HELOC vs. Cash-Out Refi: Scaling Your Florida Portfolio

If you have been watching the Florida real estate market lately, you know that property values in cities like Tampa, Orlando, and Miami have seen significant shifts. For a homeowner or a landlord, this increase in value is more than just a number on a screen. It represents usable equity.

When you reach the point where you want to grow your portfolio from one property to three, or five to ten, the big question usually centers on how to tap into that equity. Two of the most common tools for this are the Home Equity Line of Credit (HELOC) and the Cash-Out Refinance.

Choosing between them is not about finding a "better" loan. It is about finding the right tool for your specific phase of investment.

Defining Your Equity Tools

To understand which direction to take, we need to clear up exactly what these products do in a professional context.

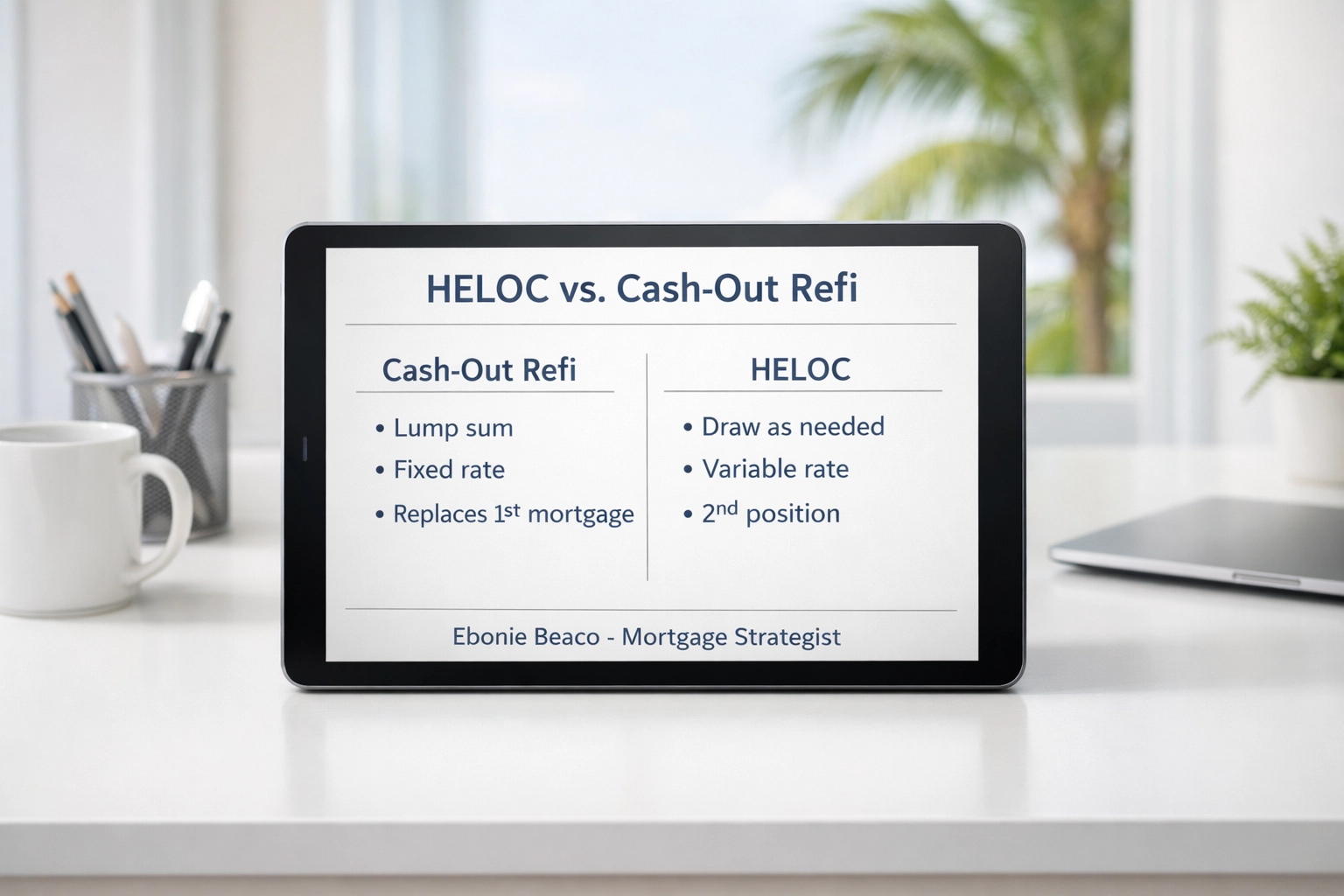

HELOC (Home Equity Line of Credit) A revolving line of credit secured by your home equity that allows you to borrow, repay, and borrow again. Practical Application: You use this like a credit card for your house to fund renovations or quick earnest money deposits on new deals.

Cash-Out Refinance A new mortgage that replaces your existing first mortgage with a larger loan, paying you the difference in a lump sum. Practical Application: You use this to lock in a long term fixed rate while pulling out a large amount of capital for a major purchase.

LTV (Loan to Value) The ratio of a loan to the value of an asset purchased. Practical Application: Most lenders in Florida will let you go up to 80 percent LTV for a cash out refinance on a primary residence.

Image Description: Title 'HELOC vs. Cash-Out Refi'. Comparison table showing: Cash-Out Refi (Lump sum, Fixed rate, Replaces 1st mortgage) vs. HELOC (Draw as needed, Variable rate, 2nd position). At the bottom: Ebonie Beaco - Mortgage Loan Officer.

