Ground-Up Development Loans: Building Your Portfolio

Taking a vacant lot and turning it into a high-value residential or commercial property is one of the most rewarding moves in real estate. Whether you are looking at a single-family home in Virginia or a multi-unit complex in the heart of Chicago, ground-up development allows you to create inventory where none exists.

However, financing these projects is a different beast compared to a standard home purchase. You aren't just buying a building; you are funding a vision, a timeline, and a massive logistics operation. Ground-up development loans provide the capital to take you from raw land to a finished certificate of occupancy.

What is a Ground-Up Development Loan?

A ground-up construction loan is a short-term financing tool designed to fund the creation of new properties starting from scratch. Unlike a traditional mortgage where you get a lump sum at the closing table, these loans operate on a disbursement basis.

Ground-Up Construction Loan: A specialized short-term loan used to cover land acquisition, labor, materials, and permits for a new building project. Practical application: This allows you to preserve your liquid capital while the lender pays out the costs of building as work is completed.

These loans are typically interest-only during the construction phase. You only pay interest on the money that has actually been "drawn" or spent, which helps keep your carrying costs lower while there is no rental income coming in yet.

How the Draw Schedule Works

You don't get the full loan amount on day one. Instead, your lender follows a draw schedule. This is a pre-negotiated timeline where funds are released in stages as you hit specific construction milestones.

Typical milestones include:

- Site Preparation: Clearing the land and grading.

- Foundation: Pouring the slab or basement.

- Framing: Getting the skeleton of the building up.

- Mechanicals: Installing HVAC, plumbing, and electrical systems.

- Finish Work: Drywall, flooring, and cabinetry.

Before each draw is released, an inspector usually visits the site to verify that the work is done. This transparency ensures that the project is moving according to the loan process and that the budget is being managed correctly.

Qualifying for New Construction Financing

Lenders look at more than just your credit score when you apply for a ground-up loan. They are essentially betting on your ability to finish the project. Here is what you usually need to bring to the table:

1. Down Payment (Equity) Most lenders require a down payment of 20% to 30% of the total construction cost. If you already own the land, the equity in that land can often count toward your down payment.

2. Detailed Construction Budget You need a "line-item" budget. Lenders want to see exactly how much you are spending on everything from the architectural plans to the final coat of paint. You can use mortgage calculators to help estimate some of your long-term costs, but the construction budget itself must be professional and precise.

3. Proven Builder Experience If this is your first build, you might need to partner with a licensed general contractor who has a track record. Lenders often look for a history of at least three completed new builds within the last few years to feel confident in the project’s success.

4. Low Debt-to-Income (DTI) Ratio While some investor-specific loans like DSCR rental property loans focus primarily on the property's income, ground-up loans still place weight on your overall financial health. A DTI under 43% is generally the gold standard.

Scaling Your Portfolio with Ground-Up Builds

Why do experienced investors choose ground-up development over simply buying existing homes? The answer is customization and equity.

When you build from scratch in high-demand markets like Florida or California, you aren't limited by the "bones" of an old house. You can build exactly what modern tenants or buyers want: open floor plans, energy-efficient systems, and smart home technology.

By the time the project is finished, the After Repair Value (ARV) or completed value of the property is often significantly higher than the total cost of the land and construction. This creates instant equity that you can then access through a cash-out refinance to fund your next project.

