Ground-Up Development: How to Finance New Construction from Scratch

Starting a project from a literal patch of dirt is the ultimate play for many real estate investors. Whether you are looking at urban infill in Chicago, a multifamily complex in Florida, or a suburban subdivision in Virginia, ground-up development allows you to create inventory exactly how the market wants it. However, the complexity of financing these projects is significantly higher than buying a turnkey rental or even a standard fix-and-flip.

When you move into the world of new construction, you aren't just a landlord or a renovator; you are a creator. This means your lenders will look at you through a different lens. They want to see your track record, your team of professionals, and a rock-solid capital stack. In this guide, we will break down how the money flows from the first permit to the final certificate of occupancy.

The Reality of Starting from Zero

Ground-up development involves taking raw or underutilized land and building a structure from scratch. This process carries more risk than existing property acquisitions because there are so many variables: zoning changes, supply chain disruptions, labor shortages, and environmental issues. Because of this risk, the financing is structured in layers.

For seasoned investors in markets like California or Georgia, understanding the local loan process is the first step toward a successful build. You need to know how much skin you have in the game and where the gaps in your funding might appear.

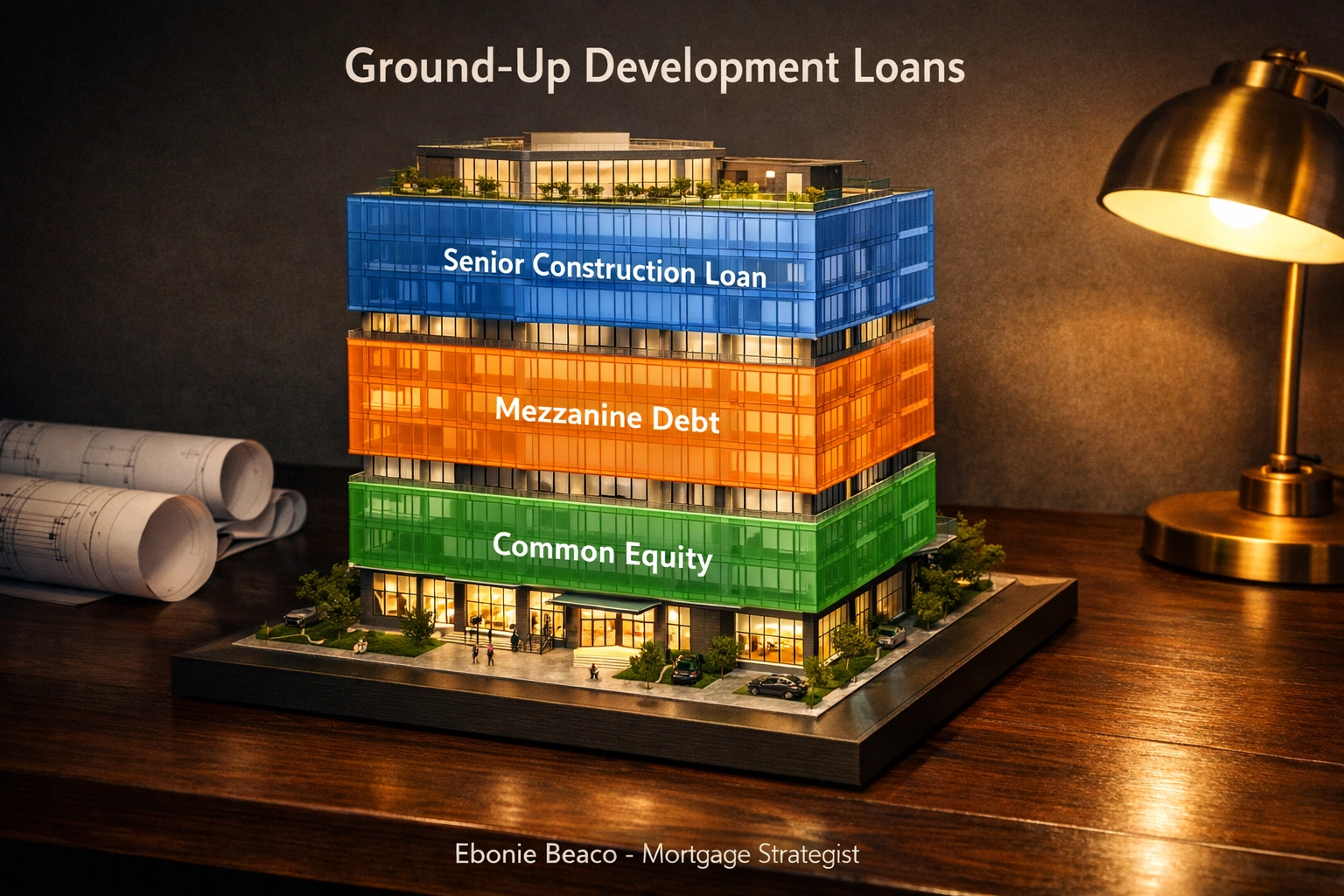

Understanding the Capital Stack

In the development world, we talk about the capital stack. This is simply the different types of money that make up the total budget of your project. Think of it like a layered cake.

Senior Construction Debt

This is the foundation of your financing. Typically provided by banks or specialized private lenders, senior construction loans usually cover 55% to 65% of the total project cost. Because this is "senior" debt, this lender has the first claim on the property if things go sideways.

Unlike a traditional mortgage where you get all the cash at the closing table, construction loans use a draw process. You only pay interest on the money you have actually spent. This keeps your holding costs lower during the early phases of the build.

Mezzanine Debt and Preferred Equity

If your senior loan covers 60% and you don't want to bring the remaining 40% in cash, you look for mezzanine debt or preferred equity. This fills the gap between the senior debt and your own cash. It is more expensive: often ranging from 12% to 18%: but it allows you to scale larger projects without draining your liquidity.

