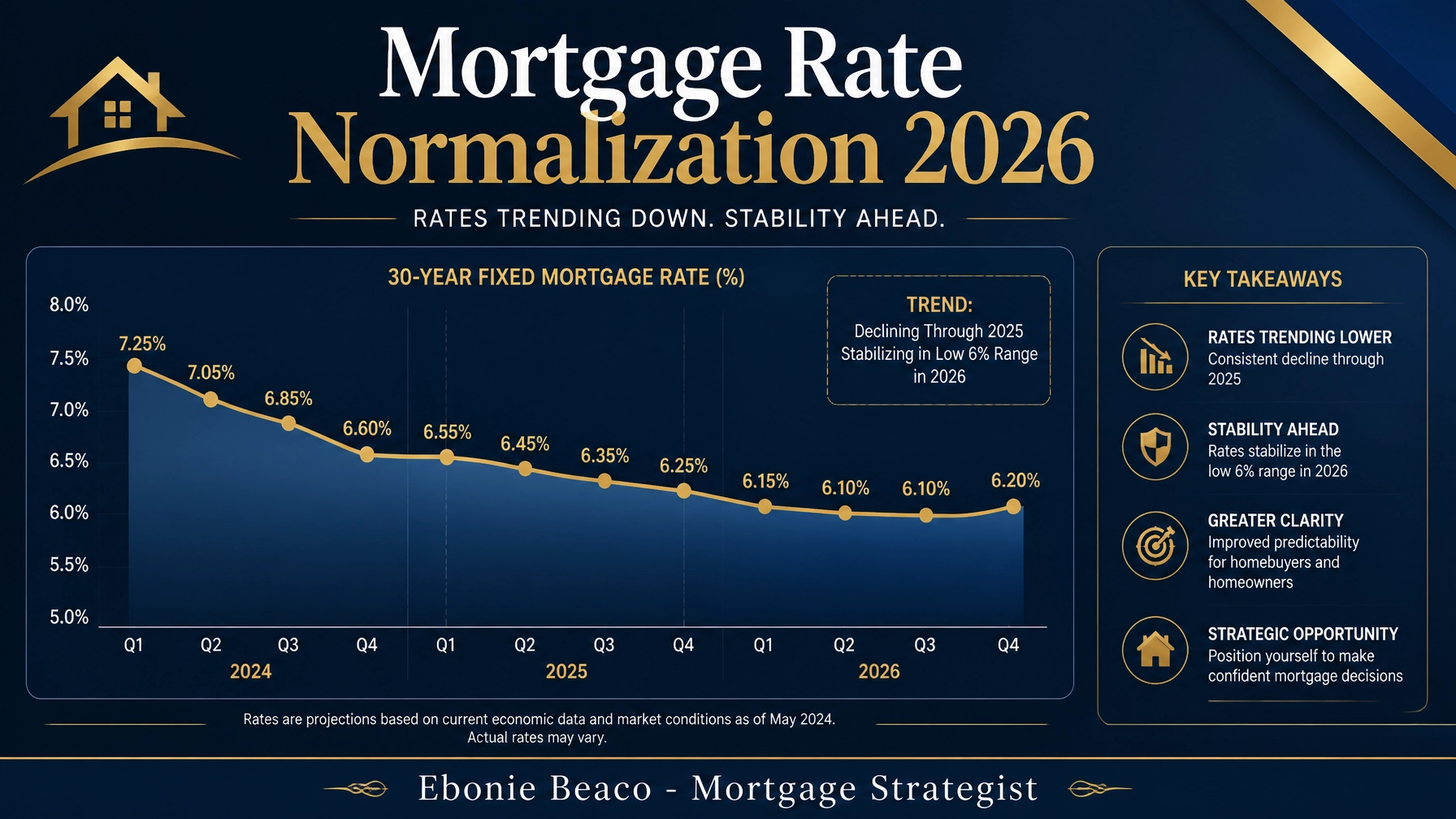

The mortgage market landscape on this Saturday, May 30, 2026, continues to show signs of a measured normalization that has defined the first half of the year. After several years of significant volatility, the current stability in interest rates provides a unique window for homebuyers and investors to execute long term strategies with greater confidence. While we are no longer seeing the ultra low rates of the early 2020s, the current plateau in the low 6 percent range offers a much more predictable environment than the previous peaks above 7 percent. This environment requires a shift from the wait and see approach to a more proactive strategy that leverages current equity and specific loan programs designed for modern market conditions. Understanding these shifts is essential for anyone looking to acquire property or optimize their current real estate portfolio in states like Illinois, Florida, or California.

