Florida Investment Strategy: Navigating the Impact of Today’s Fed Signals on Mortgage Rates

As we move through the first week of June 2026, the real estate landscape in Florida is facing a pivotal moment. Investors, homeowners, and real estate professionals are all closely watching the signals coming from the Federal Reserve. For anyone active in the Florida market, whether you are managing a short term rental in Orlando or looking at multifamily units in Tampa, understanding these economic shifts is essential for maintaining a profitable portfolio. The current environment is defined by a "hold and wait" approach from central bankers, which has a direct influence on the financing options available to you today.

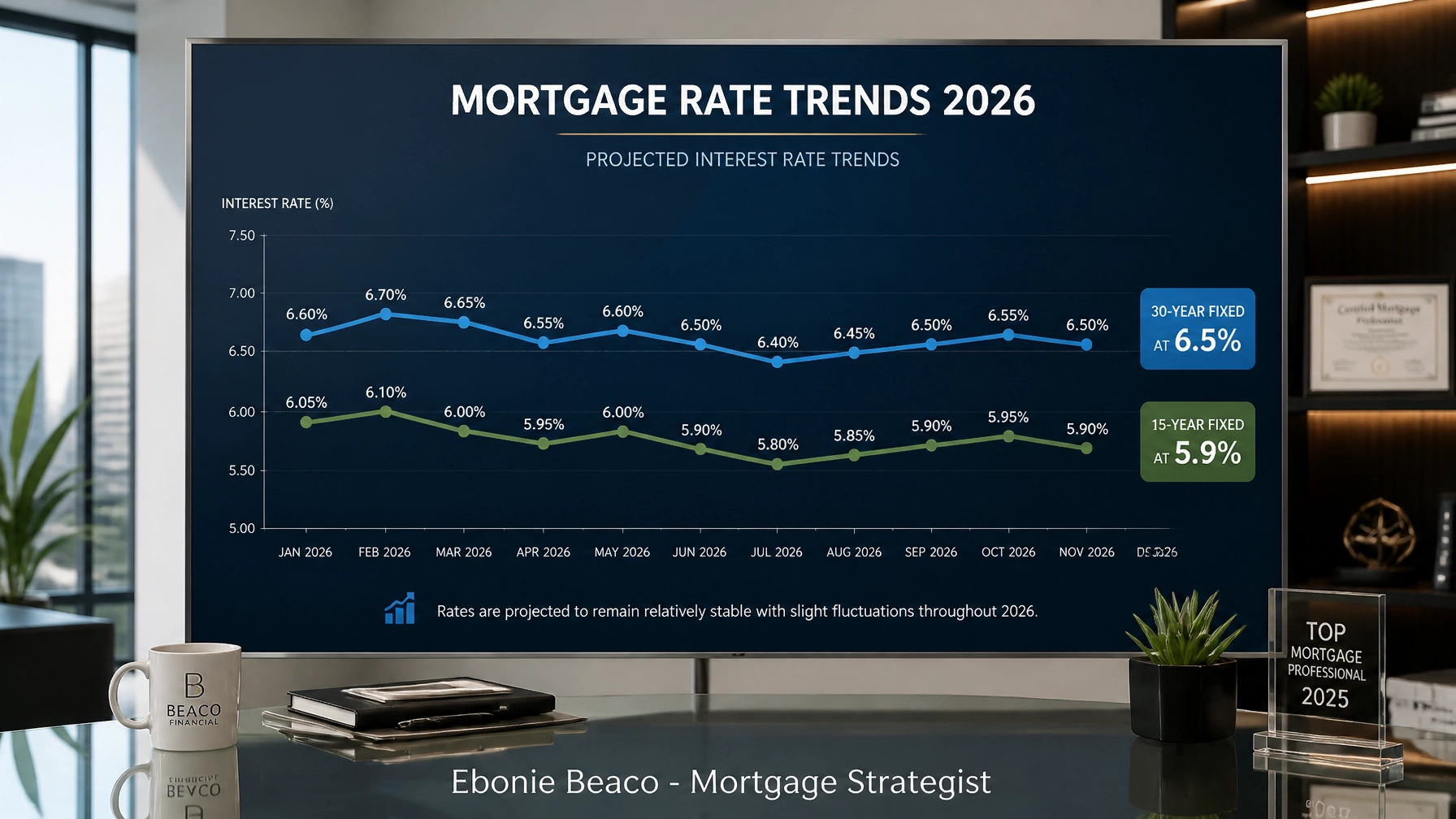

The transition from the optimistic rate environment of 2025 to the more cautious stance we see now has changed the math for many deals. We are seeing 30 year fixed mortgage rates settle in the mid 6% range, a significant shift from the volatility experienced earlier this year. For Florida investors, this means that the focus must shift from speculative appreciation to sustainable cash flow. Navigating these waters requires a clear understanding of why rates are behaving this way and how you can position your financing to stay ahead of the curve.

Decoding the June 2026 Fed Signals

The Federal Reserve is scheduled to meet on June 16 and 17, and the consensus among economists is almost unanimous. Current data suggests a 99% probability that the Fed will maintain the federal funds target range at 3.50% to 3.75%. This stability might seem like good news at first glance, but the subtext of their communication remains hawkish. The "higher for longer" narrative is still very much in play because inflation has not yet reached the Fed's long term targets.

Market participants are paying close attention to the press conference that will follow the meeting. Even without a formal rate hike, the language used by Fed officials can cause immediate ripples in the bond market. If the Fed emphasizes that inflation is still a concern, we could see the 10 year Treasury yield rise, which often leads to higher mortgage rates for consumers. This is why many experts suggest that mortgage interest rates could climb even without a formal move from the central bank. You can find more detailed daily updates on these trends at The Mortgage Reports.

