HELOC Secrets Revealed: What Experts Don't Want You to Know About Financing a Home Remodel

You have probably seen the commercials. A smiling couple stands in a sparkling new kitchen, talking about how easy it was to fund their "dream home" using the equity they already had.

While it sounds like magic, pulling cash out of your house is a serious financial move. If you are a homeowner in Indiana, Kentucky, or any of the states we serve like Florida and Virginia, you are sitting on a potential goldmine of equity.

But there is a darker side to the Home Equity Line of Credit (HELOC) that many lenders skip over during the sales pitch. At Home Loans Network, we believe in being transparent. We want you to understand the risks as well as the rewards before you sign on the dotted line.

What is a HELOC?

HELOC (Home Equity Line of Credit): A revolving credit line secured by your home that allows you to borrow against the equity you have built up.

Think of it like a credit card for your house. You get approved for a specific limit, and you can pull money out as you need it for things like a new roof, a kitchen remodel, or even to fund a fix and flip investment. You only pay interest on the amount you actually use.

The Secret Risks: What to Watch For

Most people focus on the low initial interest rates and the flexibility. However, there are several "secrets" or risks that can turn a home remodel into a financial headache if you are not careful.

1. The Foreclosure Threat

This is the most important thing to remember: your home is the collateral. Unlike a personal loan or a credit card, if you cannot make the payments on your HELOC, the lender has the right to take your house.

2. The Variable Rate Rollercoaster

Most HELOCs come with variable interest rates. This means your monthly payment is tied to market indexes. If the Federal Reserve raises rates, your monthly payment goes up.

Imagine starting a renovation with a 6% interest rate only to see it climb to 10% or 12% before the project is finished. This makes long-term budgeting for your remodel extremely challenging.

3. The "Draw Period" vs. "Repayment Period" Trap

HELOCs usually have two phases. During the Draw Period (often 10 years), you might only be required to pay the interest. This feels great because the payments are low.

However, once the Repayment Period starts, you have to pay back both the interest and the principal. Your monthly payment could double or triple overnight. If you are not prepared for that jump, it can cause a massive strain on your budget.

4. The Freeze Factor

Did you know a lender can freeze or reduce your credit line? If your credit score takes a dive, or if home values in your neighborhood start to drop, the bank can stop you from taking any more money out.

If you are halfway through a $50,000 kitchen remodel and the bank freezes your line at $25,000, you could be left with a construction zone and no way to pay the contractor.

