Friday’s Mortgage Market Update Explained in Under 3 Minutes

Today is Friday, June 5, 2026, and the mortgage industry is reacting to the latest economic data released this morning by the Bureau of Labor Statistics. The May Employment Situation report arrived at 8:30 AM ET, providing a critical look at the health of the labor market and its influence on long-term interest rates. For homeowners in states like Illinois and Florida, as well as real estate investors tracking portfolio performance, this data sets the tone for the upcoming summer housing market. Understanding these shifts allows you to position your financing strategy effectively whether you are looking to purchase a new property or leverage existing equity.

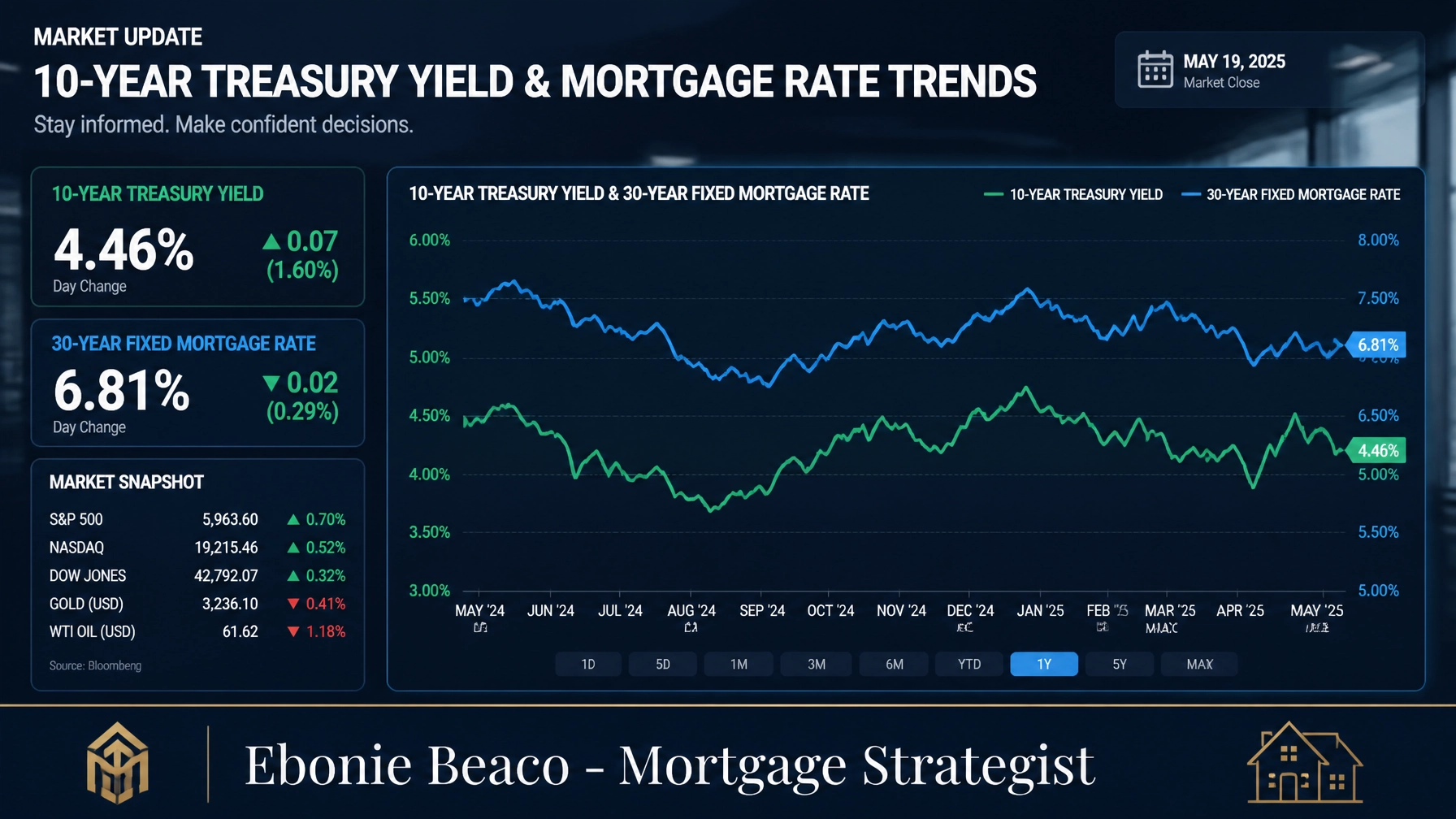

The relationship between employment data and mortgage rates is often direct because a strong labor market can signal persistent inflation. When job growth exceeds expectations, bond market participants often anticipate that the Federal Reserve will maintain higher interest rates to cool the economy. Conversely, a cooling labor market often leads to a decline in the 10-year Treasury yield, which serves as a primary benchmark for 30-year fixed-rate mortgages. You can track current rate trends and analyze how they impact your monthly payments by using the tools available at the Home Loans Network mortgage calculators.

The 10-Year Treasury Yield and Your Rate

10-Year Treasury Yield: This is the interest rate paid by the U.S. government on its ten-year debt obligations and acts as the lead indicator for long-term mortgage pricing. When this yield rises, lenders typically increase the interest rates offered to consumers on products like conventional and FHA loans. Today’s market response to the jobs report has caused immediate movement in this yield, which dictates the pricing you will see for the remainder of the weekend. Lenders across Alabama, Michigan, and Virginia are adjusting their rate sheets in real time to reflect this volatility.