Image Description: Title 'HELOC vs. Cash-Out Refi'. Comparison table showing: Cash-Out Refi (Lump sum, Fixed rate, Replaces 1st mortgage) vs. HELOC (Draw as needed, Variable rate, 2nd position). At the bottom: Ebonie Beaco - Mortgage Loan Officer.

The Cash-Out Refinance Strategy

A cash-out refinance is often the preferred choice for investors who want stability. When you perform a cash-out refinance, you are essentially starting over with a new 30 year fixed mortgage.

If your current interest rate is higher than today’s market rates, this move is a double win. You get your capital, and you potentially lower your total monthly commitment. Even if rates are slightly higher, the ability to fix your cost of capital for three decades provides a level of predictability that helps when calculating your DSCR (Debt Service Coverage Ratio) on future rentals.

In Florida, the closing costs for a refinance typically range between 2 percent and 5 percent of the loan amount. You should account for these costs when you are calculating your potential return on investment for the next property. You can explore more about this process at https://www.homeloansnetwork.com/home-refinance.

The HELOC Flexibility Strategy

A HELOC works differently. It usually sits in a "second position" behind your main mortgage. This means you do not have to touch your original 30 year mortgage. If you have a 3 percent interest rate on your primary home from years ago, you likely do not want to give that up.

A HELOC allows you to keep that low rate while opening a separate line of credit. You only pay interest on what you actually spend. If you have a $100,000 HELOC but you only use $20,000 for a kitchen remodel on a flip, you only pay interest on that $20,000.

The downside? HELOCs almost always have variable interest rates. In a volatile market, your payment could increase. This is why many Florida investors use HELOCs for short term needs, like the "Renovation" part of a BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy.

Calculating the Scaling Potential

Let's look at how the numbers actually work for a homeowner in a city like Jacksonville or St. Petersburg.

