Florida DSCR Loan Lender: Why DSCR is King in the Sunshine State

Florida represents a unique frontier for real estate investors. From the neon lights of Miami to the family-friendly sprawl of Orlando and the coastal charm of the Gulf, the Sunshine State offers a rental market that rarely sleeps. If you are looking to grow a portfolio here, you have likely run into a common wall: traditional bank financing.

Conventional loans often demand stacks of tax returns, debt-to-income (DTI) checks, and endless proof of personal employment. For the aggressive investor or the self-employed entrepreneur, these requirements can stall a deal faster than a summer thunderstorm. This is where the DSCR loan takes the throne.

In Florida, the Debt Service Coverage Ratio (DSCR) loan is king because it shifts the focus from your personal bank account to the property’s ability to generate cash.

Defining the DSCR Loan

Debt Service Coverage Ratio (DSCR) Loan: A mortgage product specifically for investment properties that qualifies the borrower based on the rental income generated by the asset rather than personal income or employment history.

Practical Application: If you are a self-employed investor with high tax write-offs, you can qualify for this loan because the lender looks at the property's gross rent to see if it covers the monthly mortgage payment.

Why Florida Investors Choose DSCR Over Everything Else

Florida’s economy is heavily driven by tourism and a constant influx of new residents. This creates a high-velocity rental market. Whether you are looking at long-term annual leases or short-term vacation rentals (STRs), the cash flow potential is significant.

No Personal Income Verification

Traditional lenders want to see your W-2s and pay stubs. They calculate your DTI to ensure you aren't overleveraged. For many real estate professionals, their taxable income looks lower than their actual cash flow due to smart accounting. With a DSCR Investor Loan, your personal income is essentially invisible to the underwriter.

Unlimited Portfolio Scaling

If you use conventional financing, you typically hit a "ceiling" after 10 properties. Fannie Mae and Freddie Mac have strict limits on how many financed properties one individual can hold. In the Florida market, where building a large portfolio is the goal, this limit is a deal-breaker. DSCR loans allow you to scale without these arbitrary caps.

Close in an LLC

Asset protection is a major priority for Florida landlords. DSCR lenders allow you to close the loan under a business entity, such as an LLC. This separates your personal liability from your real estate holdings, a strategy many investors use to safeguard their family’s wealth. You can explore more about how this fits into the overall loan process to prepare your business for its next acquisition.

Visual Description: A financial breakdown showing a Florida property with a $3,500 monthly rental income and a $2,800 total monthly payment (PITIA), resulting in a DSCR of 1.25. The graphic includes labels for "Cash Flow Positive" and "DSCR Qualification Success". Title: 'Florida DSCR Loan Lender'. Bottom: 'Ebonie Beaco - Mortgage Loan Officer'.

Visual Description: A financial breakdown showing a Florida property with a $3,500 monthly rental income and a $2,800 total monthly payment (PITIA), resulting in a DSCR of 1.25. The graphic includes labels for "Cash Flow Positive" and "DSCR Qualification Success". Title: 'Florida DSCR Loan Lender'. Bottom: 'Ebonie Beaco - Mortgage Loan Officer'.

The Math Behind the Crown: Calculating Your DSCR

To understand why this product is so effective, you have to look at the math. Lenders use a simple formula to determine if a property qualifies.

The Formula: Gross Monthly Rent / Monthly PITIA (Principal, Interest, Taxes, Insurance, and HOA dues).

Let’s look at a real-world Florida example:

- Purchase Price: $450,000

- Down Payment (20%): $90,000

- Loan Amount: $360,000

- Estimated Monthly PITIA: $2,900

- Market Rent (Long-term): $3,600

The Calculation: $3,600 / $2,900 = 1.24 DSCR

A ratio of 1.0 means the property breaks even. Anything above 1.0 is considered cash-flow positive. Most lenders look for a ratio of 1.20 or higher to offer the most competitive rates, though "no-ratio" programs exist for properties that don't quite meet that mark but have high equity. You can use our mortgage calculators to run these numbers for your specific Florida leads.

