Home Equity Secrets Revealed: What Your Bank Isn't Telling You About HELOCs in Florida and Georgia

You have probably seen the mailers. Your local big-box bank sent a glossy postcard promising a "low-rate" line of credit to fix up your kitchen or consolidate that pesky credit card debt. In high-growth markets like Florida and Georgia, these offers are everywhere.

But there is a side to the Home Equity Line of Credit (HELOC) world that rarely makes it onto a postcard. As a mortgage strategist, I see the fine print that catches homeowners off guard. Whether you are looking for a Michigan HELOC lender to fund a renovation or exploring options as a Virginia HELOC lender for your next investment, understanding the "why" behind the numbers is essential.

Explore the mechanics of equity, the hidden clauses banks use to protect themselves, and how you can use these tools to build actual wealth.

The Revolving Credit Reality: What a HELOC Actually Is

Home Equity Line of Credit (HELOC): A revolving credit facility secured by the equity in your real estate, allowing you to borrow, repay, and borrow again during a set period.

Practical application: You treat your home equity like a high-limit credit card, but with interest rates that are typically much lower because the loan is secured by your property.

Most people understand the basic concept, but they miss the nuance of the "Draw Period" versus the "Repayment Period." During the first 10 years (the typical draw period), you often only pay interest on what you spend. Once that ends, the loan enters a 20 year repayment period where you must pay back both the principal and the interest.

If you aren't prepared for that payment jump, your monthly budget could take a massive hit. Transparency in these timelines is something we prioritize at Home Loans Network.

The Secret Florida and Georgia Banks Keep About Appraisals

In fast-moving markets like Miami, Orlando, Atlanta, and Savannah, property values can fluctuate rapidly. When you apply for a HELOC, the bank uses an appraisal to determine your "Combined Loan-to-Value" (CLTV).

Combined Loan-to-Value (CLTV): The ratio of all loans on a property (first mortgage plus the HELOC limit) compared to the appraised value of the home.

Practical application: If your home is worth $500,000 and you owe $300,000 on your primary mortgage, a lender allowing an 85% CLTV would let you have a total debt of $425,000, meaning a HELOC of $125,000.

The "secret"? Many retail banks use "Desktop Appraisals" or AVMs (Automated Valuation Models) that might undervalue your home in a hot neighborhood. If the computer says your house is worth less than it actually is, your credit line shrinks. An expert strategist knows how to push for a full appraisal when the data supports a higher value, ensuring you access every bit of equity you deserve.

The Hidden Clause That Could Freeze Your Funds Overnight

This is the one that keeps homeowners up at night once they hear about it. Almost every HELOC agreement contains a clause that allows the bank to "freeze" or "reduce" your line of credit if the value of your home drops significantly.

Imagine you are in the middle of a $100,000 renovation in Virginia. You’ve spent $50,000. Suddenly, the market dips, and your Virginia HELOC lender sends a notice saying your line is frozen. You are stuck with a half-finished kitchen and no way to pay the contractor.

We see this often with big national banks that are quick to mitigate risk. Working with a specialized network allows you to compare loan programs that might have more flexible terms or different risk appetites.

