Finding a Mortgage Lender for Out-of-State Investing

Investing in real estate beyond your backyard is a strategic way to diversify your portfolio and tap into markets with higher yields. Whether you live in a high-cost area like Los Angeles or Chicago and want to buy rental property in Alabama or Indiana, the logistics of financing change when you cross state lines.

Finding the right lender is the most critical step in this journey. You need a partner who understands the local nuances of the market where the property is located while being able to work with you remotely.

The Landscape of Out-of-State Lending

When you look for a mortgage lender for out-of-state properties, you generally have three paths: national banks, local community banks, and specialized investor-focused lenders.

National Banks Large financial institutions operate in almost every state. They offer a sense of familiarity and often have streamlined online portals. Pros: Standardized processes and competitive rates for traditional homeowners. Cons: Rigid credit requirements and a lack of personalized service for complex investment scenarios.

Local Community Banks These are small banks located in the specific city where you are buying. Pros: Deep knowledge of the local street-by-street market. Cons: They often require you to have a physical presence or an existing relationship in the area.

Specialized Investor Lenders These lenders focus specifically on real estate professionals and landlords. They offer products like DSCR loans and fix-and-flip lines of credit. Pros: Flexible underwriting based on the property’s income rather than your personal paystubs. Cons: Interest rates may be slightly higher than a primary residence loan.

Explore the loan process to see how these different paths diverge during underwriting.

Why DSCR Loans are the Gold Standard for Out-of-State Investors

For many investors buying in Florida, Georgia, or Michigan from a distance, the Debt Service Coverage Ratio (DSCR) loan is the preferred tool.

DSCR (Debt Service Coverage Ratio) A mortgage format where qualification is based on the property’s rental income rather than the borrower’s personal income. Practical Benefit: You do not need to provide tax returns or W2s, making it ideal for self-employed investors or those with multiple properties.

When you use a DSCR loan, the lender looks at whether the monthly rent covers the mortgage payment (Principal, Interest, Taxes, Insurance, and Association fees). If the ratio is 1.0 or higher, the deal is often viable. This is especially helpful for out-of-state investing because it removes the hurdle of explaining your local employment to a distant underwriter.

