Home Equity Line of Credit (HELOC): Primary vs. Rentals

For many property owners in markets like Chicago, Miami, or Los Angeles, equity is often the most significant untapped asset in their financial portfolio. Whether you are living in your home or renting it out to tenants, that equity represents a powerful tool for wealth building.

A Home Equity Line of Credit, or HELOC, functions as a revolving credit line secured by the value of your property. Think of it like a credit card with a much lower interest rate, where your house acts as the collateral. However, the rules of the game change significantly depending on whether the property is your primary residence or an investment property.

Defining Key HELOC Terminology

Before diving into the strategic differences, it is essential to understand the technical metrics lenders use to evaluate your equity.

HELOC (Home Equity Line of Credit): A flexible loan that allows you to borrow against the equity in your home up to a predetermined limit, repay it, and borrow again. Practical Application: You can use this to fund a renovation or provide a down payment on a new investment property without liquidating your current assets.

LTV (Loan-to-Value Ratio): The relationship between the amount of money you owe on a mortgage and the current market value of the property. Practical Application: This ratio determines the maximum amount of equity a lender will allow you to access.

CLTV (Combined Loan-to-Value): The total of all loans on a property (first mortgage plus the HELOC) divided by the property value. Practical Application: Lenders use this to ensure there is still a "buffer" of equity left in the home to protect against market fluctuations.

DTI (Debt-to-Income Ratio): A personal finance measure that compares your monthly debt payments to your gross monthly income. Practical Application: This helps a lender decide if you can afford the additional monthly payment of a new line of credit.

The Primary Residence HELOC: The Low-Hanging Fruit

For most homeowners in states like Michigan, Virginia, or Georgia, the primary residence HELOC is the most accessible form of equity financing. Because you live in the home, lenders view the loan as lower risk. If financial trouble hits, people are more likely to prioritize their own roof over an investment property.