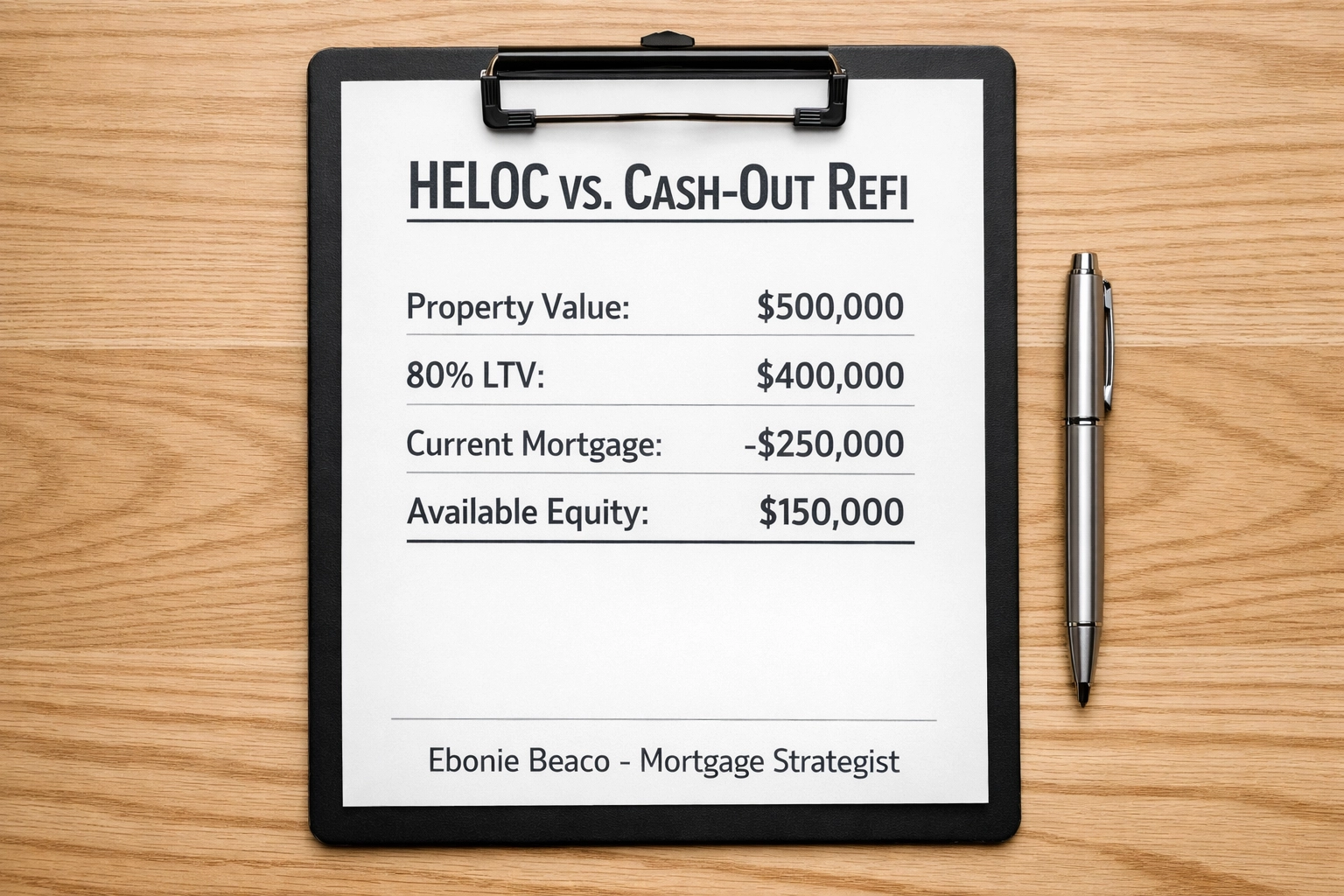

Imagine you own a property valued at $500,000. Your current mortgage balance is $250,000.

The Calculation:

- Property Value: $500,000

- Max Loan to Value (80%): $400,000

- Current Mortgage: -$250,000

- Potential Available Equity: $150,000

With $150,000 in your pocket from a cash-out refinance, you could potentially put 25 percent down on two separate $300,000 investment properties. This allows you to triple your door count using the equity from just one asset.

