How the New 2026 Conventional Loan Limit Influences Your Strategy: Today’s Market News Update

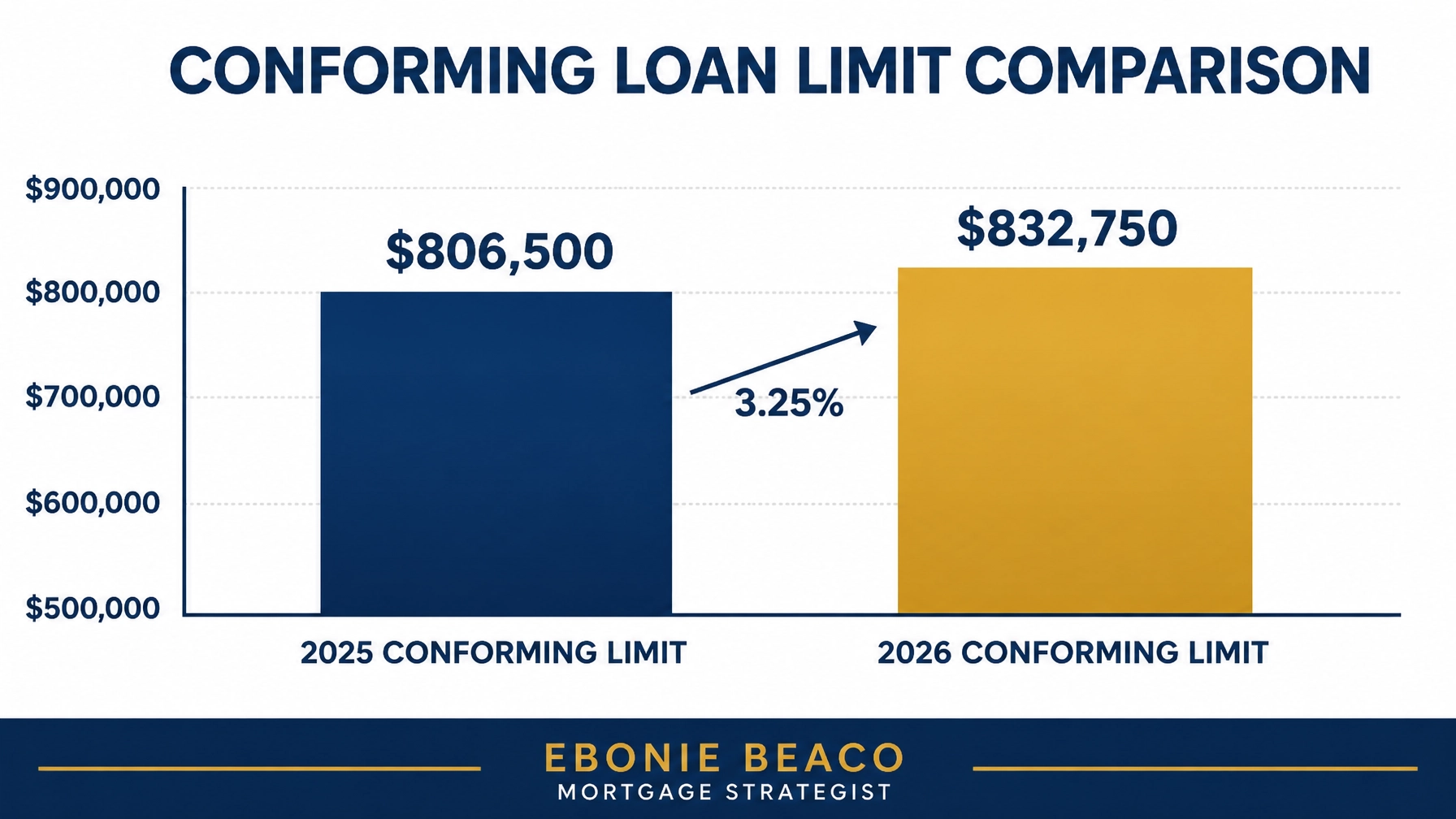

The mortgage landscape recently shifted with the announcement of the 2026 conforming loan limits. Every year, the Federal Housing Finance Agency (FHFA) adjusts these limits based on house price changes to ensure financing stays accessible for the average borrower. For 2026, the baseline limit for a single-unit property has officially increased to $832,750 across most of the United States.

This update reflects a 3.26 percent increase from the 2025 limit of $806,500. This change is not just a technicality; it directly impacts your purchasing power and the types of loan products available to you. By understanding these new caps, you can better navigate the housing markets in California, Florida, Virginia, and beyond.

Defining Conforming Loan Limits

Conforming loan limits are the maximum dollar amounts for mortgages that Fannie Mae and Freddie Mac can purchase. These limits are set annually by the FHFA to keep pace with national home price appreciation. When a loan "conforms" to these standards, it typically offers more competitive interest rates and flexible underwriting compared to non-conforming options.