Current Mortgage Rate Trends and National Context

As of June 4, 2026, the national average for a 30 year fixed purchase mortgage is approximately 6.516%. This is slightly lower than the peaks we saw a few months ago, but it remains higher than the rates available late last year. For those looking at shorter terms, the 15 year fixed rate is hovering around 5.89%, providing a more aggressive path for those looking to build equity quickly. Adjustable rate mortgages, such as the 5/1 ARM, are averaging around 5.67%, which may appeal to investors with a specific exit strategy in mind.

It is important to note that refinance rates are currently tracking slightly higher than purchase rates. The national average for a 30 year refinance is about 6.66% today. This gap exists because lenders are pricing in the additional risks and costs associated with refinancing in a range bound market. For a comprehensive look at how these rates are trending, Bankrate provides a deep dive into the weekly surveys that many industry professionals use for benchmarking.

The Florida Real Estate Landscape

Florida remains one of the most dynamic real estate markets in the country, but it is not immune to these national interest rate pressures. In cities like Miami, Tampa, and Orlando, the demand for housing continues to be driven by strong population growth and a robust tourism sector. However, the higher cost of borrowing means that buyers are becoming more selective. This shift in buyer behavior is actually creating opportunities for savvy investors who can negotiate more favorable terms on property prices or seller concessions.

When you look at the different submarkets within Florida, the impact of these rates varies. In South Florida, luxury and high end condos are seeing a slight cooling as high financing costs deter some domestic buyers. Meanwhile, in Central Florida, the demand for workforce housing and long term rentals remains high. Investors who focus on these resilient sectors are finding that they can still achieve strong returns if they use the right loan programs tailored for investment properties.

Financing Strategies for Florida Investors

In a 6.5% rate environment, the financing strategy you choose can make or break your investment. One of the most popular options for Florida landlords right now is the DSCR (Debt Service Coverage Ratio) loan. This program allows you to qualify for financing based on the rental income of the property rather than your personal income or tax returns. This is particularly beneficial for self employed investors or those with large portfolios who may have high DTI (Debt to Income) ratios on paper.

Another strategy being used by homeowners in Florida is accessing equity through a home refinance. While rates are higher than they were two years ago, the appreciation in Florida home values has been so significant that many owners have hundreds of thousands of dollars in "trapped" equity. A cash out refinance can provide the capital needed for property renovations or as a down payment on a second investment property. By using a conventional loan, you can lock in a stable rate and use that capital to expand your wealth.

The Math of a Florida DSCR Deal

To understand how these rates translate into real numbers, let’s look at a typical scenario for a short term rental property in Orlando. Imagine you are purchasing a property for $450,000. With a 20% down payment, your loan amount would be $360,000. At today’s rates of roughly 6.5%, your monthly principal and interest payment would be approximately $2,275. After adding taxes, insurance, and HOA fees, your total monthly PITIA (Principal, Interest, Taxes, Insurance, Association) might come to around $3,200.

For a DSCR loan to work, the lender will look at the projected rental income. If this property generates $4,500 in monthly rent, your DSCR would be 1.4x ($4,500 divided by $3,200). Most lenders are looking for a ratio of 1.2x or higher, so this deal would comfortably qualify. This extra cushion provides a safety net for the investor and the lender, ensuring that the property remains self sustaining even if rates drift slightly higher.

Risk Mitigation and Insurance Factors

No discussion about Florida real estate is complete without addressing insurance. Rising insurance premiums and the availability of coverage for flood and windstorm damage are critical factors in your overall investment strategy. These costs are part of your operating expenses and directly impact your cash flow and your ability to qualify for certain mortgage products. When you are underwriting a deal, it is vital to get an accurate insurance quote early in the process so that your math remains solid.

Furthermore, climate resilience is becoming a bigger factor for lenders and appraisers. Newer construction that meets stricter building codes may often be easier to finance and insure than older properties. By focusing on properties that are built to withstand the elements, you are not just protecting your physical asset, but also your long term financial stability. Combining a solid property choice with a strategic mortgage plan allows you to navigate the current high rate environment with confidence.

Preparing for Future Market Shifts

Looking ahead, the Mortgage Bankers Association and other industry leaders expect rates to remain range bound or even rise slightly through the remainder of 2026. This means that waiting for a dramatic drop in rates might result in missed opportunities as property values continue to climb in high demand Florida markets. The strategy for most successful investors today is to buy the property at a rate that makes sense now, with the intention of refinancing later if a significant downward shift occurs.

Using tools like a HELOC or a bridge loan can also provide the flexibility needed to act quickly when a deal presents itself. These short term financing solutions can bridge the gap while you wait for more permanent financing or until you complete a value add renovation. The key is to stay informed about the Fed's next moves and to maintain a close relationship with a mortgage strategist who understands the local market nuances in Florida and across the other states we serve, including Michigan, Georgia, and Virginia.

Final Thoughts on Your Florida Strategy

The "hold and wait" signal from the Federal Reserve does not mean that your investment strategy should be on hold. Instead, it is a call for more diligent underwriting and a focus on deal structures that do not rely on aggressive rate cuts. By understanding the data, utilizing programs like DSCR loans, and managing your risks effectively, you can continue to build wealth through Florida real estate even in a 6.5% mortgage rate environment.

If you are ready to explore how these financing strategies can be applied to your specific goals, we are here to provide the guidance you need. Whether you are a first time homebuyer or a seasoned investor looking to scale your portfolio, having a plan that aligns with today's economic reality is the first step toward long term success.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664