HELOC Secrets Revealed: What Your Michigan HELOC Lender Doesn't Want You to Know

Accessing the equity in your home often feels like finding a hidden treasure chest. Whether you are living in Michigan, Virginia, or any of the other states we serve like Florida or California, your home is likely your largest financial asset. A Home Equity Line of Credit (HELOC) is frequently marketed as the ultimate flexible tool to tap into that wealth.

However, many institutions: including your typical Michigan HELOC lender: may not highlight the structural risks and nuances that could impact your long-term financial health. My goal as a mortgage strategist is to peel back the curtain and provide the transparency you deserve.

Essential HELOC Terminology

- HELOC (Home Equity Line of Credit): A revolving credit line secured by your primary or investment property that allows you to borrow against equity as needed.

- CLTV (Combined Loan-to-Value): The total percentage of all loans on a property compared to its current market value.

- Draw Period: The initial phase of the loan, usually 10 years, during which you can withdraw funds and often make interest-only payments.

- Repayment Period: The phase following the draw period where the credit line closes, and you must pay back both principal and interest.

The Interest-Only Illusion That Could Trap Your Budget

Jump in and look at the most common marketing hook: the low monthly payment. During the draw period, most lenders allow you to pay only the interest on the amount you have borrowed. While this keeps your immediate costs low, it creates a significant financial cliff.

The moment your draw period ends, the loan enters the repayment phase. Suddenly, you are required to pay back the full principal balance over a set term, often 10 or 20 years, alongside the interest. For many homeowners in Virginia or Illinois, this transition leads to "payment shock," where the monthly obligation doubles or even triples overnight.

Why the Draw Period Is Only Half the Story

Explore the math before you commit. If you use a HELOC to fund a major renovation or to start a fix-and-flip project, you must have a clear exit strategy for the principal balance. Relying solely on the interest-only payment schedule is a short-sighted move that many lenders won't discourage because they earn more interest over time.

The Variable Rate Trapdoor and How to Avoid It

Access to cheap capital is great until the price of that capital changes. Unlike a standard conventional loan with a fixed rate, almost every HELOC is a variable-rate product tied to the Prime Rate.

When the Federal Reserve adjusts interest rates, your HELOC payment moves in tandem. This means your "affordable" credit line could become a heavy burden if the economy shifts.

Understanding the Prime Rate Connection

Compare your options carefully. Some lenders offer a "fixed-rate segment" feature. This allows you to lock in a specific portion of your balance at a fixed interest rate. Your Michigan HELOC lender might not proactively offer this because variable rates are often more profitable for the bank. Always ask if you can convert segments of your balance to a fixed rate to protect your cash flow from market volatility.

Is Your Credit Line at Risk of Being Frozen?

One of the most significant secrets in the industry is the lender's power to freeze or reduce your credit line. Because a HELOC is a revolving line secured by your home, the lender monitors both your credit score and the local housing market activity.

If property values in your neighborhood dip or your credit profile changes, the lender can unilaterally decide to "freeze" your line. This means you could lose access to your funds exactly when you need them most: such as during an economic downturn or in the middle of an investment project.

Market Conditions and Your Equity Access

This risk is particularly relevant for investors in states like Alabama, Arkansas, and Missouri where market fluctuations can occur unexpectedly. A mortgage strategist will advise you to draw the funds you anticipate needing for a project in advance rather than assuming the line will always be available.

