Friday’s Interest Rate Shift: How This Week's Economic Data Influences Your Florida and California Portfolio

The mortgage market experienced a notable wave of volatility this Friday as fresh economic indicators hit the desks of traders and lenders alike. For real estate investors managing portfolios in high-stakes markets like Florida and California, understanding these shifts is essential for maintaining cash flow and long-term equity growth. This week’s data focused heavily on inflation and labor market cooling, two factors that have historically held a significant grip on the 10-year Treasury yield and, by extension, the interest rates you see at the closing table. As we navigate the midpoint of May 2026, the connection between consumer spending and borrowing costs has become increasingly transparent, requiring a more surgical approach to acquisition and refinancing.

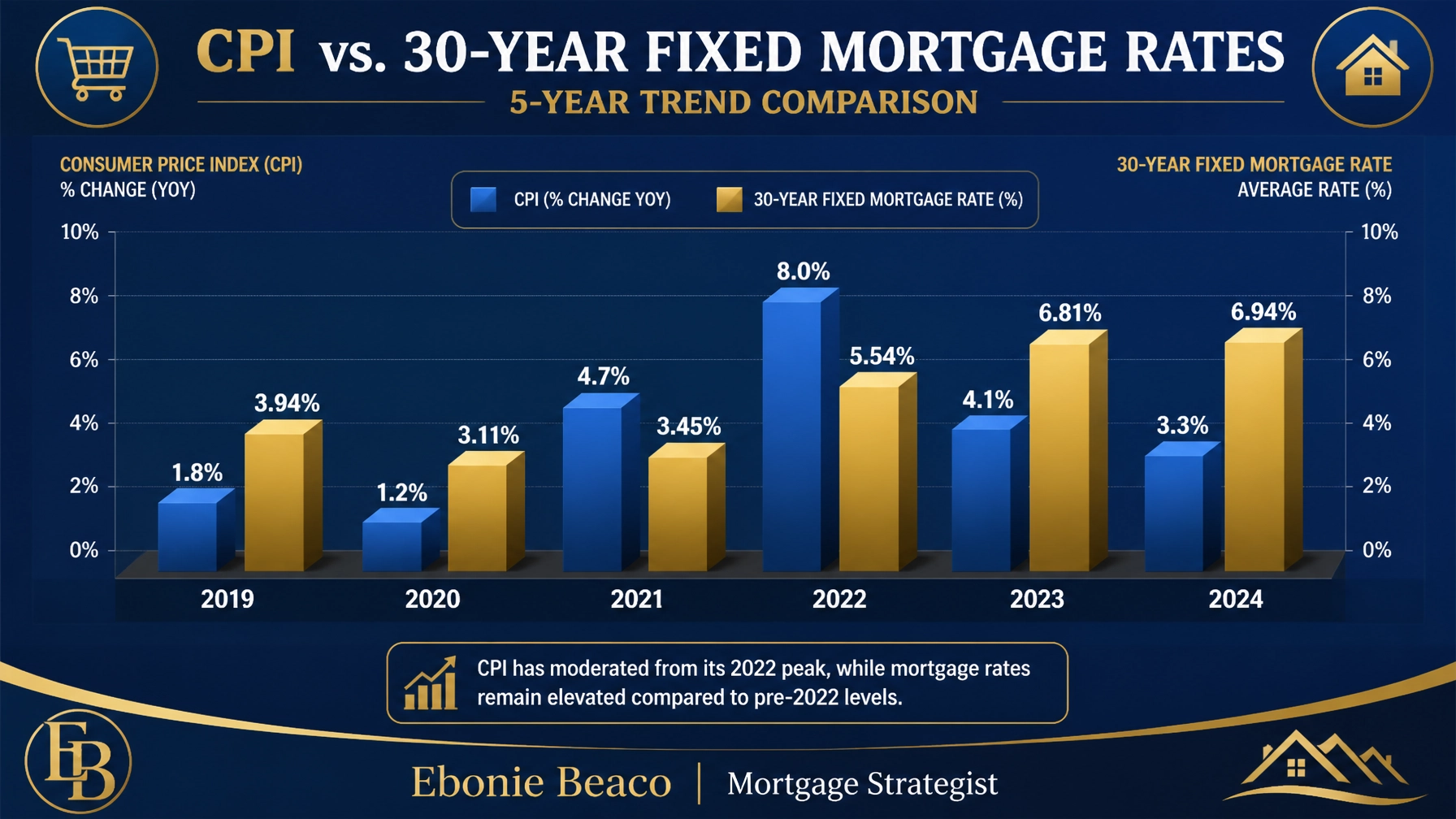

Decoding the Economic Drivers: CPI and PPI

To grasp why your mortgage quote might change within the span of a single afternoon, you must first look at the Consumer Price Index (CPI) and the Producer Price Index (PPI). These reports serve as the primary thermometers for inflation, telling the Federal Reserve whether their monetary policy is cooling the economy effectively or if further tightening is necessary. This week’s reports showed a slight divergence from expectations, which immediately triggered a response in the bond market. When inflation appears persistent, bond investors sell off, pushing yields higher and causing mortgage lenders to adjust their pricing to account for the increased risk and cost of capital.