Short-Term Rentals: The Florida Advantage

Florida is the global capital for Airbnb and Short-Term Rental Financing. In markets like Kissimmee, Destin, or Fort Lauderdale, the income from a vacation rental often dwarfs what a long-term tenant would pay.

Many traditional lenders struggle to quantify Airbnb income. However, specialized DSCR lenders in Florida can use "AirDNA" data or short-term rental market projections to qualify the loan. This allows you to purchase a high-yield vacation property based on its projected nightly success rather than just the local 12-month lease averages.

Qualifications for a Florida DSCR Loan

While you don't need tax returns, you do need to meet certain criteria to access these programs.

- Credit Score: Most programs require a minimum score of 620, though better rates kick in at 700+.

- Down Payment: Expect to put down 15% to 25%. The more equity you have, the lower your ratio requirements might be.

- Appraisal and Rent Schedule: The lender will order an appraisal that includes a "1007 Rent Schedule" to verify the fair market rent for the area.

- Cash Reserves: Lenders often want to see 3 to 6 months of PITIA in a liquid account to ensure you can handle a vacancy.

Access our FAQ to see common questions about liquidity and credit requirements for investor-specific products.

Strategies for the Florida Market

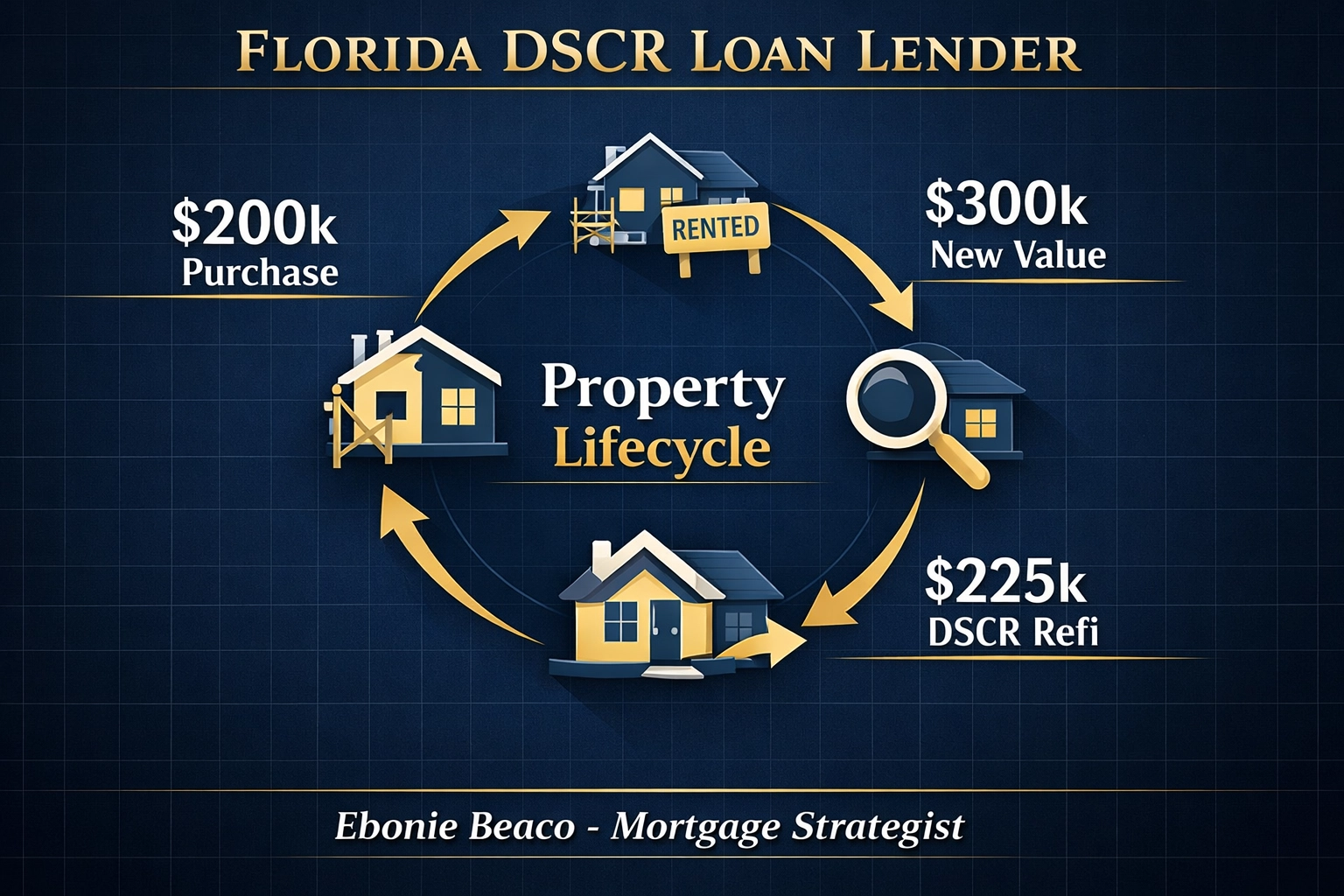

The BRRRR Method

Buy, Rehab, Rent, Refinance, Repeat. Florida has plenty of older homes in prime locations. Investors use Hard Money Loans or Bridge Loans to acquire and renovate these properties. Once the property is renovated and a tenant is in place, they use a DSCR Cash-Out Refinance to pull their original capital back out.

Because DSCR loans focus on the new appraised value and the new rental income, you can often recover your entire initial investment to fund your next Florida deal.

Cash-Out Refinance for Portfolio Growth

If you already own a rental property in Florida that has appreciated in value, you can use a home refinance strategy to tap into that equity. Pulling cash out of a stabilized asset via a DSCR loan is a streamlined way to get the down payment for your next two or three units.