Basis Points: This is a unit of measure used in finance to describe the percentage change in the value of financial instruments, where one basis point equals 0.01 percent. Even a move of ten or fifteen basis points in a single morning can significantly alter the cost of a loan over its thirty-year lifespan. Investors and homebuyers should stay informed about these daily shifts to ensure they lock in rates at the most opportune moments. Accessing professional guidance can help you navigate these fluctuations and understand how they apply to conventional loans and other programs.

The current volatility emphasizes why many borrowers are moving toward more specialized financing options that provide stability or flexibility. In markets like Chicago, where real estate activity remains robust, timing a rate lock is a strategic decision that requires up-to-the-minute information. You should compare different loan products to see which one aligns best with your current financial profile and long-term goals. Understanding the underlying economic drivers, such as the Consumer Price Index (CPI), provides you with the context needed to make these high-stakes decisions with confidence.

Housing Inventory and Regional Trends

Months of Supply: This metric represents how long it would take for all current homes on the market to sell at the current sales pace if no new listings were added. A balanced market typically has four to six months of supply, while anything less suggests a seller’s market where prices may continue to rise. In many parts of Georgia and Missouri, we are seeing a gradual increase in inventory as more sellers enter the market. This shift provides more options for first-time buyers who have been sidelined by the low inventory levels of previous years.

Median List Price: This is the middle price point of all homes currently listed for sale in a specific geographic area, providing a more stable read on market value than the average price. Prices in states like California and Virginia continue to show resilience due to sustained demand from professional buyers and growing families. Monitoring these localized price trends is essential for anyone considering a purchase or a cash-out refinance to fund new ventures. You can find detailed local data in resources like the Chicago neighborhoods market reports.

Active listings across the Midwest and Southeast are showing a varied landscape as we head into the second weekend of June. While some metropolitan areas are seeing a surge in new construction, other regions remain constrained by limited turnover in existing homes. This environment requires a customized approach to financing that accounts for the specific competitive dynamics of your local neighborhood. Realtors and investors should look closely at these regional variations to identify undervalued opportunities before they become mainstream knowledge.

Strategies for Current Homeowners

Cash-Out Refinance: This involves replacing your current mortgage with a new loan for more than you owe and taking the difference in cash to use for other purposes. Homeowners with significant equity can use these funds for home improvements, debt consolidation, or as a down payment on an investment property. This strategy is particularly effective for those who have seen their home values appreciate significantly in the last few years. You can explore how this process works and the requirements for approval at our loan process page.

HELOC (Home Equity Line of Credit): This is a revolving line of credit that allows you to borrow against the equity in your home as needed, similar to how a credit card works. It offers a flexible way to access capital without replacing your existing low-interest first mortgage, making it an attractive option in a rising rate environment. For residents in Arkansas and Kentucky, a HELOC can provide the necessary liquidity for emergency repairs or strategic investments. Many people find that this tool offers the right balance of access and control for managing their household wealth.

Consider a scenario where a homeowner in Florida has a property valued at $600,000 with a remaining mortgage balance of $300,000. By utilizing a cash-out refinance at an 80 percent loan-to-value (LTV) ratio, they could potentially access up to $180,000 in liquid capital. This example illustrates how substantial wealth can be unlocked and redeployed into higher-yielding assets or essential property upgrades. Using these mortgage basics to your advantage is a hallmark of sophisticated financial planning.

Opportunities for Real Estate Investors

DSCR Loan (Debt Service Coverage Ratio): This is a specialized mortgage for real estate investors that qualifies the borrower based on the cash flow generated by the property rather than personal income or employment history. It is an ideal solution for entrepreneurs and self-employed individuals who may have complex tax returns but own high-performing rental assets. Investors in California and Indiana are increasingly using DSCR loans to scale their portfolios quickly. This program simplifies the acquisition of multi-unit buildings and short-term rentals by focusing on the property's ability to cover its own debt.

Fix and Flip Financing: This refers to short-term bridge loans designed for investors who purchase distressed properties, renovate them, and sell them for a profit within a short timeframe. These loans typically cover both the purchase price and the cost of renovations, providing the leverage needed to execute complex projects. In competitive markets like Atlanta or Chicago, having access to fast, reliable capital can be the difference between securing a deal and losing it to a cash buyer. Exploring jumbo loans or non-QM options can also provide the necessary funding for higher-end renovation projects.

The current market update suggests that while rates are staying in a higher range, the stability of the labor market supports continued demand for rental housing. Investors who focus on the long-term fundamentals of cash flow and equity growth are finding success despite the broader economic headlines. Jump in and analyze your next deal by looking at the projected income and expenses to ensure the numbers work in today’s environment. Compare different loan programs to find the one that maximizes your return on investment while managing your risk exposure.

Final Market Outlook for the Weekend

As we move into the weekend, the primary focus for buyers and sellers will be on how lenders respond to the latest bond market activity. If you are currently shopping for a home or considering a refinance, it is advisable to stay in close contact with your mortgage professional to monitor rate locks. The volatility we are seeing today is a reminder that the market can shift rapidly based on a single data release. Being prepared with a pre-approval and a clear understanding of your budget will help you act decisively when you find the right property.

For those in the research phase, now is a great time to review your credit profile and gather the necessary documentation for a future application. You can even request a soft pull credit request to see where you stand without affecting your credit score. This proactive step ensures that when market conditions align with your goals, you are ready to move forward without delay. Education and preparation are your best tools for navigating the complexities of real estate finance in 2026.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664