Consumer Price Index (CPI): A measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food, and medical care.

Practical Application: If CPI remains high, mortgage rates typically rise because lenders expect the Federal Reserve to keep federal funds rates elevated to combat inflation.

Producer Price Index (PPI): A family of indexes that measures the average change over time in the selling prices received by domestic producers of goods and services.

Practical Application: PPI acts as a leading indicator for CPI, as rising costs for producers are often passed down to consumers, signaling future inflationary pressure and higher interest rates.

The Florida Frontier: Navigating High-Yield Markets

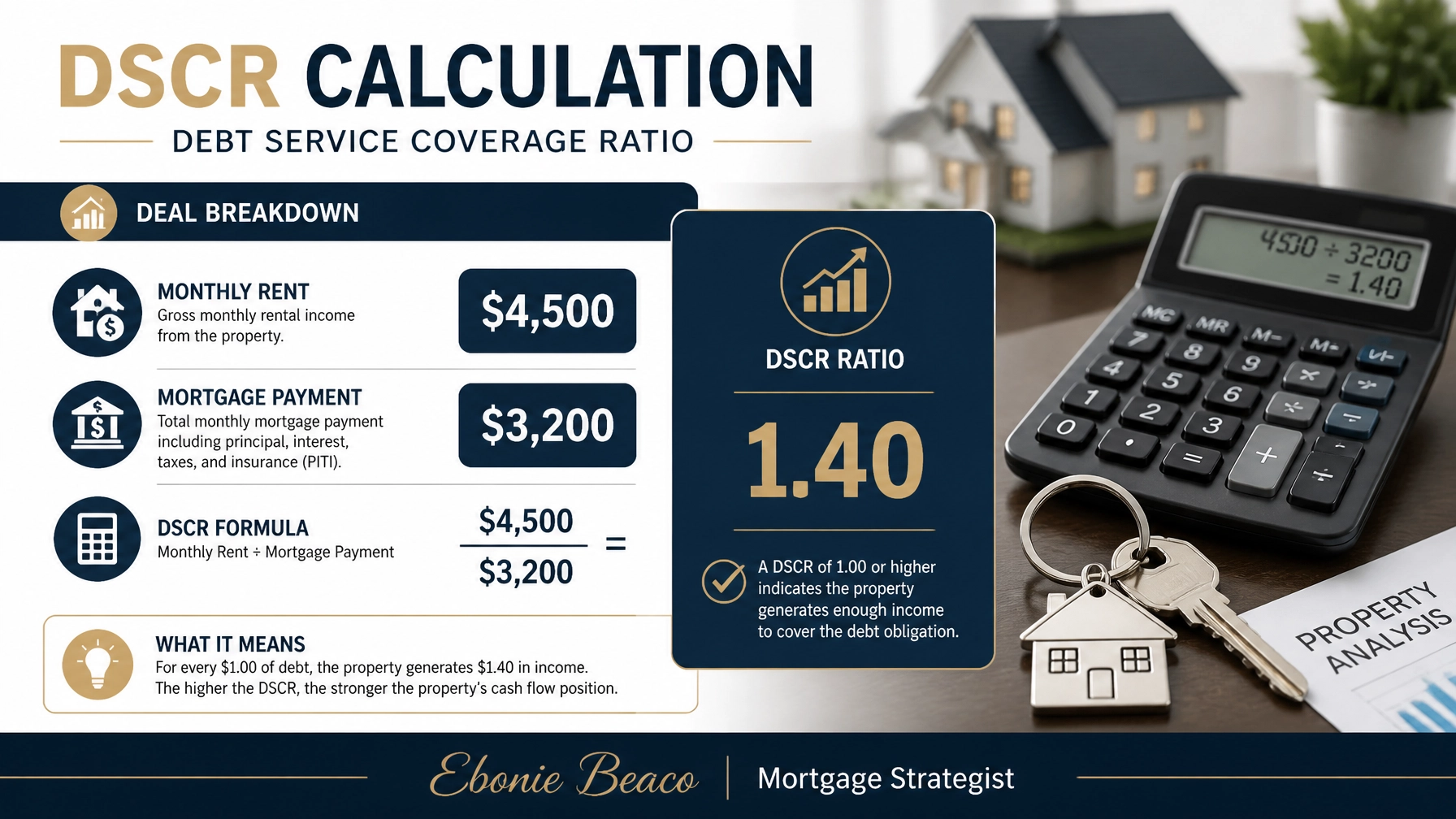

Florida continues to be a focal point for investors seeking high rental yields, particularly in the short-term rental and multifamily sectors. This week’s interest rate shift has a direct impact on how investors in the Sunshine State utilize DSCR investor loans to scale their holdings. In cities like Orlando, Tampa, and Miami, the cost of borrowing often competes with rising insurance premiums and property taxes, making the interest rate a critical component of the "Net Operating Income" equation. If you are exploring the Florida market, jumping in with a solid understanding of how a half-percentage point shift affects your debt coverage is the difference between a profitable asset and a monthly liability.