Staying within these limits allows you to access conventional financing programs that often require lower down payments. For many homeowners and investors, keeping a loan amount below the conforming threshold is a primary goal to avoid the stricter requirements of jumbo financing.

The 2026 Baseline vs. High-Cost Areas

The baseline limit of $832,750 applies to the majority of counties in states like Alabama, Arkansas, Indiana, and Michigan. However, in designated high-cost areas, the limit can reach as high as $1,249,125 for a single-family home. These high-cost designations are common in metropolitan regions where home prices significantly exceed the national average.

In states like California and parts of Florida and Virginia, these higher caps are essential. They allow borrowers in expensive markets to utilize conventional loan benefits for properties that would otherwise require a jumbo mortgage. You can find detailed breakdowns of these county-specific limits on the FHFA official website.

Why the New Limits Influence Your Purchasing Power

Increased loan limits mean you can finance a larger portion of a home's price without crossing into jumbo territory. For example, a buyer looking at a $900,000 property in a standard-cost county can now put down a smaller percentage while remaining within conforming guidelines. This shift effectively lowers the barrier to entry for higher-priced homes.

Consider a scenario where you are purchasing a home for $900,000. With the new 2026 limit of $832,750, your required down payment to stay within a conventional loan is significantly lower than it was in previous years. This allows you to keep more cash in your pocket for renovations or other investments.

Practical Example: Purchasing a $900,000 Home

Let's look at how the numbers work for a standard purchase in 2026.

- Purchase Price: $900,000

- Down Payment: $70,000 (Approx. 7.7%)

- Loan Amount: $830,000

- Result: This loan qualifies for 2026 conventional limits.

In 2025, this same $830,000 loan would have exceeded the baseline limit of $806,500. The borrower would have been forced to either increase their down payment by $23,500 or apply for a jumbo loan, which often comes with higher interest rates and more stringent credit score requirements.

Conforming Loans vs. Jumbo Loans

Jumbo loans are mortgages that exceed the conforming limits set by the FHFA. Because Fannie Mae and Freddie Mac cannot buy these loans, lenders take on more risk and typically enforce tougher rules. This might include a higher minimum credit score, larger reserve requirements, and a lower debt-to-income (DTI) ratio.

By using the new 2026 limits, you may avoid these hurdles. Conventional loans often allow for a higher DTI and lower loan-to-value (LTV) ratios. If you are a self-employed borrower or an investor, staying within the conventional loan programs can make the approval process much smoother.

High-Balance Strategies in California and Virginia

For residents in high-cost counties like Los Angeles, Orange County, or Northern Virginia, the "high-balance" conforming limit is a vital tool. The 2026 cap of $1,249,125 provides a massive window for financing premium real estate with conventional terms. This is particularly relevant for those looking at luxury condos or single-family residences in sought-after neighborhoods.

Investors focusing on these regions can leverage high-balance loans to acquire high-value rental properties. By using a DSCR (Debt Service Coverage Ratio) loan or a high-balance conventional mortgage, you can scale your portfolio even in expensive markets.