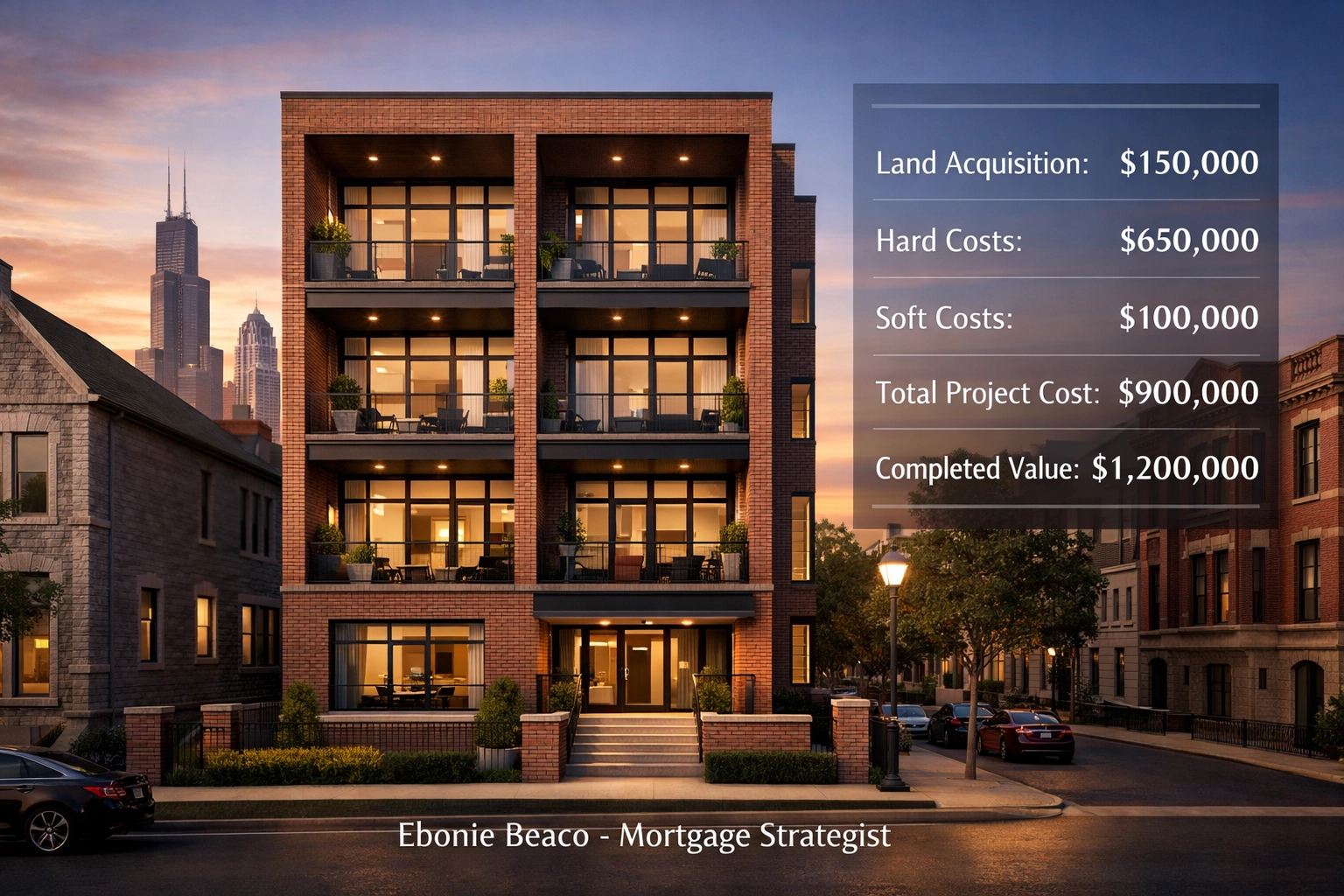

Financial Example: Building a Four-Unit in Chicago

Let’s look at how the numbers might play out for a small multi-family development in a market like Chicago.

- Land Acquisition Cost: $150,000

- Hard Construction Costs (Labor/Materials): $650,000

- Soft Costs (Permits/Architect/Interest): $100,000

- Total Project Cost: $900,000

- Loan-to-Cost (LTC) at 75%: $675,000

- Investor Down Payment: $225,000

If the completed 4-unit building is appraised at $1,200,000 once finished, the investor has created $300,000 in equity. At this point, many developers choose to transition from their short-term construction loan into a long-term DSCR loan to hold the property as a rental, or sell it for a significant profit.

If you're unsure how these numbers fit your specific goals, you can explore our FAQ for more on loan structures.

Regional Opportunities for Developers

The strategy for ground-up development changes depending on where you are building.

- Florida: The demand for new construction remains high due to population growth. Investors often focus on single-family builds or Airbnb-ready properties.

- California: Space is at a premium. Ground-up development often involves Accessory Dwelling Units (ADUs) or high-end luxury builds.

- Georgia and Virginia: These states offer a mix of suburban expansion and urban infill projects where ground-up loans are used to revitalize older neighborhoods.

Regardless of the location, the key is having a mortgage strategist who understands these specific markets. You can learn more about us and how we support investors across these regions.

Ground-Up vs. Fix and Flip

Is it better to renovate or build new? Fix and Flip Loans are great for properties that need cosmetic or structural updates but already have a shell. They are generally faster and have fewer permit hurdles.

Ground-Up Loans are for the "blank slate" projects. While they take longer (usually 12 to 24 months), they offer the highest level of control. You don't have to worry about "surprises" hidden behind the walls of a 100-year-old house because you are the one putting the walls up.

If you are a seasoned investor or an aspiring developer ready to take the next step, the right financing makes all the difference. We provide the tools for everything from home purchase to complex commercial builds.

Ready to Build?

Ground-up development is a powerful way to scale. It requires a solid plan, a great team, and a lender who understands the nuances of draw schedules and construction milestones. If you are looking for guidance on how to structure your next build or want to compare different mortgage basics, the Home Loans Network team is here to help.

Don’t let the complexity of new construction hold you back from building your portfolio. Whether you need financing for a duplex or a larger multi-family project, we can guide you through the process from the first shovel in the ground to the final refinance.

Reach out to Ebonie Beaco for ground-up development loans or mentoring at www.homeloansnetwork.com.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664