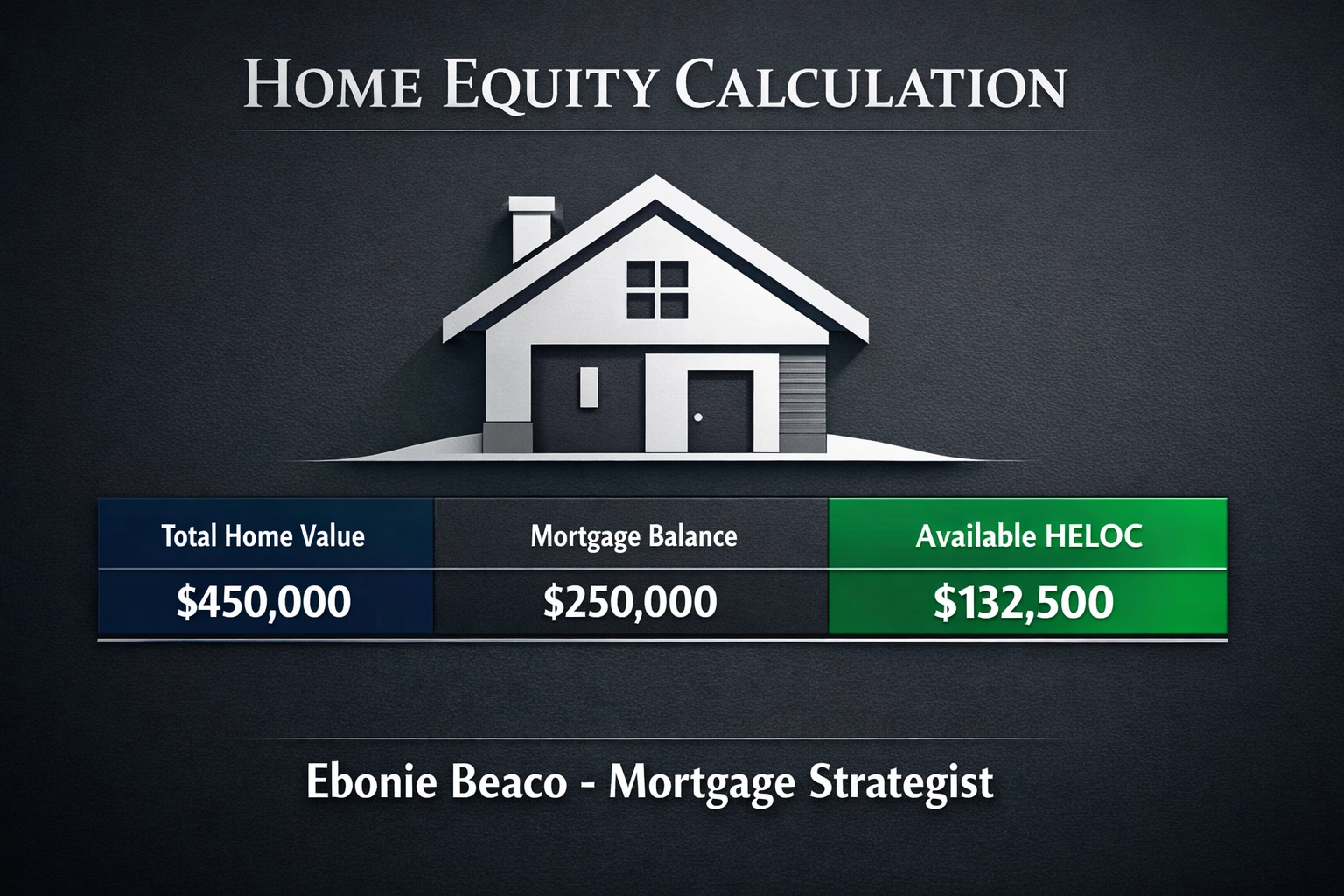

Real World Math: How Much Can You Actually Get?

Let's look at a common scenario for a homeowner looking for an Indiana HELOC lender or a Kentucky HELOC lender.

Suppose you own a home in Indianapolis or Louisville valued at $450,000. You currently owe $250,000 on your primary mortgage.

Most lenders will allow you to borrow up to 80% or 85% of your home's total value (Combined Loan-to-Value, or CLTV).

- Home Value: $450,000

- 85% Max Limit: $382,500

- Current Mortgage: $250,000

- Available HELOC: $132,500

In this case, you have access to $132,500 to fund your renovations. This is a powerful tool for home purchase strategies or simply upgrading your current living space to increase its resale value.

Why Homeowners Love HELOCs for Remodeling

Despite the risks, the HELOC remains a top choice for financing a home remodel for several reasons:

- Interest is often tax-deductible: If you use the funds to substantially improve the home that secures the loan, you might be able to deduct the interest. Always consult a tax professional to verify this for your specific situation.

- Flexibility: You don't have to take all the money at once. If your contractor needs $10,000 for demolition today and $15,000 for cabinets in three months, you only draw what you need.

- Lower Rates than Credit Cards: Even with variable rates, HELOCs are almost always significantly cheaper than using a high-interest credit card to fund a renovation.

Is a HELOC Better Than a Cash-Out Refinance?

Many of our clients in Alabama, Michigan, and Georgia ask if they should get a HELOC or a cash-out refinance.

Cash-Out Refinance: Replacing your existing mortgage with a new, larger loan and taking the difference in cash.

If you currently have a very low interest rate on your primary mortgage (like the 3% rates we saw a few years ago), you probably do not want to touch it. A cash-out refinance would force you to trade that 3% rate for whatever the current market rate is.

In that case, keeping your low-rate first mortgage and adding a HELOC on top is usually the smarter move. It allows you to access equity without losing your primary loan's benefits.

However, if interest rates have dropped since you bought your home, a cash-out refinance might allow you to get the cash you need and lower your overall monthly payment at the same time. You can use our mortgage calculators to compare these scenarios.

Using HELOCs as an Investor Strategy

Real estate investors in markets like Chicago or cities throughout Florida often use HELOCs as "bridge" money.

If you own your primary residence and have significant equity, you can use a HELOC to:

- Fund a Down Payment: Use your equity to put a down payment on a DSCR rental property.

- Cover Renovation Costs: Use the line of credit to fix up a rental unit before putting it on the market.

- Bridge Financing: Use the HELOC to buy a property quickly with "cash" and then refinance into a long-term loan later.

This is a common tactic for BRRRR investors (Buy, Rehab, Rent, Refinance, Repeat) who need quick access to capital to move on a deal.

How to Stay Safe When Borrowing Against Your Home

If you decide to move forward with a HELOC for your remodel, follow these steps to protect your financial health:

1. Treat it like a loan, not a piggy bank.

Only borrow what you absolutely need for the project. Resist the urge to use the leftover "extra" credit for a vacation or a new car.

2. Budget for the "Worst Case" Rate.

When looking at your monthly budget, don't just look at the current interest rate. Ask your lender what the "cap" is. Most HELOCs have a maximum rate they can hit. If you can't afford the payment at the maximum rate, you might want to consider a fixed-rate loan instead.

3. Have a Repayment Plan.

Don't wait for the 10-year draw period to end before you start thinking about the principal. Try to make payments toward the principal from day one. This reduces the total interest you pay and ensures you aren't hit with a massive payment shock later.

4. Check Your Equity Levels.

If home prices drop in your area (whether you are in Missouri, Arkansas, or California), you could end up "underwater": meaning you owe more than the house is worth. Keep a close eye on local market trends.

Exploring Your Options

Every homeowner's situation is different. What works for a family in Virginia might not be the best move for an investor in Illinois.

At Home Loans Network, we pride ourselves on being more than just a lender. We are your mortgage strategists. We help you look at the big picture: your current mortgage, your credit profile, and your long-term goals: to find the right fit.

Explore our various loan programs to see how we can help you unlock the value in your home. Whether you are looking for a jumbo loan, a DSCR loan, or a simple HELOC, we have the expertise to guide you through the process.

Compare the costs of a HELOC versus other financing options. Access the funds you need to turn your current house into your forever home.

Ready to Start Your Project?

Financing a remodel doesn't have to be a mystery. By understanding the secrets of the HELOC, you can use your home equity as a tool to build wealth and improve your quality of life without falling into common debt traps.

If you have questions about how a HELOC would work for your specific property in Florida, Indiana, or any of the other states we serve, we are here to help.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664