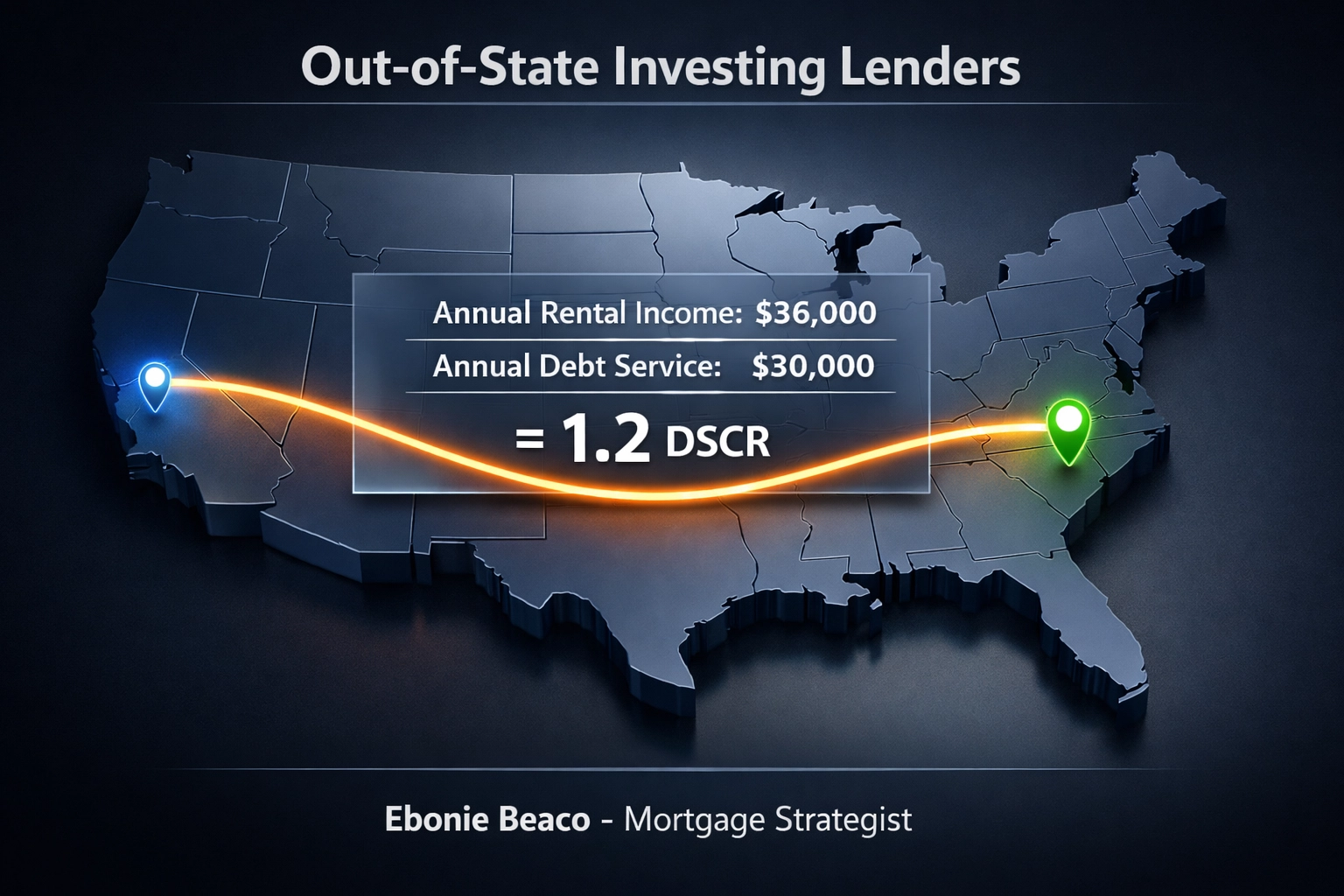

Visual: Out-of-State Investing Lenders. A professional chart showing a DSCR calculation: Annual Rental Income ($36,000) / Annual Debt Service ($30,000) = 1.2 DSCR. Property located in Birmingham, AL; Investor located in San Francisco, CA. Ebonie Beaco - Mortgage Loan Officer.

Visual: Out-of-State Investing Lenders. A professional chart showing a DSCR calculation: Annual Rental Income ($36,000) / Annual Debt Service ($30,000) = 1.2 DSCR. Property located in Birmingham, AL; Investor located in San Francisco, CA. Ebonie Beaco - Mortgage Loan Officer.

Comparing National Lenders vs. Specialized Brokers

National mortgage lenders are the primary option for straightforward out-of-state financing because they operate in both your location and the investment market area. This gives them an understanding of both ends of the transaction. This approach is particularly suitable if you are a first-time out-of-state investor seeking a simplified process.

However, the trade-off is often a "cookie-cutter" approach. If your situation is even slightly unique: perhaps you are a wholesaler looking to transition into buy-and-hold, or you are using the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat): a national bank might decline your application.

Specialized lenders and mortgage brokers who focus on home purchase strategies for investors can access "Non-QM" (Non-Qualified Mortgage) products. These products are designed for the complexities of cross-state investing, including understanding different landlord-tenant laws and market-specific factors in states like Virginia or Missouri.

Hard Money and Bridge Loans for Faster Acquisitions

Sometimes, the market moves too fast for a traditional 30-day close. In competitive hubs like Tampa or Atlanta, you might need to close in two weeks.

Hard Money Loans Short-term financing secured by real estate, typically issued by private investors or companies. Practical Benefit: Approval is based on the property value and "After Repair Value" (ARV) rather than your personal credit score.

Bridge Loans A temporary loan used until an investor secures permanent financing or removes an existing obligation. Practical Benefit: It "bridges" the gap between buying a distressed property out-of-state and getting it ready for a long-term rental loan.

Hard money and bridge loans are excellent for the "Fix and Flip" crowd. If you find a distressed multi-unit building in Chicago, you can use a bridge loan to acquire and renovate it, then perform a cash-out refinance once the units are leased and the value has increased.