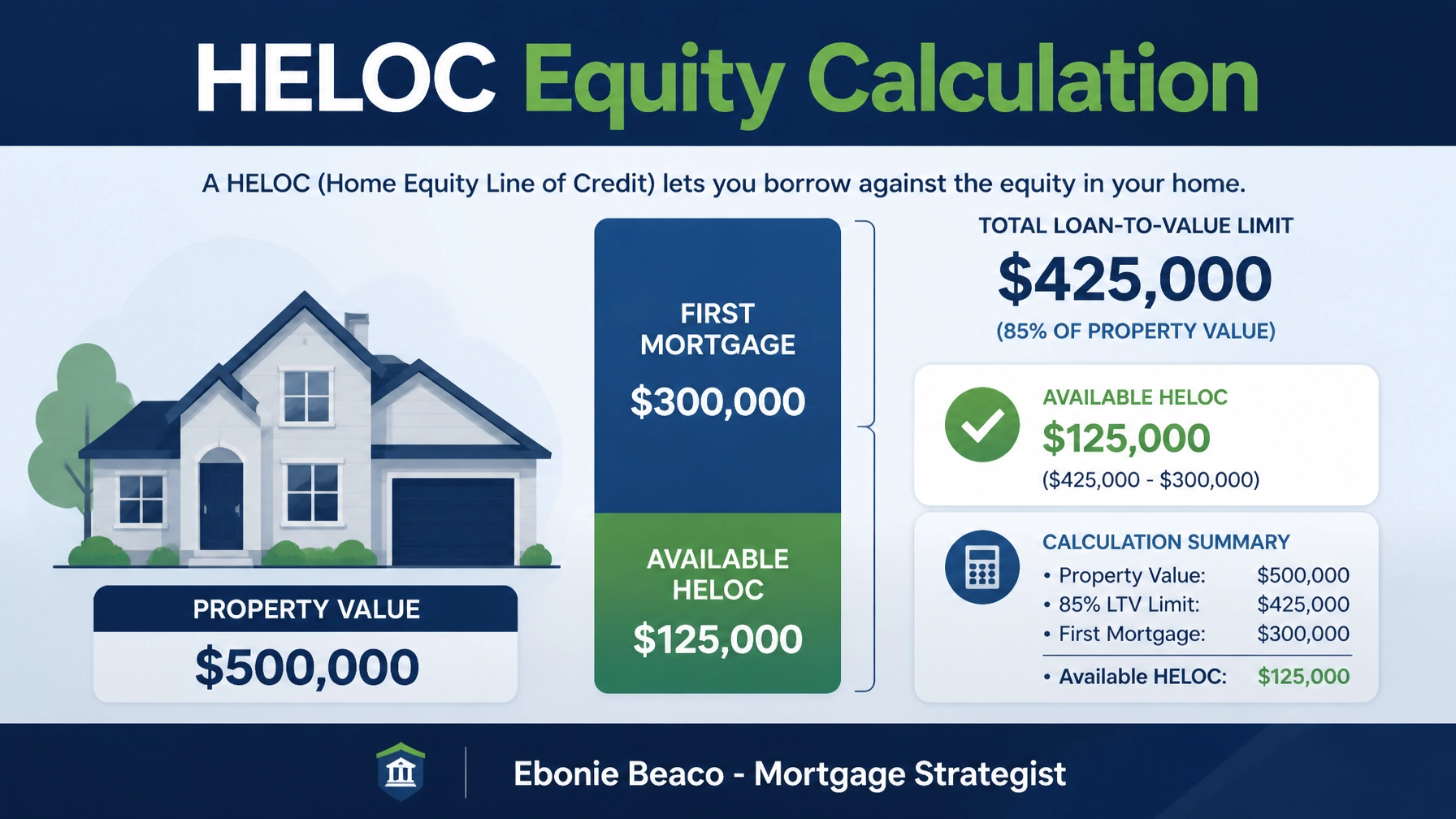

A Practical Example: Unlocking $125,000 in Michigan Equity

To understand how these numbers function in a real scenario, let's look at a typical homeowner in Michigan or a Virginia HELOC lender's client.

Suppose you own a home valued at $500,000. You currently have a first mortgage balance of $300,000. Most lenders will allow a Maximum Combined Loan-to-Value (CLTV) of 85%.

The Calculation:

- Total Allowable Debt (85% of $500k): $425,000

- Minus Current Mortgage: $300,000

- Available HELOC Equity: $125,000

With $125,000 available, you have the capital to fund an Airbnb startup, consolidate high-interest debt, or even provide a down payment on a multi-unit apartment building.

Using Your HELOC for Real Estate Investing

Investors frequently use HELOCs as a "bridge" to acquire new properties. Whether you are a wholesaler in Georgia or a landlord in Kentucky, a HELOC provides the liquidity required to move quickly on a deal.

Fix and Flip or Buy and Hold?

Explore how a HELOC can function as "dry powder" for your portfolio. You can use the line to pay for renovations on a fix-and-flip property, then pay the line back once the property sells. For BRRRR investors (Buy, Rehab, Rent, Refinance, Repeat), a HELOC is a powerful tool to fund the initial acquisition and rehab before moving into long-term DSCR rental property loans.

Michigan vs. Virginia: Choosing Your Local Strategy

While the fundamental mechanics of a HELOC remain the same, local lender behavior varies by state. In Michigan, you may find credit unions that are more aggressive with their CLTV limits, sometimes reaching 90% for top-tier borrowers.

In contrast, a Virginia HELOC lender might place more emphasis on debt-to-income (DTI) ratios and may have different fee structures for annual maintenance. It is vital to compare regional players against national banks to find the most favorable terms for your specific profile.

Local Lending Nuances You Should Know

- Michigan: High availability of credit union options with low or no closing costs.

- Virginia: Competitive market with many regional banks offering fixed-rate conversion options.

- Other States: We also navigate the unique lending landscapes in Indiana, Kentucky, Missouri, and beyond to ensure your strategy aligns with local market trends.

Comparing HELOCs with Other Financing Options

A HELOC is not always the best solution. Depending on your goals, a cash-out refinance or a second mortgage might provide more stability. If you need a large lump sum and prefer a fixed interest rate from day one, a cash-out refinance allows you to replace your existing mortgage with a new, larger one, pocketing the difference.

However, if you already have a very low interest rate on your first mortgage, you likely do not want to touch it. In that case, a HELOC or a standalone second mortgage is the smarter path to preserve your primary low-rate financing while still accessing your equity.

Final Strategies for Savvy Homeowners

Before you sign on the dotted line with any Michigan HELOC lender, ask the hard questions. Ensure you understand the transition from the draw period to the repayment period. Confirm the frequency of rate adjustments and check for any hidden fees, such as "inactivity fees" if you choose not to use the line immediately.

Position yourself as an informed borrower. By understanding these industry secrets, you can use home equity as a tool for wealth creation rather than a source of financial stress.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664