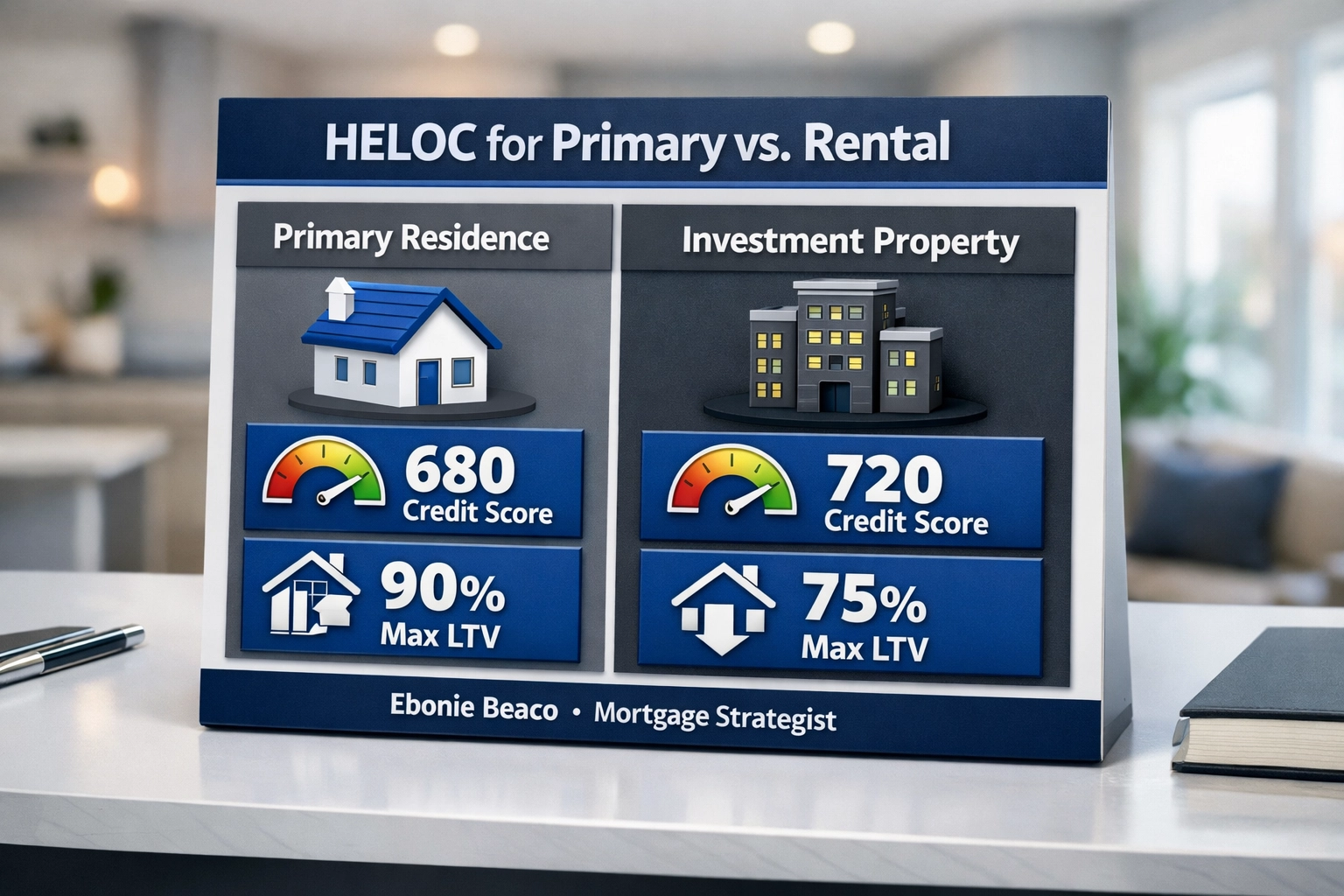

Maximum LTV Guidelines On a primary residence, lenders are often willing to go as high as 85% to 90% CLTV. This means if your home is worth $500,000, you might be able to have total debt (first mortgage + HELOC) up to $450,000.

Credit Score Requirements Typically, a score of 680 is the baseline for a primary HELOC. Higher scores will naturally yield better interest rates and higher credit limits.

Interest Rates Rates on primary HELOCs are usually based on the Prime Rate plus a small margin. These are generally the lowest rates available for any equity-based product.

HELOC for Investment Properties: The Pro-Level Strategy

If you are a landlord in Florida or an investor using the BRRRR method in Alabama, you might want to tap into the equity of your rental portfolio. While more difficult to obtain, an investment property HELOC is a game-changer for scaling.

Stricter Requirements Lenders view rental properties as higher risk. If a tenant stops paying rent, the mortgage payment relies solely on the owner's personal reserves. Consequently, the barriers to entry are higher.

Maximum LTV Guidelines You will rarely see a lender go above 75% or 80% CLTV on a rental property. They require a larger equity "cushion" to offset the risk of vacancy or property damage.

Credit Score and Reserves Expect to need a credit score of 720 or higher. Furthermore, lenders often require 6 to 12 months of cash reserves for all properties you own to ensure you can handle a period of zero rental income.

Interest Rate Premium Investors should expect to pay roughly 1% to 2% more in interest than they would for a primary residence line of credit.

Visual Description: A comparison table showing 'Primary Residence' vs 'Investment Property' requirements. Primary: 680 Score, 90% Max LTV. Investment: 720 Score, 75% Max LTV. Image Title: HELOC for Primary vs. Rental. Bottom text: Ebonie Beaco - Mortgage Loan Officer.

Visual Description: A comparison table showing 'Primary Residence' vs 'Investment Property' requirements. Primary: 680 Score, 90% Max LTV. Investment: 720 Score, 75% Max LTV. Image Title: HELOC for Primary vs. Rental. Bottom text: Ebonie Beaco - Mortgage Loan Officer.

Real-World Financial Examples

To see how these strategies function in the wild, let's look at two scenarios involving homeowners and investors in the current market.

