Florida DSCR Loan Lender vs. Traditional Banks: Which Is Better for Your Rental Property?

SEO Title: Florida DSCR Loan Lender vs. Traditional Banks: Which Is Better for Your Rental Property?

Meta Description: Compare Florida DSCR loans vs. traditional banks for rental properties. Learn about requirements, DSCR ratios, and the best financing for your Florida investment portfolio in 2026.

URL Slug: florida-dscr-loan-lender-vs-traditional-banks

Featured Image Recommendation: A high-quality landscape photo of a luxury modern coastal rental property in Florida with palm trees and a swimming pool at sunset with REI Vault Pro branding.

SEO Alt Text: Professional landscape of a Florida luxury rental property used to illustrate DSCR vs traditional bank financing.

Social Media Excerpt: Choosing between a DSCR loan and a traditional bank in Florida? One focuses on your income, the other on the property's performance. Here is how to decide which is better for your rental portfolio in 2026.

SEO Tags: Florida DSCR Loan, Real Estate Financing, Rental Property Loans, Traditional Bank vs DSCR, Investor Loans Florida, DSCR Ratio, Real Estate Investing 2026.

Navigating the Florida real estate market requires more than just finding the right property; it requires choosing the right financing vehicle to fuel your growth. For investors looking to acquire or refinance rental properties in 2026, the primary fork in the road often leads to a choice between a traditional bank and a Florida DSCR loan lender.

The decision affects your ability to scale, your monthly cash flow, and the level of personal documentation you must provide. While traditional banks have long been the default choice for many, the rise of investor-specific lending has introduced powerful alternatives that prioritize the performance of the asset over the personal financial history of the borrower.

Understanding the Core Financing Models

Choosing the right loan depends on your specific financial profile and your long-term investment goals. To compare these options, you must first understand the fundamental differences in how each lender evaluates risk.

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its debt payments based solely on its gross rental income.

DTI (Debt-to-Income Ratio): A calculation used by traditional banks to determine how much of a borrower's personal gross monthly income goes toward paying existing and new debts.

Traditional banks typically focus on you, the individual. They analyze your W-2s, tax returns, and current debt obligations. Conversely, a Florida DSCR loan lender focuses on the property. If the rental income covers the mortgage payment, the deal moves forward.

Comparing Traditional Banks and DSCR Loans in Florida

The Florida market is unique due to its high concentration of short-term rentals and high-growth metropolitan areas like Orlando, Miami, and Tampa. Each financing path offers distinct advantages depending on your strategy.

1. Qualification and Documentation

Traditional banks require a comprehensive "paper trail." This includes two years of tax returns, 30 days of pay stubs, and a deep dive into your personal debt-to-income ratio. If you are a self-employed investor or have significant tax write-offs that lower your adjusted gross income, you may find it difficult to qualify for a traditional bank loan even if you have millions in assets.

DSCR lenders simplify this process. There is no employment verification and no personal income requirement. You can access the AI Deal Analyzer to see how your property's potential rent stacks up against its debt service without worrying about your personal W-2 status.

2. Scaling Your Portfolio

Traditional banks often have a "cap" on the number of financed properties a single borrower can hold, typically limited to 10. Once you reach this limit, conventional financing becomes nearly impossible.

Florida DSCR loans do not have these same limitations. Because each loan is underwritten based on the individual property’s performance, you can continue to acquire new properties as long as they meet the required DSCR ratio. This is essential for investors looking to build large-scale portfolios across Florida, Alabama, or Georgia.

3. Ownership and Vesting

Many professional investors prefer to hold their properties in an LLC or a corporate entity to protect their personal assets. Traditional bank loans often require you to close the loan in your personal name, which can create liability risks.

DSCR lenders encourage closing in an LLC. This allows for cleaner accounting and better legal protection for your real estate business. If you are serious about building a professional brand, you should join the REI Vault Pro community to learn how to structure your entities for maximum efficiency.