Current Market Reality and Rate Stability

As we close out the month of May, the 30 year fixed mortgage rate has stabilized around 6.25 percent for top tier borrowers, reflecting a broader trend of cooling inflation and consistent Federal Reserve policy. This stability is a welcome departure from the rapid fluctuations of the past 24 months, allowing buyers to calculate their purchasing power with significantly less fear of a sudden rate hike during the escrow process. According to the latest research from Fannie Mae, this environment of gradual normalization is expected to persist through the summer months as housing inventory slowly increases across major metropolitan areas. For residents in high demand markets like Chicago, Atlanta, and Northern Virginia, this means the competition remains steady but the panic driven bidding wars of previous years have largely subsided.

Strategic Shifts for Residential Homebuyers

For those looking to purchase a primary residence, the focus should move toward finding the right property rather than timing the absolute bottom of the interest rate cycle. Many buyers are discovering that the slight decrease in rates over the last year has unlocked significant purchasing power, making formerly out of reach homes more accessible. Utilizing programs like down payment assistance or conventional loans with competitive pricing can help bridge the gap for first time buyers in Arkansas, Alabama, and Indiana. It is also a prime time to explore rate term refinancing for those who purchased properties when rates were at their highest point in 2024. By securing a pre approval today, you can position yourself to act quickly when the right home hits the market in a still competitive spring season.

Advanced Strategies for Real Estate Investors

Real estate investors are finding renewed opportunities in the current market by focusing on cash flow and portfolio scalability rather than short term appreciation. The DSCR (Debt Service Coverage Ratio) loan remains one of the most effective tools for landlords looking to acquire rental properties without the constraints of personal income verification. Because these loans focus on the income generated by the property itself, investors can continue to expand their holdings in lucrative markets such as Florida and Georgia. Furthermore, the fix and flip market has seen a resurgence as inventory levels provide more opportunities for distressed property acquisitions that can be renovated and sold or held as long term rentals. Investors are also looking closely at Airbnb and short term rental financing in vacation destinations throughout Virginia and Kentucky to capitalize on the summer travel surge.

Technical Definitions for Market Participants

- DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its debt payments based on its gross rental income.

- HELOC (Home Equity Line of Credit): A revolving credit line that allows homeowners to borrow against the equity in their home as needed, often used for renovations or further investments.

- Non-QM (Non-Qualified Mortgage): A category of loans that do not meet the standard criteria of government backed agencies, often used by self employed borrowers or those with complex income structures.

- LTV (Loan-to-Value): The ratio of the loan amount to the appraised value of the property, which determines the amount of equity required for a transaction.

- Cash-Out Refinance: A mortgage refinancing option where the new loan is larger than the existing one, allowing the borrower to take the difference in cash.

Leveraging Home Equity for Portfolio Growth

Homeowners who have seen their property values rise over the last several years are increasingly looking at equity extraction strategies to fund new investments or home improvements. A cash out refinance or a HELOC can provide the necessary capital to purchase a second home, fund a renovation, or even consolidate higher interest debt. In states like California and Michigan, where equity growth has been particularly robust, these strategies allow homeowners to put their idle wealth to work. By accessing equity now, you can lock in a stable rate and use those funds to acquire income producing assets that will continue to build wealth over time. This approach is particularly effective for those following the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy to scale their rental portfolios quickly and efficiently.

Practical Financial Example: Unlocking Home Equity

To illustrate how a homeowner might utilize their equity in today’s market, let’s look at a typical scenario for a resident in a mid sized city in Illinois or Missouri. Consider a homeowner with a primary residence valued at $550,000 who currently owes $300,000 on their existing mortgage. Under a standard 80 percent LTV (Loan to Value) guideline for a cash out refinance, the maximum total loan amount would be $440,000. After paying off the existing $300,000 mortgage and accounting for estimated closing costs, the homeowner could walk away with approximately $130,000 in liquid cash. This capital could then be used as a 20 percent down payment on a $500,000 investment property, effectively turning one home into two and doubling the homeowner's real estate footprint.

Regional Market Insights: Illinois to Virginia

The impact of these mortgage market updates varies significantly depending on the specific region and local inventory levels. In Chicago, the demand for multi unit buildings remains high as investors seek to provide housing in a market with a strong rental base. Florida continues to see high interest in both residential purchases and commercial development, supported by a steady influx of new residents from other states. Virginia and Georgia are showing strong growth in suburban markets where families are looking for larger homes and more space while still maintaining proximity to major employment hubs. According to data from Freddie Mac, the Southeast region is expected to lead the country in total home sales volume through the end of 2026.

Conclusion: Planning Your Next Move

Adapting your homebuying or investment strategy to the May 30 mortgage market update requires a balance of patience and decisive action. While the era of 3 percent interest rates is behind us, the current stability in the low 6 percent range offers a sustainable path for building long term wealth through real estate. Whether you are a first time homebuyer in Indiana or a seasoned investor in California, the key is to align your financing with your specific financial goals and risk tolerance. By staying informed on the latest trends and working with a strategist who understands the nuances of various loan programs, you can navigate this market with clarity and confidence. The opportunities for growth are present for those who are prepared to act on the data and leverage the tools available in today's lending environment.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664