Scenario 1: Accessing Equity in a Primary Home

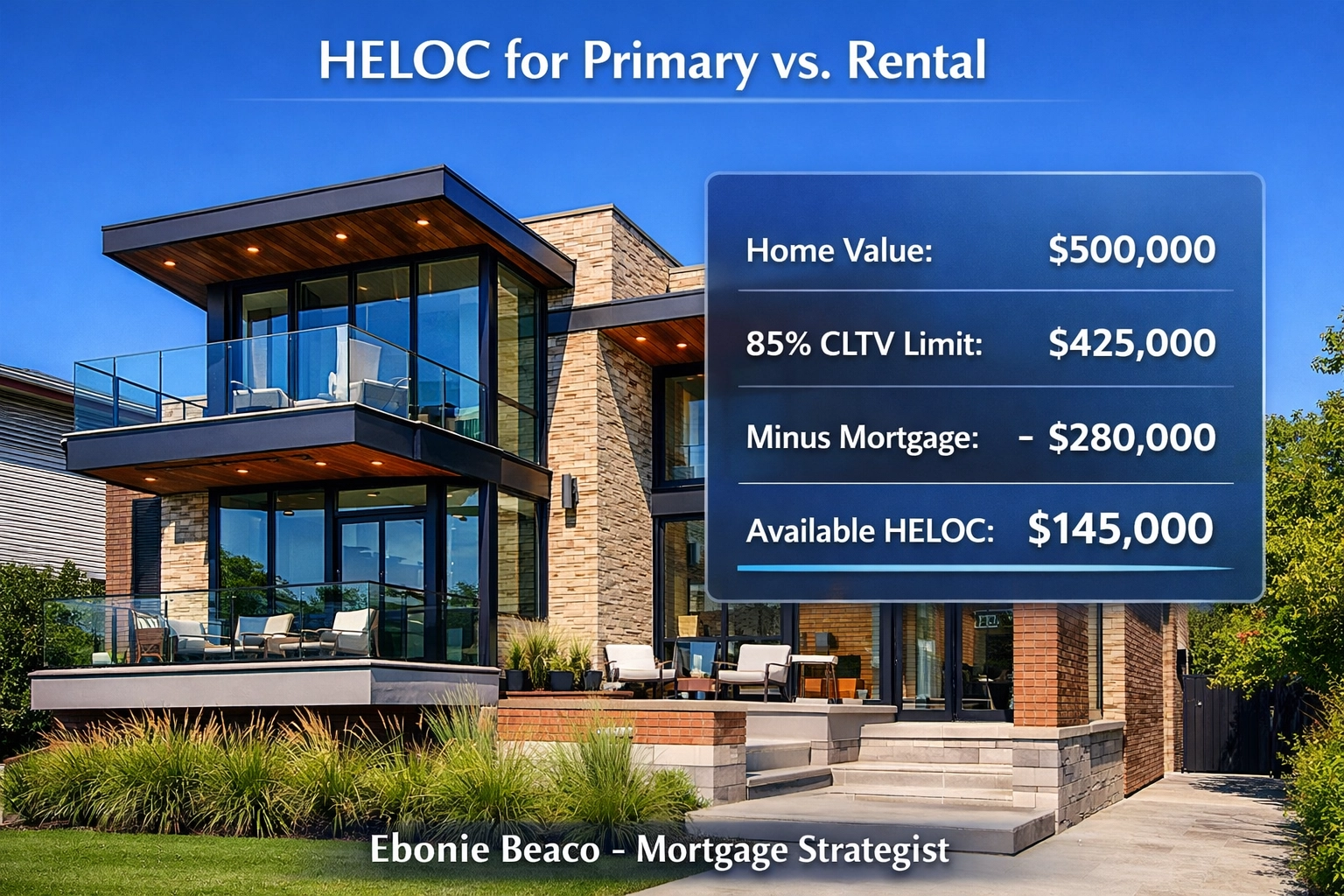

Imagine you own a home in Chicago, Illinois. Over the last few years, the property value has climbed to $500,000. Your current mortgage balance is $280,000. You want to use a HELOC to fund a down payment for your first rental property.