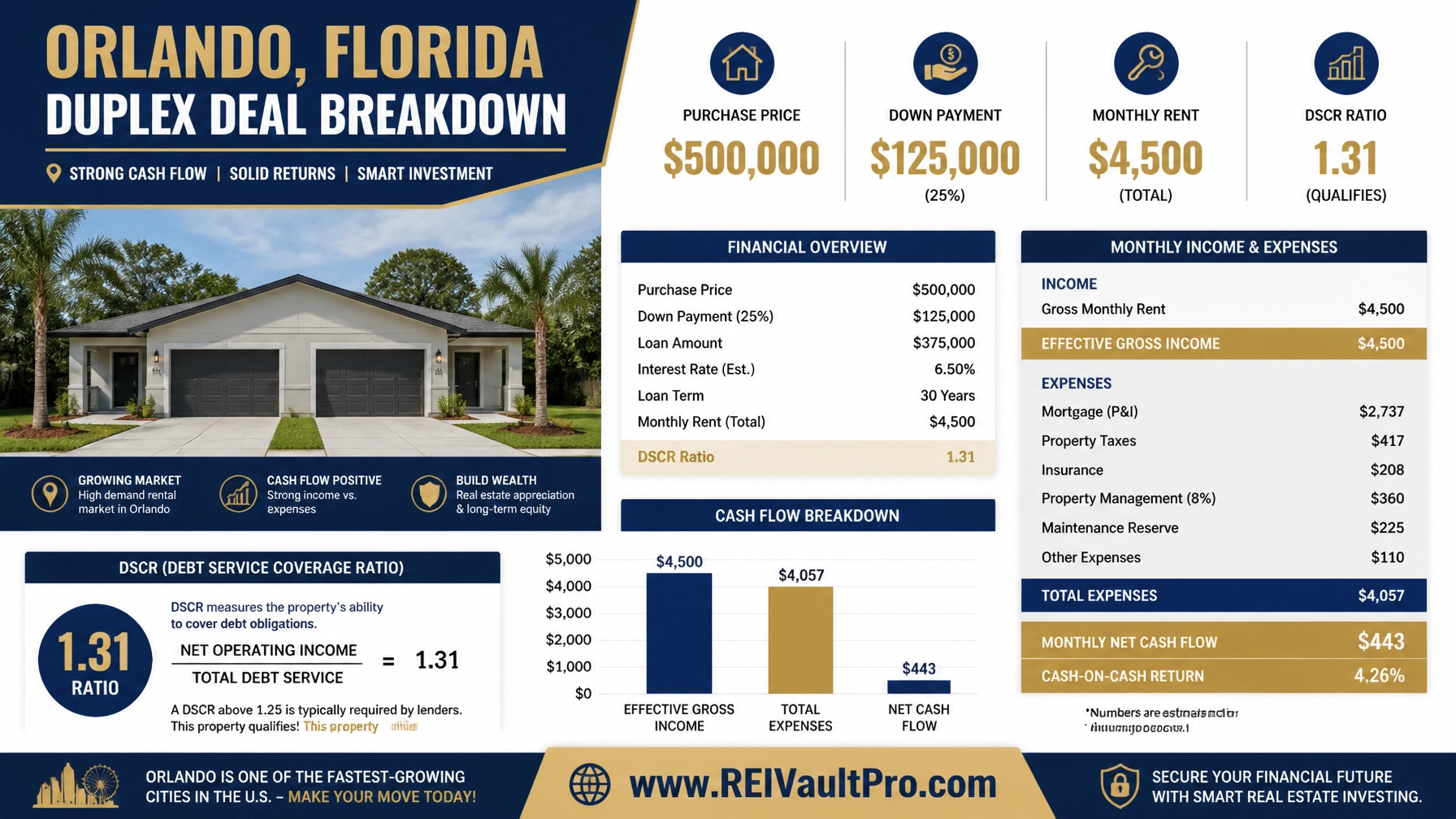

Calculating the Numbers: An Orlando Duplex Example

To see how a DSCR loan works in a real-world scenario, let's look at a typical investment in the Orlando, Florida market.

Imagine you are purchasing a duplex for $500,000. You plan to put down 25% ($125,000) and finance the remaining $375,000.

- Purchase Price: $500,000

- Loan Amount: $375,000

- Estimated Interest Rate (June 2026): 7.5%

- Monthly Principal & Interest: $2,622

- Monthly Taxes, Insurance, & HOA: $800

- Total Monthly PITIA: $3,422

- Gross Monthly Rental Income: $4,500

To find the DSCR, you divide the gross monthly rent by the total monthly payment:

$4,500 / $3,422 = 1.31

Because the ratio is 1.31, the property "covers" its debt service with a 31% buffer. Most Florida DSCR lenders look for a ratio of 1.25 or higher, making this an ideal candidate for investor financing.