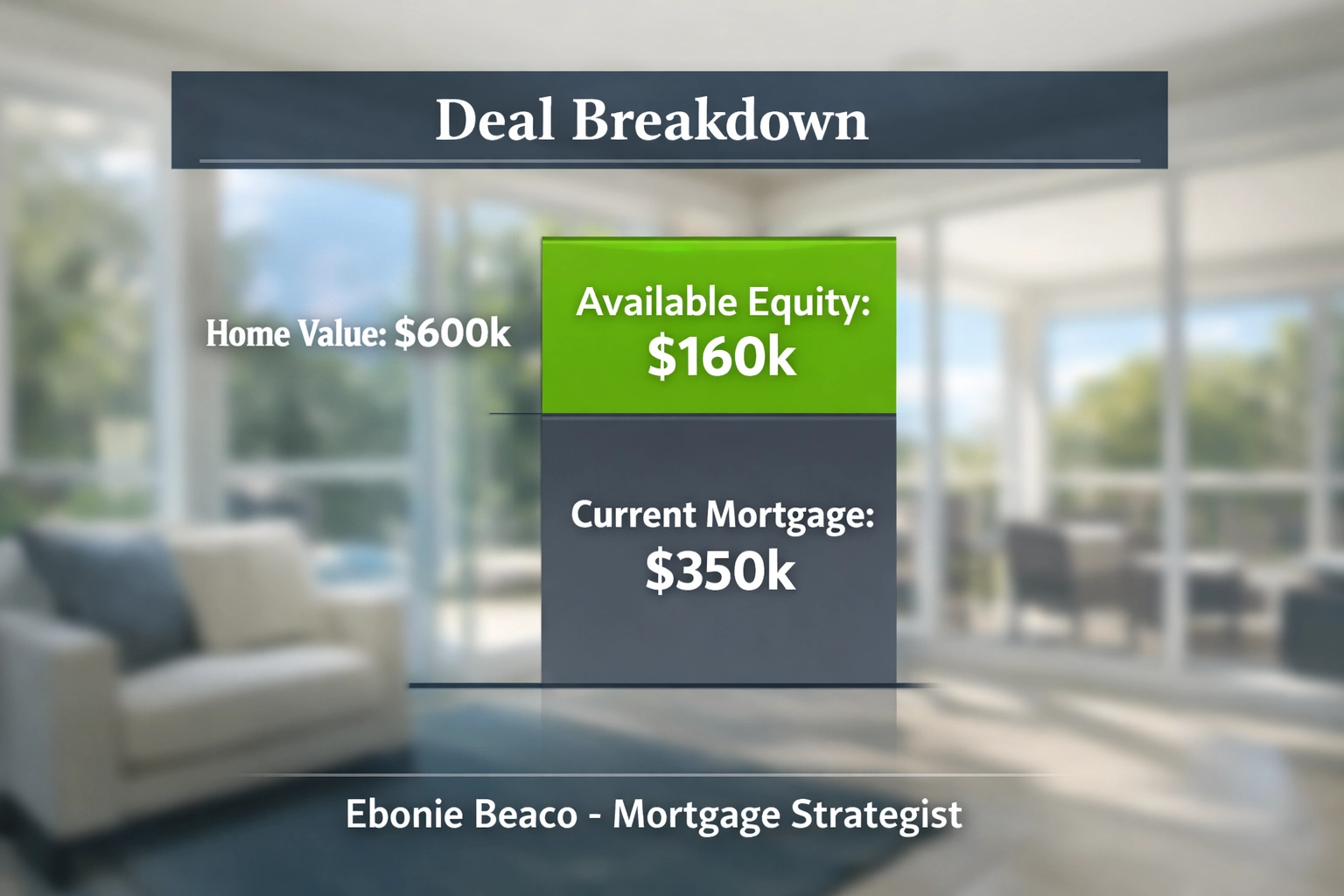

How the Math Works: A Real-World Florida Scenario

Let’s look at a practical example for a homeowner in Tampa or Jacksonville. Understanding the numbers helps you visualize the potential of your equity.

Scenario: The Equity Extraction Strategy

- Property Value: $600,000

- Current Mortgage Balance: $350,000

- Max CLTV Offered: 85%

- Total Allowable Debt: $510,000 ($600,000 x 0.85)

- Available HELOC Limit: $160,000 ($510,000 - $350,000)

In this scenario, the homeowner has $160,000 of "ready-to-use" cash. If they use $50,000 to pay off high-interest debt at 24% APR and move it to a HELOC at 8% or 9% APR, the monthly savings are substantial. Accessing this via online forms is the first step toward restructuring your personal balance sheet.

The "Investor Secret": Using HELOCs for the BRRRR Method

If you are a real estate investor in Michigan or Indiana, you know that timing is everything. A HELOC on your primary residence is one of the most powerful tools for the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy.

Investors use the HELOC as "cash" to buy a distressed property quickly. Because you already have the line of credit, you don't have to wait for a new loan approval to close a deal. Once the investment property is renovated and rented, you do a cash-out refinance on that property to pay back the HELOC on your primary home.

This creates a self-funding cycle of wealth. Whether you are looking for a Michigan HELOC lender to start this journey or you are scaling a portfolio in Alabama or Missouri, the strategy remains the same: use equity to create more equity.

Why Your Bank Doesn't Want You to Know About DSCR Loans

When you go to a traditional bank for a HELOC on an investment property, they often say "no." Most big banks only want to lend on primary residences. They want you to think your only option is a high-interest personal loan.

In reality, there are specialized programs like DSCR (Debt Service Coverage Ratio) Loans.

Debt Service Coverage Ratio (DSCR): A calculation used by lenders to determine if an investment property's rental income covers its debt obligations (mortgage, taxes, insurance).

Practical application: If the rent is $2,000 and the mortgage is $1,500, the DSCR is 1.33. Lenders love seeing a ratio over 1.2.

If you can't get a HELOC on a rental, you might be better off with a DSCR cash-out refinance. This allows you to pull equity out of the investment property itself based on the income it generates, rather than your personal income or your primary home's equity.

The Variable Rate Trap: Is Your Payment About to Skyrocket?

Most HELOCs have variable interest rates tied to the Prime Rate. This is great when rates are falling, but it can be dangerous when they rise.

Banks love variable rates because the risk sits entirely on your shoulders. If the Fed raises rates, your payment goes up automatically.

Jump in and ask about "Fixed-Rate Segments." Some modern HELOC products allow you to lock in a portion of your balance at a fixed interest rate. This gives you the flexibility of a line of credit with the security of a traditional fixed-rate loan. It is a hybrid strategy that many retail bank employees aren't even trained to offer.

Navigating the Process Across the Map

Whether you are in Chicago, Illinois, or rural Kentucky, the mortgage basics remain consistent, but the local market knowledge changes. Florida and Georgia have specific closing costs and taxes that differ from Indiana or Arkansas.

- California and Virginia: High-value markets where equity builds fast.

- Michigan and Ohio: Great areas for utilizing equity for home improvements that add significant resale value.

- Florida and Georgia: Prime locations for using HELOCs to fund short-term rental (Airbnb) down payments.

Before you sign on the dotted line with a local branch, check our FAQ to see how these programs actually function in your specific state.

Compare Your Options Before You Commit

The biggest secret of all? The first offer you get is rarely the best one. Banks have "buckets" of money they need to lend out, and their rates change based on how full those buckets are.

By working with a strategist who understands the landscape across AL, AR, CA, FL, GA, IL, IN, KY, MI, MO, and VA, you gain access to a broader range of products. You might find that a Jumbo Loan or a simple refinance is actually a better fit for your goals than a HELOC.

Don't leave your equity to chance. Your home is likely your largest asset; treat the debt attached to it with the same respect you treat your investments.

Schedule a 1 on 1 to discuss your equity strategy:

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664 Book an Appointment