Visual Description: A flow chart showing the BRRRR method. Step 1: Purchase/Rehab ($200k). Step 2: New Appraised Value ($300k). Step 3: DSCR Refinance at 75% LTV ($225k). Step 4: Original Capital Returned ($25k profit + original investment). Title: 'Florida DSCR Loan Lender'. Bottom: 'Ebonie Beaco - Mortgage Loan Officer'.

Visual Description: A flow chart showing the BRRRR method. Step 1: Purchase/Rehab ($200k). Step 2: New Appraised Value ($300k). Step 3: DSCR Refinance at 75% LTV ($225k). Step 4: Original Capital Returned ($25k profit + original investment). Title: 'Florida DSCR Loan Lender'. Bottom: 'Ebonie Beaco - Mortgage Loan Officer'.

Navigating the Florida Insurance Crisis

One unique aspect of lending in Florida is the insurance landscape. To maintain a healthy DSCR, you must manage your PITIA. Rising homeowners' insurance premiums in Florida can squeeze your ratio.

When you work with a specialist who understands the Florida market, we look at the full picture. We help you structure the loan: perhaps by adjusting the down payment or looking at different interest-only options: to ensure the property remains a viable investment despite local insurance costs. Transparency in these numbers is essential for long-term success.

Why Work with a Mortgage Strategist?

Real estate is more than just a transaction; it is a wealth-building journey. Whether you are a seasoned landlord with a 50-unit portfolio or a first-time investor looking at a duplex in Tampa, you need a strategist who understands the nuances of Non-QM Mortgage Loans.

We don't just "process" applications; we structure deals. If a property doesn't quite meet the 1.20 ratio, we explore interest-only payments to lower the monthly "debt service," thereby raising the DSCR and helping you qualify.

Jump in and explore our about us page to learn how we prioritize transparency and education for every investor we partner with.

Take the Next Step in the Sunshine State

The Florida market moves fast. Opportunities in emerging neighborhoods don't wait for 60-day bank approvals. DSCR loans offer the speed, flexibility, and scalability that modern investors demand.

If you want to compare options or need a clear path to your next closing, let’s talk. Whether you need a loan for a new purchase or are looking for mentoring on how to navigate the complex world of real estate finance, the Home Loans Network is here to guide you.

Explore our online forms to start your scenario review today.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664