Image Description: Title 'HELOC vs. Cash-Out Refi'. Calculation Breakdown: Property Value $500,000, 80% LTV = $400,000. $400,000 minus $250,000 current loan = $150,000 Cash Available. At the bottom: Ebonie Beaco - Mortgage Loan Officer.

Image Description: Title 'HELOC vs. Cash-Out Refi'. Calculation Breakdown: Property Value $500,000, 80% LTV = $400,000. $400,000 minus $250,000 current loan = $150,000 Cash Available. At the bottom: Ebonie Beaco - Mortgage Loan Officer.

Scaling with DSCR Loans

Once you have extracted that equity, the next step is often looking at DSCR Investor Loans. These loans are a favorite for scaling because they do not rely on your personal income or tax returns. Instead, the lender looks at the rental income of the property you are buying.

If the rent covers the mortgage payment (including taxes, insurance, and HOA), the deal often qualifies. By using your cash-out funds as a down payment, you can keep your personal DTI (Debt to Income) ratio clean, making it easier to continue acquiring properties. You can find more details on these strategies at https://www.homeloansnetwork.com/mortgage-basics.

Florida Specific Considerations

Florida has some unique quirks when it comes to refinancing.

Property Tax Reassessments In Florida, we have the "Save Our Homes" cap, which limits how much the assessed value of your primary residence can increase each year. When you refinance, it usually does not trigger a massive reassessment like a sale would, but you should always check with your local county appraiser to understand the impact on your escrow account.

Insurance Costs Insurance is a hot topic in the Sunshine State. Before you pull equity to buy a new property, ensure you have a clear quote for the new asset. Higher insurance premiums can eat into the cash flow you projected when you were doing your initial math.