Why Florida Investors Choose DSCR Lenders

The Florida rental market is heavily influenced by tourism and seasonal migration. This creates a high demand for short-term rental (STR) properties.

Short-Term Rental (STR) Financing: A specific type of DSCR loan where the lender uses projected Airbnb or VRBO income rather than a standard long-term lease to calculate the ratio.

Traditional banks are often hesitant to finance short-term rentals because the income can be variable. However, advanced AI tools allow DSCR lenders to analyze STR market data to confirm the property's earning potential. This flexibility is a game-changer for investors in coastal regions or near major attractions.

When a Traditional Bank Might Be the Better Option

Despite the flexibility of DSCR loans, traditional banks still serve a purpose. If you have a stable W-2 job, excellent credit, and you are only looking to buy your first or second rental property, a traditional bank may offer a slightly lower interest rate.

Conventional loans are generally the most cost-effective if you meet the following criteria:

- You have a low DTI (Debt-to-Income) ratio.

- You can provide full tax documentation.

- The property is a standard long-term rental.

- You do not mind having the debt reported on your personal credit profile.

However, for those looking for speed and the ability to scale without personal income constraints, the DSCR model remains the superior choice for professional real estate investors.

Integrating Technology into Your Financing Strategy

Modern real estate investing requires modern tools. Whether you are comparing loan programs or estimating the renovation costs of a new acquisition, leveraging data is the key to maintaining a competitive edge.

Using an AI Deal Analyzer allows you to run multiple scenarios in seconds. You can compare the cash flow of a property under a traditional bank loan versus a DSCR loan, helping you decide which path leads to the highest return on investment.

Related REI Vault Pro Resources

To help you refine your investment strategy and choose the best financing for your Florida portfolio, explore these essential tools:

- AI Deal Analyzer: This tool automates the calculation of DSCR, Cap Rate, and ROI. It helps you quickly determine if a Florida rental property will qualify for investor financing.

- Pro Investor Membership: Access advanced market analytics and funding strategies specifically designed for scaling multi-property portfolios.

- REI Vault Pro Demo: Watch a full walkthrough of our software suite to see how we help investors identify and fund high-performing deals.

- AI Tools Suite: A collection of calculators and simulators to help you estimate everything from rental yields to bridge loan costs.

Choosing Your Path to Wealth

The Florida real estate market continues to offer incredible opportunities for those who understand how to leverage debt effectively. By comparing the rigid requirements of traditional banks against the asset-based flexibility of DSCR lenders, you can choose the financing that best aligns with your financial profile.

If you are ready to stop relying on tax returns and start focusing on the potential of your properties, it is time to explore the world of investor-focused lending. The right financing strategy can be the difference between owning one rental and owning a portfolio that provides true financial freedom.

Start a Free Trial with REI Vault Pro today to analyze your next Florida deal and access the financing tools you need to succeed.

FAQ Section

What is the minimum credit score for a Florida DSCR loan?

Most lenders require a minimum credit score of 640 to 660. However, to secure the most competitive interest rates and lower down payment requirements, a score of 720 or higher is typically recommended.

Can I use a DSCR loan for a property I plan to live in?

No. DSCR loans are strictly for business purposes and investment properties. You cannot occupy the property at any time. For a primary residence, you must use traditional bank financing or a government-backed loan.

How much down payment is required for a Florida DSCR loan?

Investors should expect to put down between 20% and 25%. Some programs may allow for lower down payments if the property has an exceptionally high DSCR ratio or if the borrower has a significant amount of experience in the market.

Does a DSCR loan affect my personal credit?

While the lender will check your credit during the application process, many DSCR loans are closed in the name of an LLC and do not report to your personal credit bureau. This helps keep your personal DTI low for other financing needs.

Are interest rates higher for DSCR loans than traditional bank loans?

Generally, yes. Because DSCR loans offer more flexibility and require less documentation, they typically carry an interest rate that is 0.75% to 1.5% higher than a conventional investment property loan.