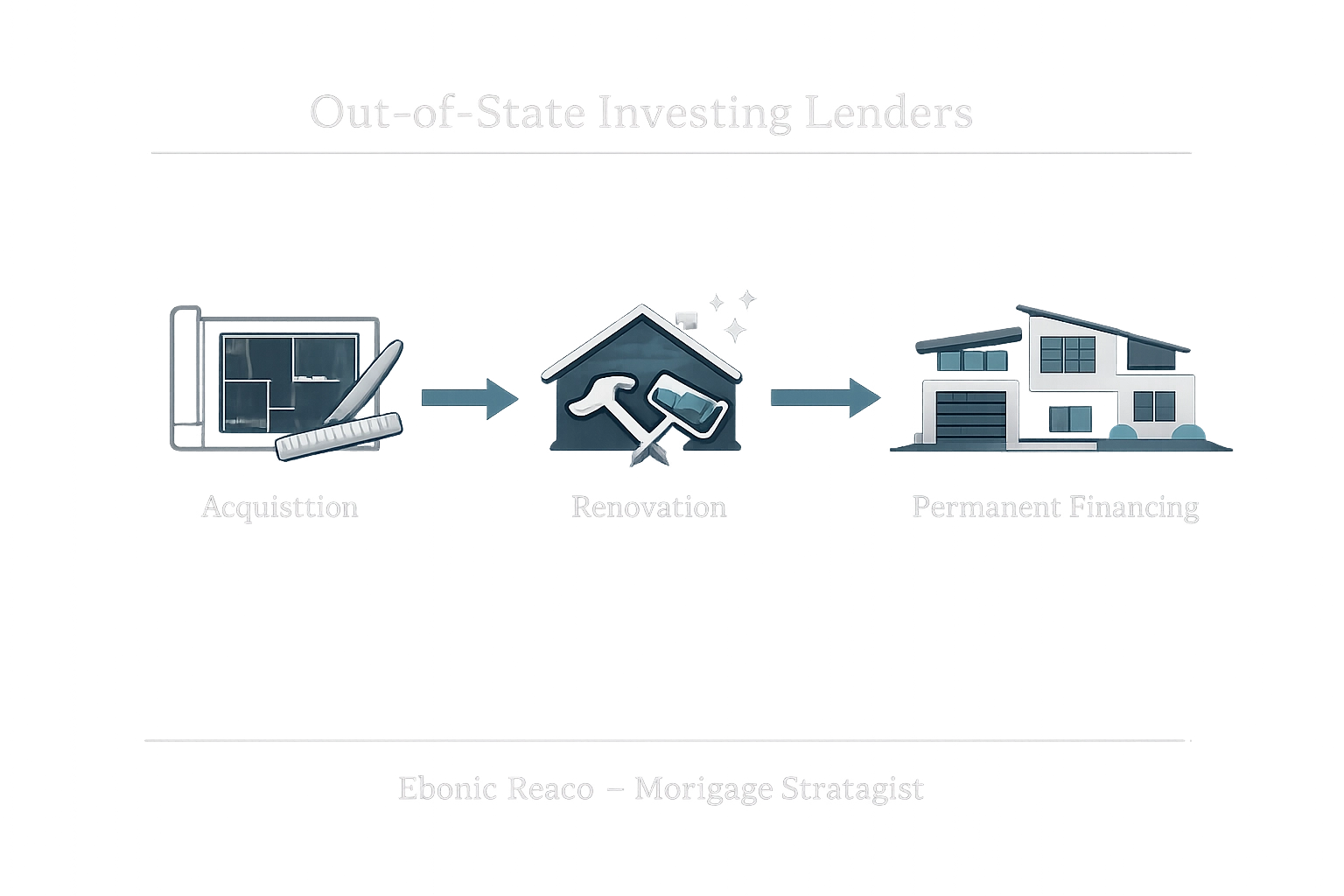

Visual: Out-of-State Investing Lenders. A flow chart showing the Bridge-to-Permanent financing path. Step 1: Acquisition with Bridge Loan. Step 2: Renovation. Step 3: Refinance to Long-Term DSCR Loan. Ebonie Beaco - Mortgage Loan Officer.

Visual: Out-of-State Investing Lenders. A flow chart showing the Bridge-to-Permanent financing path. Step 1: Acquisition with Bridge Loan. Step 2: Renovation. Step 3: Refinance to Long-Term DSCR Loan. Ebonie Beaco - Mortgage Loan Officer.

Key Questions to Ask Your Out-of-State Lender

Before you sign an intent to proceed, you must vet your lender. Use these questions to ensure they can handle a long-distance transaction:

- Do you lend in the specific state where the property is located? Not all lenders are licensed in every state. Ensure they have active licenses in Alabama, Arkansas, California, or whichever state you are targeting.

- What is your experience with Non-QM and DSCR products? If they only do FHA and VA loans, they might not be the best fit for an investment portfolio.

- How do you handle appraisals in rural or distant markets? Reliable valuations are the heartbeat of an out-of-state deal.

- Can you provide a pre-approval letter that is respected by local listing agents? In markets like Virginia, a strong pre-approval letter can be the difference between a winning bid and a rejected one.

You can find more answers to common hurdles in the FAQ section.

Utilizing Technology and Remote Closing

Technology has removed the friction from out-of-state investing. Most modern lenders use digital portals for document uploads and "E-closings" or mobile notaries.

Mobile Notary A public official who travels to your location to witness the signing of mortgage documents. Practical Benefit: You can buy a house in Florida while sitting in your home office in Michigan.

When choosing a lender, ask about their digital capabilities. If they require you to mail physical checks or fly in for the closing, they are likely not set up for the modern out-of-state investor.

Diversifying Across State Lines

Why are investors looking at other states? Often, it is about the "Price-to-Rent" ratio. In many California cities, the cost of entry is so high that the monthly rent doesn't cover the mortgage. By looking at markets in the Midwest or the South, investors can find properties that provide immediate monthly cash flow.

If you already have equity in a primary residence, you might consider a HELOC or cash-out refinance to fund the down payment on your out-of-state investment. This allows you to use your existing home’s value to build a portfolio elsewhere.