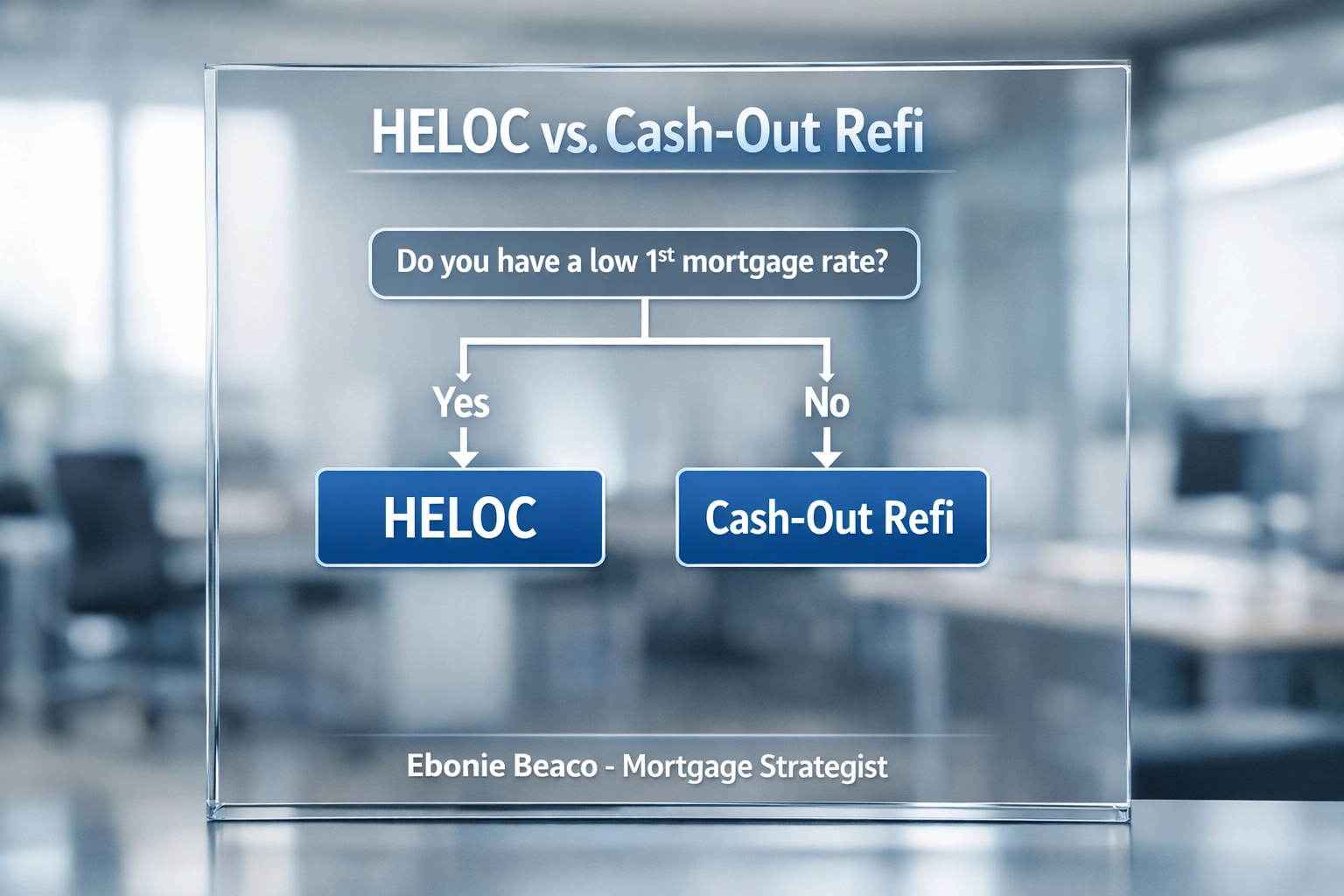

Which One Should You Choose?

The choice depends on your timeline and your existing mortgage.

Go with a Cash-Out Refinance if:

- You need a large, one time lump sum for a major acquisition.

- Your current interest rate is higher than or similar to market rates.

- You want a fixed, predictable payment for the next 30 years.

- You are planning to hold the new investment properties for a long period.

Go with a HELOC if:

- You have an incredibly low interest rate on your primary mortgage that you want to keep.

- You only need funds sporadically for things like repairs or earnest money.

- You plan to pay the balance back quickly (e.g., after finishing a flip).

- You want lower upfront closing costs.

Image Description: Title 'HELOC vs. Cash-Out Refi'. Flowchart: Start -> Do you have a low 1st mortgage rate? -> Yes -> HELOC. -> No -> Cash-Out Refi. At the bottom: Ebonie Beaco - Mortgage Loan Officer.

Image Description: Title 'HELOC vs. Cash-Out Refi'. Flowchart: Start -> Do you have a low 1st mortgage rate? -> Yes -> HELOC. -> No -> Cash-Out Refi. At the bottom: Ebonie Beaco - Mortgage Loan Officer.

How Mentoring Helps

Scaling a portfolio involves more than just picking a loan. It involves timing, market selection, and understanding how to structure your debt so that you do not get stuck after the second or third property.

Many investors run into a wall because they use the wrong type of financing early on. They might use a traditional conventional loan when a Non-QM Mortgage Loan or a Bridge Loan would have kept their options more open for the next deal.

As a mortgage strategist, I help you look at the chess board three moves ahead. Whether you are a first time landlord in Miami or a seasoned investor in Chicago looking to enter the Florida market, having a plan for your equity is vital.

You can use resources like the https://www.homeloansnetwork.com/mortgage-calculators to start running your own numbers, but a one on one conversation often uncovers opportunities you might have missed.

Moving Forward

The Florida market continues to offer opportunities for those who know how to leverage their positions. Equity is a tool, and like any tool, it works best when you understand exactly how to handle it.

If you are ready to explore your equity options or if you are looking for mentoring on how to build a sustainable real estate portfolio, let's connect. We can look at your current numbers, your goals for the next twelve months, and figure out which path makes the most sense for your financial profile.

Explore your options and take the next step in your investment journey.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664