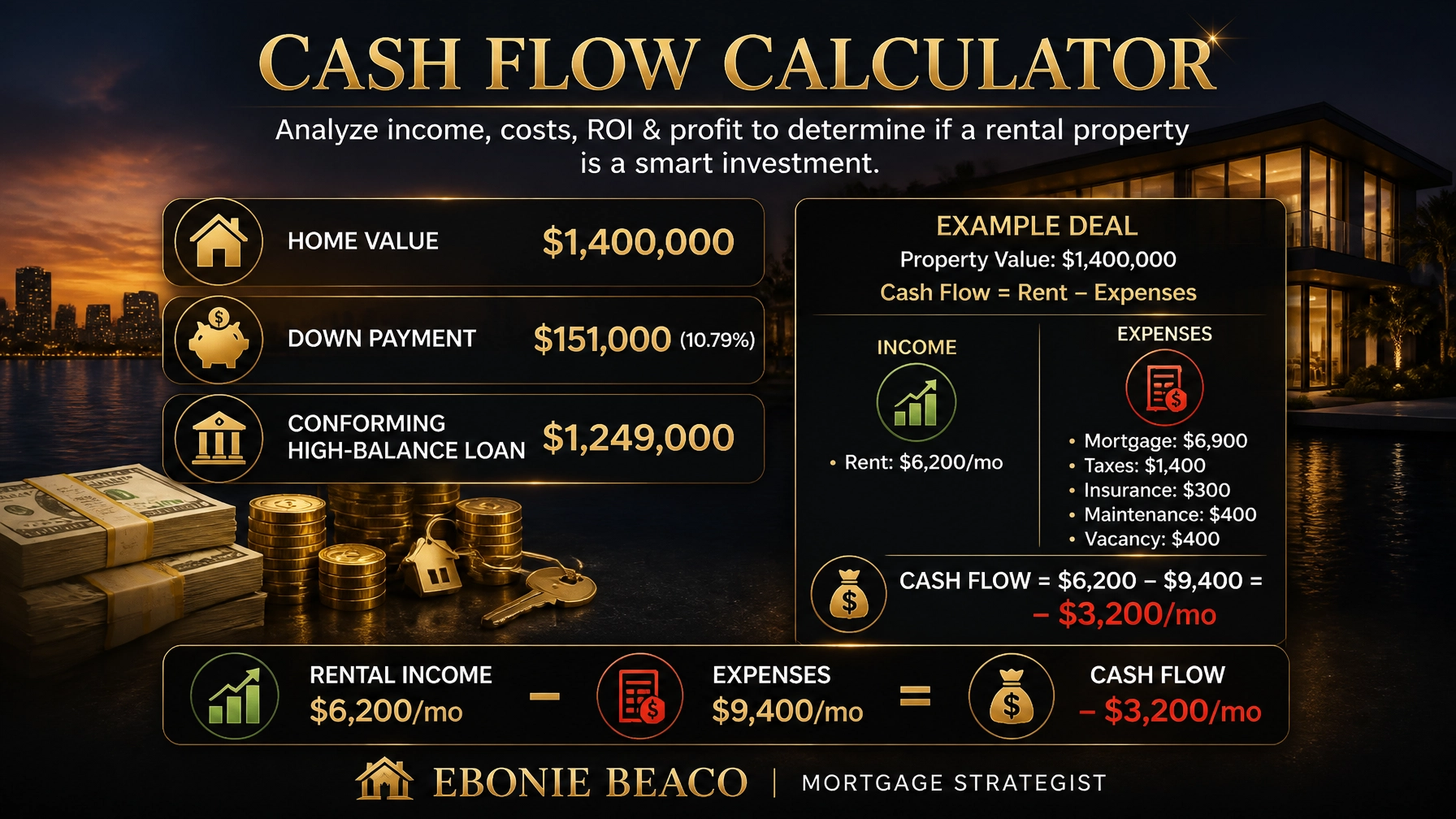

Financial Calculation for High-Cost Markets

Imagine an investor purchasing a luxury rental property in a high-cost area.

- Home Value: $1,400,000

- Down Payment: $151,000 (Approx. 10.8%)

- Conforming High-Balance Loan: $1,249,000

- Result: The loan stays within the 2026 high-cost ceiling.

This scenario demonstrates how the increased ceiling supports high-value transactions. Previously, a loan of this size would likely have required a 20% down payment or a more complex jumbo underwriting process. Now, the investor can secure the asset with more leverage.

Impact for First-Time Homebuyers

First-time homebuyers often struggle with the balance between rising home prices and down payment savings. The 3.26 percent increase in limits provides a much-needed cushion. It ensures that as prices appreciate in states like Georgia, Illinois, and Missouri, the available loan amounts move in tandem.

Accessing down payment assistance alongside a conventional loan can be a powerful combination. Many of these assistance programs are specifically designed to work with conforming loans, making the 2026 update even more significant for those entering the market.

Opportunities for Real Estate Investors

Investors should view the higher limits as an opportunity to refinance or acquire new properties with better terms. If you have a property currently financed with a high-interest jumbo loan, you might now be able to refinance it into a lower-rate conventional loan if your balance falls under the new limits.

Furthermore, these limits apply to 2-unit, 3-unit, and 4-unit properties with even higher caps. For instance, a 4-unit property in a standard area now has a limit of $1,601,750. This is a game-changer for investors using the house-hacking strategy or building a multi-unit portfolio.

Key Technical Terms to Know

- DTI (Debt-to-Income Ratio): A percentage of your gross monthly income that goes toward paying debts.

- LTV (Loan-to-Value Ratio): The relationship between the loan amount and the appraised value of the property.

- Non-QM (Non-Qualified Mortgage): Loans that do not meet the standard conforming criteria, often used by self-employed borrowers.

- DSCR (Debt Service Coverage Ratio): A metric used to qualify rental property loans based on the property's income rather than the borrower's personal income.

How to Navigate Your Next Move

The shift in loan limits is just one piece of the real estate puzzle in 2026. Whether you are looking at home purchase options or considering a home refinance, these new figures provide a clear advantage.

Compare your current loan balance or your target home price against these new limits. You may find that your financing options have expanded significantly overnight. Our team is here to help you analyze these scenarios and choose the best path forward for your financial goals.

Explore your options and see how these new limits can benefit your strategy.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664