Common Equity

This is the "first loss" position. It is the money provided by you, the sponsor, and your outside investors. If the project costs more than expected, the equity holders are the ones who feel the pinch first. Institutional partners often expect a high internal rate of return (IRR) for taking on this level of risk.

Image Description: A professional diagram showing the levels of a Capital Stack for a development project. The bottom layer is Common Equity, the middle is Mezzanine Debt, and the top is Senior Construction Loan. Title: Ground-Up Development Loans. Bottom Text: Ebonie Beaco - Mortgage Loan Officer. No cash or money symbols shown.

Image Description: A professional diagram showing the levels of a Capital Stack for a development project. The bottom layer is Common Equity, the middle is Mezzanine Debt, and the top is Senior Construction Loan. Title: Ground-Up Development Loans. Bottom Text: Ebonie Beaco - Mortgage Loan Officer. No cash or money symbols shown.

Calculating Your Loan-to-Cost (LTC)

One of the most important metrics in new construction is Loan-to-Cost (LTC). While standard residential loans focus on Loan-to-Value (LTV), construction lenders care more about what it actually costs to build the thing.

LTC measures the loan amount against the total cost of the project, including the land purchase, hard costs (lumber, labor, concrete), and soft costs (architects, permits, engineering).

LTC Calculation Example

Let’s look at a hypothetical project in Michigan:

- Land Acquisition: $300,000

- Construction Hard Costs: $1,000,000

- Soft Costs (Permits/Plans): $200,000

- Total Project Cost: $1,500,000

If a lender offers you a 70% LTC loan, the calculation works like this: $1,500,000 (Total Cost) x 0.70 = $1,050,000 (Loan Amount)

In this scenario, you would need to provide $450,000 in equity to cover the remainder of the costs. You can use our mortgage calculators to help run different scenarios for your specific deal.

Image Description: A clean financial breakdown chart showing the LTC calculation. Total Project Cost: $1,500,000. Loan Amount: $1,050,000. LTC: 70%. Equity Required: $450,000. Title: Ground-Up Development Loans. Bottom Text: Ebonie Beaco - Mortgage Loan Officer. No cash or money symbols shown.

Image Description: A clean financial breakdown chart showing the LTC calculation. Total Project Cost: $1,500,000. Loan Amount: $1,050,000. LTC: 70%. Equity Required: $450,000. Title: Ground-Up Development Loans. Bottom Text: Ebonie Beaco - Mortgage Loan Officer. No cash or money symbols shown.