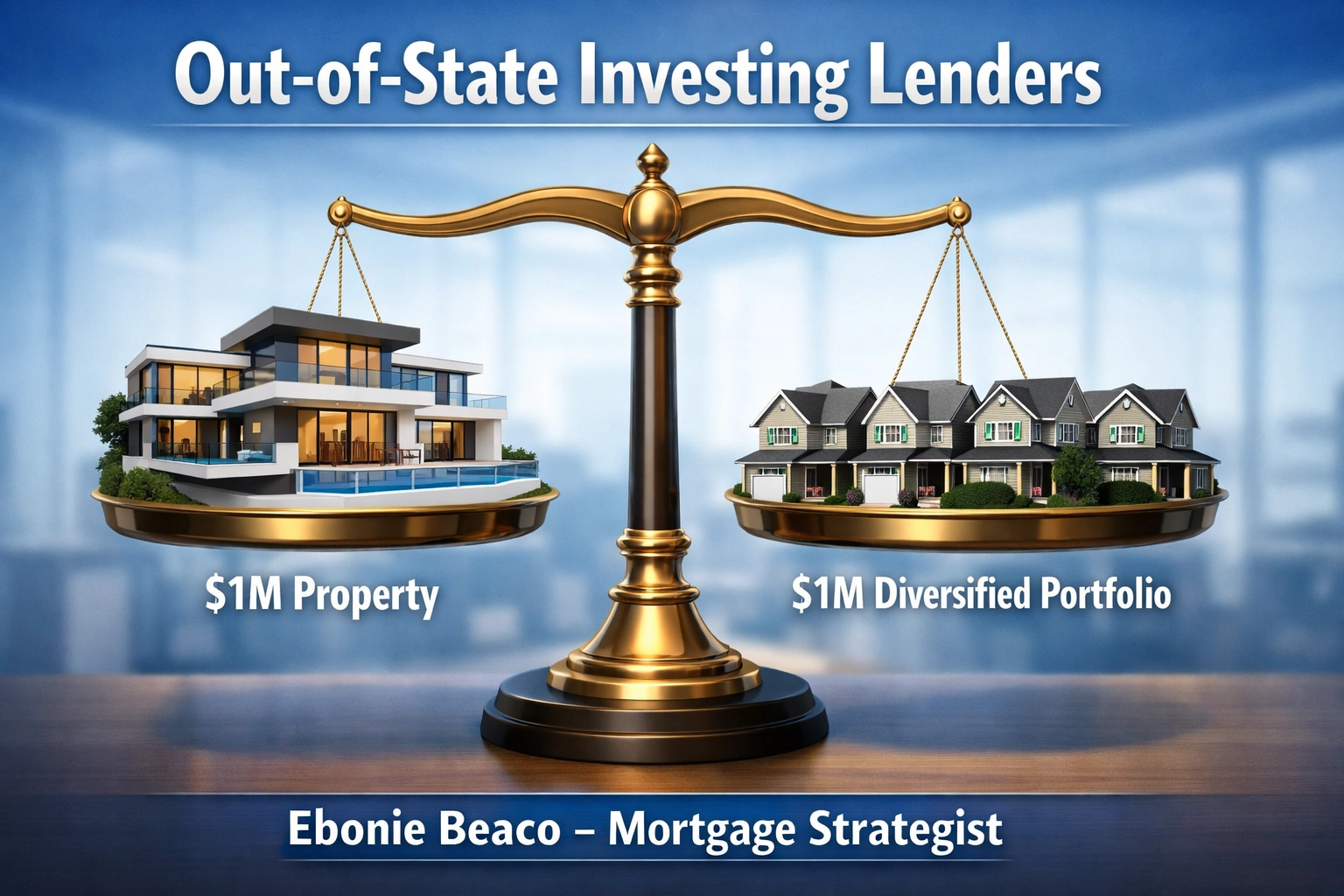

Visual: Out-of-State Investing Lenders. A comparison table showing a $1M property in CA with $4k rent vs. four $250k properties in IN with $2k rent each ($8k total). Ebonie Beaco - Mortgage Loan Officer.

Visual: Out-of-State Investing Lenders. A comparison table showing a $1M property in CA with $4k rent vs. four $250k properties in IN with $2k rent each ($8k total). Ebonie Beaco - Mortgage Loan Officer.

Final Steps to Securing Your Loan

Out-of-state investing is a team sport. Your lender is the most important player on that team, alongside your property manager and real estate agent. By focusing on specialized investor loans like DSCR or bank statement programs, you can overcome the traditional barriers of distance and strict bank guidelines.

Jump in and use mortgage calculators to run the numbers on your potential deals. Comparing loan terms, interest rates, and fees across different lenders is essential to finding the best fit for your investment strategy.

If you are ready to expand your portfolio or need a strategist to walk you through the nuances of financing properties across the country, reaching out for expert guidance is the next logical step.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664