Florida investors often rely on the strength of the tourism economy to justify higher entry points, but the current rate environment demands a stricter underwriting process. Many are shifting their focus toward markets like Jacksonville or the Panhandle, where price-to-rent ratios remain more favorable despite the national upward trend in financing costs. Explore the potential of leveraging equity from existing properties through a cash-out refinance to secure more stable, long-term debt while rates are still within a manageable historical range. Accessing these funds now allows you to stay liquid as new opportunities arise in the fluctuating Florida landscape.

The California Strategy: Combating Compressed Cap Rates

In California, the real estate landscape is characterized by high asset values and compressed cap rates, which makes any shift in interest rates particularly impactful. This week’s economic data has led many California investors to reconsider traditional financing in favor of more flexible Non-QM mortgage loans. With properties in Los Angeles, San Diego, and the Bay Area often yielding lower initial cash flow, investors are increasingly utilizing interest-only payment structures to lower their monthly debt obligations. This strategy helps maintain a positive Debt Service Coverage Ratio (DSCR) while waiting for the long-term appreciation that the California market is famous for.

Another growing trend among California homeowners and investors is the development of Accessory Dwelling Units (ADUs). By adding a secondary unit to an existing property, you can significantly increase the total rental income, which helps offset the higher interest rates seen in the current market. Compare the cost of construction against the projected rental yield to see if this value-add strategy fits your portfolio goals. Many are using a HELOC / Home Equity Line of Credit to fund these additions, allowing them to tap into their home's equity without disturbing a low-rate primary mortgage.

Analyzing the Numbers: The Reality of Rate Shifts

To truly understand how this week’s interest rate shift influences your bottom line, we must look at a practical financial example. Consider an investor purchasing a four-unit building for $1,200,000. Depending on the week’s economic data, the interest rate could swing between 6.75% and 7.25%, significantly altering the property’s cash-on-cash return and its ability to qualify for specific loan programs.

Financial Scenario: 4-Unit Multifamily Acquisition

- Purchase Price: $1,200,000

- Down Payment (25%): $300,000

- Loan Amount: $900,000

- Monthly Gross Income: $10,500

- Interest Rate A (6.75%): Monthly P&I $5,837

- Interest Rate B (7.25%): Monthly P&I $6,139

In this example, the difference of 0.50% in the interest rate results in an additional $302 per month in debt service, or $3,624 annually. While this may seem manageable on a single property, when scaled across a portfolio of ten properties, that shift represents $36,240 in lost annual cash flow. This is why monitoring the 10-year Treasury yield is vital for any serious real estate professional. You can monitor daily updates through reliable resources like the Freddie Mac Primary Mortgage Market Survey to stay ahead of these shifts.

Portfolio Strategies Across the States

While Florida and California often dominate the headlines, the economic data from this week influences investment activity across all the states where we provide guidance. In Alabama and Arkansas, where entry prices are lower, investors are using fix-and-flip loans to capitalize on the housing shortage. In Georgia and Virginia, the demand for suburban single-family rentals remains high, attracting BRRRR (Buy, Rehab, Rent, Refinance, Repeat) investors who need predictable exit financing. Meanwhile, in Michigan, Indiana, and Illinois, the focus often shifts to workforce housing and industrial real estate, where interest rate stability is key to long-term lease negotiations.

Missouri and Kentucky investors are also seeing a shift toward commercial real estate and mixed-use properties. Financing these assets requires a deep understanding of how global economic trends filter down into local rent rolls. Regardless of where your properties are located, the goal remains the same: align your financing strategy with the specific economic climate of the moment. By staying informed on CPI and PPI data, you can anticipate rate movements and lock in financing before volatility strikes.

Looking Ahead: Building Wealth Through Strategy

The interest rate shift witnessed this Friday serves as a reminder that the real estate market is never static. For homeowners, realtors, and investors, the ability to adapt to new data is a competitive advantage. Whether you are looking at a cash-out refinance to consolidate debt or a DSCR loan to acquire your next rental property, the strategy you choose must be rooted in the current economic reality. Education and transparency are the tools that allow you to move with confidence, even when the headlines suggest uncertainty.

Jump in and review your current portfolio’s debt structure. Are there opportunities to refinance out of high-interest bridge loans? Could a HELOC provide the liquidity you need for your next California ADU or Florida vacation rental? By analyzing your options through the lens of this week’s economic data, you position yourself to build lasting wealth. Stay focused on the long-term goal of homeownership and investment success, using each market shift as a stepping stone toward financial independence.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664