Fix and Flip Loans 101: Funding Your Atlanta Projects

If you have spent any time driving through neighborhoods in Atlanta, Augusta, or Savannah, you have likely seen them: the distressed bungalows and dated mid-century homes tucked away, waiting for someone to bring them back to life. For many real estate investors, these properties represent more than just a renovation project; they are the foundation of a profitable business.

However, the biggest hurdle to scaling a renovation business isn't usually finding the house or the contractor: it is securing the capital to move quickly. Traditional bank loans often shy away from properties in poor condition, and they certainly don't move at the speed of the Georgia real estate market.

This is where fix and flip loans enter the picture. These are specialized, short-term financing tools designed specifically for the "buy, renovate, and sell" model.

What are Fix and Flip Loans?

Fix and Flip Loans: A category of short-term, asset-based financing used by real estate investors to purchase and improve a property before reselling it for a profit.

Practical Application: These loans allow you to acquire a property that a traditional lender would reject due to its physical condition, while also providing the capital needed for repairs.

When you use this type of financing, the lender looks primarily at the property's potential value rather than just your personal debt-to-income ratio. This focus on the "After Repair Value" (ARV) is what makes fix and flip lending the lifeblood of the investment community. You can explore your options and see how these fit into your overall strategy at Home Loans Network.

How the Funding Structure Works

Most fix and flip loans are structured in two distinct parts to protect both the lender and the investor.

The Initial Advance

This covers a percentage of the purchase price. In most scenarios, a lender might cover 80% to 90% of the acquisition cost. You, the investor, bring the remaining 10% to 20% as your "skin in the game."

The Rehab Holdback

This is the money earmarked for your renovations. Unlike the purchase funds, which are released at the closing table, rehab funds are usually held in escrow and released in "draws" as specific milestones of the project are completed.

Jump in and learn more about how this timing impacts your cash flow on our mortgage basics page.

The Power of the ARV Calculation

Understanding your numbers is the difference between a successful flip and a financial headache. Lenders use a specific formula to determine how much they are willing to lend on a project. This is typically referred to as the 75% Rule.

The goal is to ensure that your total investment (Purchase + Rehab) does not exceed 75% of the estimated value of the home once it is fully renovated.

Example Scenario:

- Property Purchase Price: $200,000

- Estimated Renovation Costs: $60,000

- Estimated After Repair Value (ARV): $350,000

If we apply the 75% rule to the ARV: $350,000 x 0.75 = $262,500.

Since your total cost is $260,000 ($200k purchase + $60k rehab), this project fits safely within the lending guidelines. You can run your own numbers using our mortgage calculators to see how your specific deal stacks up.

Image Description: A clean financial breakdown graphic titled 'Fix and Flip Loans 101'. It displays the calculation: ARV ($350,000) x 75% = $262,500 Max Loan/Total Cost. Below this, it lists Purchase: $200,000 and Rehab: $60,000. At the bottom, it reads: Ebonie Beaco - Mortgage Loan Officer.

Image Description: A clean financial breakdown graphic titled 'Fix and Flip Loans 101'. It displays the calculation: ARV ($350,000) x 75% = $262,500 Max Loan/Total Cost. Below this, it lists Purchase: $200,000 and Rehab: $60,000. At the bottom, it reads: Ebonie Beaco - Mortgage Loan Officer.

Why Atlanta is a Hub for House Flipping

The Georgia market, particularly the Atlanta metropolitan area, remains a prime target for fix and flip investors. The combination of aging housing stock in desirable school districts and a steady influx of new residents creates a "perfect storm" for value-add real estate.

Investors in cities like Atlanta need to move fast. When a distressed property hits the market, there are often multiple offers within hours. Fix and flip loans provide the speed necessary to compete with cash buyers. While a traditional mortgage might take 30 to 45 days to close, a fix and flip loan can often be funded in 7 to 10 days.

Accessing this speed is vital for wholesalers and rehabbers who need to close quickly to secure a deep discount on the purchase price. You can see our full loan process here to understand how we streamline these closings.

Key Features of Fix and Flip Financing

If you are transitioning from traditional home buying to investing, the terms of these loans will look very different from what you are used to.

- Short Terms: These loans typically last between 6 and 18 months. They are bridge solutions, not 30-year commitments.

- Interest-Only Payments: To keep your monthly carrying costs low while you aren't receiving rent, most fix and flip loans only require interest payments during the term.

- No Prepayment Penalties: Most of these programs allow you to pay off the loan as soon as the house sells without charging you a fee for finishing early.

- Speed Over Paperwork: While your credit and experience are reviewed, the property’s profitability is the primary driver of the approval.

Compare these features against other investment options like DSCR rental property loans if you are considering keeping the property as a long-term rental instead of selling it.

The Rehab Draw Process Explained

One of the most common questions new investors ask is: "How do I actually get the money for the repairs?"

Lenders do not simply hand over $60,000 in cash at closing. Instead, you follow a draw schedule.

- Work Completion: You or your contractor complete a specific phase of work (e.g., plumbing and electrical rough-in).

- Inspection: You notify the lender, and they send an inspector to verify the work is done.

- Fund Release: The lender releases the portion of the rehab budget allocated to that phase.

This system ensures the project stays on track and that the funds are actually being used to increase the property's value. If you have questions about how to manage your first draw, check our about us section to see how we guide our clients through their first projects.