- Property Value: $500,000

- Max CLTV (85%): $425,000

- Current Mortgage: $280,000

- Available HELOC Credit: $145,000

With $145,000 in available credit, you could easily secure a 20% down payment for a $400,000 rental property in Indiana or Arkansas, while still having funds left over for minor renovations.

Visual Description: Financial breakdown graphic. Home Value $500k. 85% Limit = $425k. Subtract $280k Mortgage. Result = $145k Available HELOC. Image Title: HELOC for Primary vs. Rental. Bottom text: Ebonie Beaco - Mortgage Loan Officer.

Visual Description: Financial breakdown graphic. Home Value $500k. 85% Limit = $425k. Subtract $280k Mortgage. Result = $145k Available HELOC. Image Title: HELOC for Primary vs. Rental. Bottom text: Ebonie Beaco - Mortgage Loan Officer.

Scenario 2: The Rental Property Equity Play

Now, consider a seasoned investor with a duplex in Tampa, Florida. The property is worth $400,000 and has a mortgage balance of $200,000. The goal is to use the equity in this rental to buy another "fixer-upper."

- Property Value: $400,000

- Max CLTV (75%): $300,000

- Current Mortgage: $200,000

- Available HELOC Credit: $100,000

While the percentage is lower than the primary residence, that $100,000 provides the liquidity needed to act quickly when a deal surfaces in a competitive market like California or Georgia.

Strategic Deployment: HELOC vs. DSCR and Cash-Out Refinance

Understanding the tools is only half the battle; knowing when to use them is what builds long-term wealth.

Using HELOC for BRRRR (Buy, Rehab, Rent, Refinance, Repeat): Many investors use a HELOC to fund the "Buy" and "Rehab" phases. Once the property is renovated and a tenant is placed, they use a DSCR (Debt Service Coverage Ratio) loan to refinance the property, pay back the HELOC, and move on to the next deal.

HELOC vs. Cash-Out Refinance: If your current first mortgage has a very low interest rate (e.g., 3%), doing a cash-out refinance might not be the best move, as it would require you to refinance the entire balance at today’s higher rates. A HELOC allows you to keep your low-rate first mortgage in place and only pay the higher rate on the money you actually draw from the line of credit.

Short-Term Rental (Airbnb) Financing: For those looking at the vacation rental market in Florida or California, a HELOC can provide the "gap funding" needed to furnish a property or cover carrying costs during the initial setup phase. You can explore more about these specific options on our loan process page.

Preparing for Your Application

Whether you are applying for a line of credit on your home in Missouri or an investment property in Kentucky, preparation is vital.

- Check Your Credit: Ensure your score is at the peak of its potential. Clear up any small disputes or high credit card balances before the lender pulls your report.

- Organize Documentation: For primary residences, this is simple (paystubs, W2s). For rental HELOCs, be ready with lease agreements, property tax bills, and insurance declarations for your entire portfolio.

- Evaluate Cash Flow: Lenders will look at the FAQ regarding your ability to carry the debt. If the property is a rental, ensure the DSCR is strong.

- Appraisal Readiness: Since the loan is based on equity, the appraisal is a critical step. Ensure the property is in good repair to maximize the value.

Why the Location of the Property Influences Your Strategy

The housing market activity in your specific region influences how aggressive you can be. In high-appreciation states like California or Florida, equity can grow rapidly, allowing you to open a HELOC sooner than in slower-growth markets.

Conversely, in stable markets like Michigan or Arkansas, your strategy might focus more on the cash flow the property generates. Knowing the local nuances is why working with a dedicated strategist is vital to your success.

Explore our about us section to see how we help homeowners and investors navigate these regional differences.

Conclusion

Equity is only valuable if you have a plan for it. A HELOC can be the bridge between where your portfolio is today and where you want it to be next year. Whether you are looking to renovate your kitchen in Virginia or acquire your fifth rental property in Chicago, understanding the nuances between primary and rental lines of credit is the first step toward sophisticated real estate financing.

If you are unsure which path is right for your financial profile, comparing your options with a professional can provide the clarity you need.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664