The Three Phases of Development Financing

Financing a ground-up project isn't a "one and done" event. It moves through distinct phases, each with its own requirements.

Phase 1: Pre-Development and Seed Equity

Before a bank will even talk to you about a construction loan, you need to have your "entitlements" in place. This means the land is zoned correctly, the city has approved your site plans, and you have your permits ready to go.

This phase is usually funded by seed equity: your own cash or high-net-worth partners. It is the riskiest phase because if the city denies your permit, the project is dead. Lenders want to see that you have navigated these hurdles before they commit the big capital.

Phase 2: The Construction Phase and the Draw Schedule

Once you close on your construction loan, the work begins. Funds are released in "draws." Every month, your contractor submits a request for payment based on the work completed. A third-party inspector will visit the site in Florida, Illinois, or wherever your project is located to verify that the foundation is actually poured or the roof is actually on.

Lenders also require lien waivers from subcontractors. This ensures that the people doing the work are getting paid and can't put a legal claim on your property. This transparent process protects both you and the bank.

Phase 3: Stabilization and Permanent Financing

A construction loan is temporary. It usually lasts 12 to 24 months. Once the building is finished and you have a Certificate of Occupancy, you have reached the "stabilization" phase.

If it’s a rental property, you might move into a DSCR investor loan to pay off the construction debt and hold the property long-term. If it’s a commercial project or a large multifamily building, you might look for a bridge loan or permanent agency financing.

The SBA 504 Alternative for Commercial Projects

For business owners in states like Arkansas or Kentucky who want to build their own facility (owner-occupied), the SBA 504 program is a game-changer. It offers a 50-40-10 structure that allows for up to 90% financing.

- 50% comes from a conventional bank loan.

- 40% comes from a Community Development Company (CDC) via an SBA-guaranteed debenture.

- 10% is your equity injection.

This is a powerful way to preserve your cash while building a custom space for your business operations. However, the SBA portion typically funds only after the construction is finished, so you still need an interim construction lender to get the building out of the ground.

Image Description: A professional infographic showing the 50-40-10 SBA loan structure. 50% Bank, 40% CDC/SBA, 10% Borrower Equity. Title: Ground-Up Development Loans. Bottom Text: Ebonie Beaco - Mortgage Loan Officer. No cash or money symbols shown.

Image Description: A professional infographic showing the 50-40-10 SBA loan structure. 50% Bank, 40% CDC/SBA, 10% Borrower Equity. Title: Ground-Up Development Loans. Bottom Text: Ebonie Beaco - Mortgage Loan Officer. No cash or money symbols shown.

Regional Markets and Infill Opportunities

The strategy for ground-up development changes depending on where you are building. In high-density areas like Chicago, many investors focus on "infill" development: building on vacant lots in established neighborhoods. In growing states like Georgia and Alabama, we see more large-scale residential subdivisions.

Each municipality has different rules. Financing for a project in California will require much more "soft cost" allocation for environmental studies and impact fees than a similar build in Missouri. When you about us and how we work, you'll see that we prioritize understanding these regional nuances.

Managing the Interest Reserve

One technical detail that catches many new developers off guard is the interest reserve. Since a building under construction doesn't generate rent, how do you make the monthly interest payments?

Most lenders build an "interest reserve" into the loan itself. The bank essentially lends you the money to pay them the interest every month. While this helps your cash flow, it means your loan balance grows every month. You must be diligent about your timeline to ensure you don't run out of interest reserve funds before the project is stabilized.

Moving Forward with Your Project

Ground-up development is a high-stakes, high-reward strategy. It requires a team that includes a skilled architect, a reliable general contractor, and a mortgage strategist who understands the nuances of construction draws and capital stacks.

If you are looking to move beyond simple renovations and start creating new inventory, you need a partner who can help you navigate the complexities of the home purchase of land and the subsequent construction financing.

Building from scratch is one of the best ways to build generational wealth and transform communities. By structuring your financing correctly from day one, you set your project up for a smooth transition from a construction site to a stabilized, income-producing asset.

Developing land? Contact Ebonie Beaco for ground-up development loans.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664