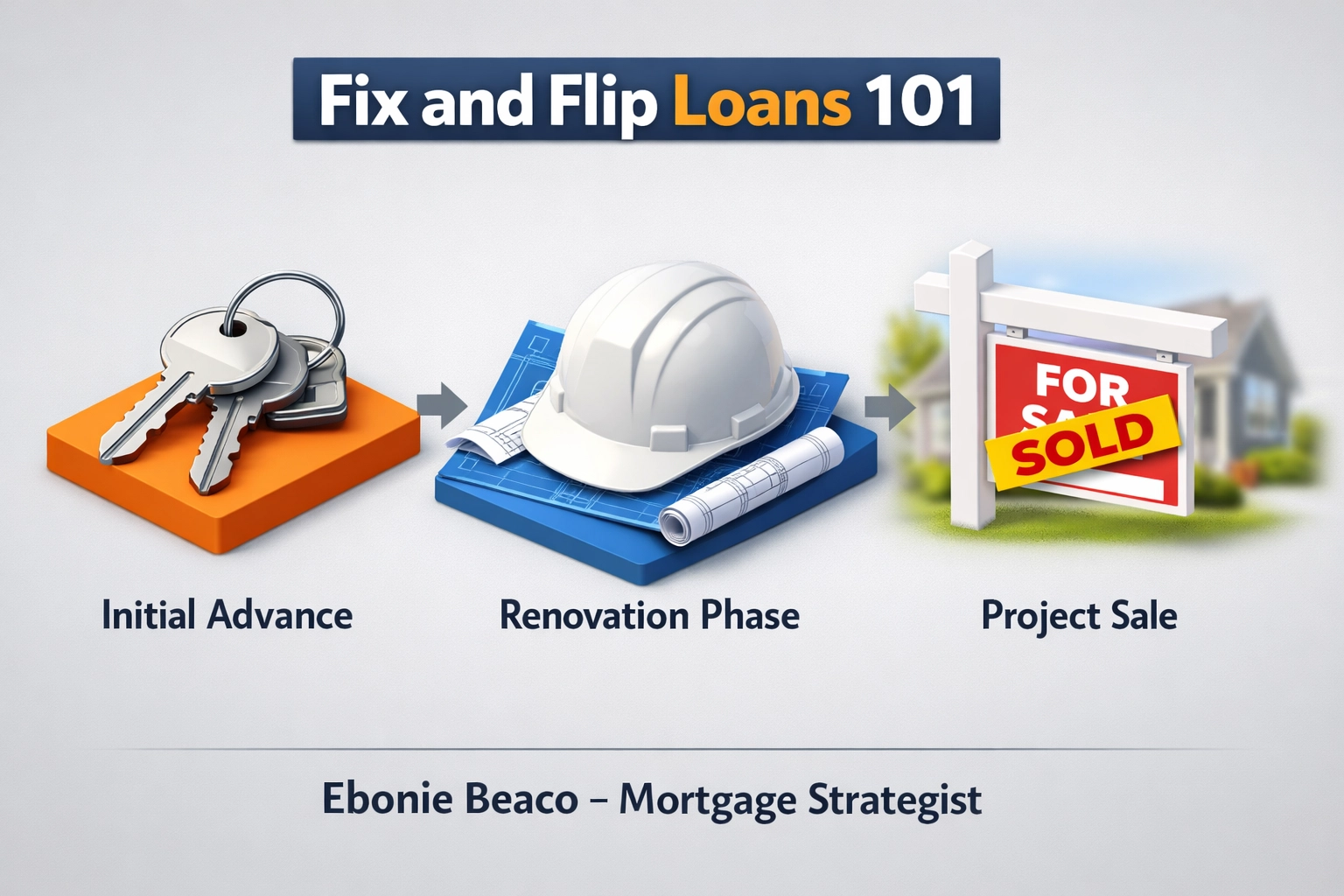

Image Description: An infographic titled 'Fix and Flip Loans 101' showing a 3-step timeline: 1. Initial Advance (80-90% of Purchase), 2. Renovation Phase (Draw Schedule), 3. Project Sale (Loan Repayment). No money or cash icons are present. At the bottom, it reads: Ebonie Beaco - Mortgage Loan Officer.

Image Description: An infographic titled 'Fix and Flip Loans 101' showing a 3-step timeline: 1. Initial Advance (80-90% of Purchase), 2. Renovation Phase (Draw Schedule), 3. Project Sale (Loan Repayment). No money or cash icons are present. At the bottom, it reads: Ebonie Beaco - Mortgage Loan Officer.

Is Fix and Flip Financing Right for You?

This strategy is built for those who have a clear exit plan. It is ideal for:

- Experienced flippers who want to keep their own cash liquid for other deals.

- New investors who have a solid contractor team but need the capital to get started.

- Landlords who want to use the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat).

If you are a homeowner looking to access equity for a different type of project, a home refinance might be a better fit. However, if your goal is to build a portfolio of renovated homes in Georgia or Michigan, fix and flip loans are the most powerful tool in your belt.

Transparency in Lending

At Home Loans Network, we believe in a transparent approach. We want you to understand the costs: including origination fees and interest rates: before you sign. Real estate investing is a numbers game, and if the numbers don't work for you, they don't work for us.

Explore our testimonials to see how other investors have utilized our strategies to grow their portfolios across Alabama, Florida, and beyond.

Whether you are looking for your first flip in Chicago or scaling a 10-house-a-year operation in Atlanta, having a mortgage strategist who understands the "investor mindset" is crucial. We don't just provide the capital; we provide the roadmap.

Explore your funding options or seek professional mentoring for your next project.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664