Financing Real Estate in a Trust: What You Need to Know

Understanding how to hold and finance property is a major step in building a long-term wealth strategy. Whether you are a homeowner in Michigan or a seasoned real estate investor in Florida, placing your assets in a trust is a common move for privacy and estate planning.

However, many people worry that moving a home into a trust will complicate their ability to get a mortgage or refinance. The good news is that financing real estate in a trust is entirely possible, provided you understand the mechanics of how lenders view these entities.

Explore the essential steps for navigating trust financing and how to keep your investment strategy moving forward without hitting unnecessary roadblocks.

Defining the Trust in Real Estate Finance

Trust: A fiduciary arrangement where a third party, known as a trustee, holds and manages assets on behalf of a beneficiary. In a real estate context, the trust becomes the legal owner of the property, while you typically retain control as the trustee or beneficiary.

Revocable Living Trust: A trust created during your lifetime that can be altered or canceled at any time. Most residential mortgage lenders prefer this structure because it allows the borrower to maintain full control over the asset.

Irrevocable Trust: A trust that cannot be easily modified or terminated once it is created. Financing property within an irrevocable trust is more complex and often requires specialized commercial or non-QM lending solutions.

Accessing the right loan product depends heavily on which type of trust you choose to implement. Most conventional lenders are comfortable with revocable trusts, but if you are working with more complex structures, you might need to look toward mortgage basics that accommodate unique title holdings.

Transferring Real Estate Into a Trust

The process of moving property into a trust is known as "funding" the trust. If you sign a trust agreement but never change the title of your home, the trust does not actually control the asset.

Quitclaim Deed: A legal document used to transfer interest in real property from one entity to another without making guarantees about the title's history. You will typically use a Quitclaim Deed to move the property from your individual name into the name of the trust.

Recording: The act of filing the deed with the County Recorder’s office to make the transfer a matter of public record. Recording is a critical step because it officially notifies the local government and future lenders that the trust holds the title.

You should prioritize transferring your most valuable assets first. While the process is not overly difficult, it requires precision to ensure the legal names match your trust documents exactly. You can find more details on how this fits into the broader timeline of buying or refinancing on our loan process page.

Visualizing the Transfer: A flowchart showing the movement of title from an Individual Name to a Revocable Living Trust via a Quitclaim Deed, including the recording step at the County Recorder.

Visualizing the Transfer: A flowchart showing the movement of title from an Individual Name to a Revocable Living Trust via a Quitclaim Deed, including the recording step at the County Recorder.

Navigating the Due-on-Sale Clause

A common concern for homeowners in places like California or Virginia is the "due-on-sale" clause found in most mortgage contracts. This clause technically allows a lender to demand full repayment of the loan if the property is transferred to a new owner.

However, federal law: specifically the Garn-St. Germain Depository Institutions Act: provides protections for residential properties with fewer than five units. If you are moving your primary residence into a revocable living trust where you remain the beneficiary, lenders generally cannot trigger the due-on-sale clause.

Due-on-Sale Clause: A mortgage contract provision that requires the borrower to pay off the full loan balance upon the sale or transfer of the property. This clause is designed to prevent borrowers from transferring low-interest loans to new buyers, but it usually does not apply to standard estate planning transfers.

Before you record that deed, it is a smart move to notify your lender in writing. While they likely won't block the transfer, transparency helps prevent administrative hiccups down the road. If you have questions about how your specific loan might react, check out our FAQ section for more common scenarios.

Financing Options for Trust-Held Properties

If the property is already in a trust and you want to pull equity out or purchase a new investment property, you have several paths to explore.

DSCR Loans for Trust Assets

For real estate investors building portfolios in Chicago or Atlanta, DSCR Investor Loans are an excellent fit for trusts. Because Debt Service Coverage Ratio loans focus on the property’s income rather than your personal income, lenders are often more flexible with the title being held in a trust or an LLC.

HELOCs and Home Equity Loans

Homeowners looking to access equity while keeping their property in a trust can still utilize a HELOC. Many lenders in our network allow for trusts to be the primary title holder, though they will review the trust documents to ensure the trustee has the legal authority to encumber the property with debt.

Cash-Out Refinance

A Cash-Out Refinance allows you to replace your existing mortgage with a new one for a larger amount, taking the difference in cash. This is a powerful tool for BRRRR investors (Buy, Rehab, Rent, Refinance, Repeat) who want to keep their assets protected within a trust structure while continuing to scale. Learn more about your options on our home refinance page.

Strategy Breakdown: A visual comparison of a standard mortgage vs. a DSCR loan when held in a trust, highlighting that the trust is the "Owner" and the individual is the "Guarantor".

Strategy Breakdown: A visual comparison of a standard mortgage vs. a DSCR loan when held in a trust, highlighting that the trust is the "Owner" and the individual is the "Guarantor".

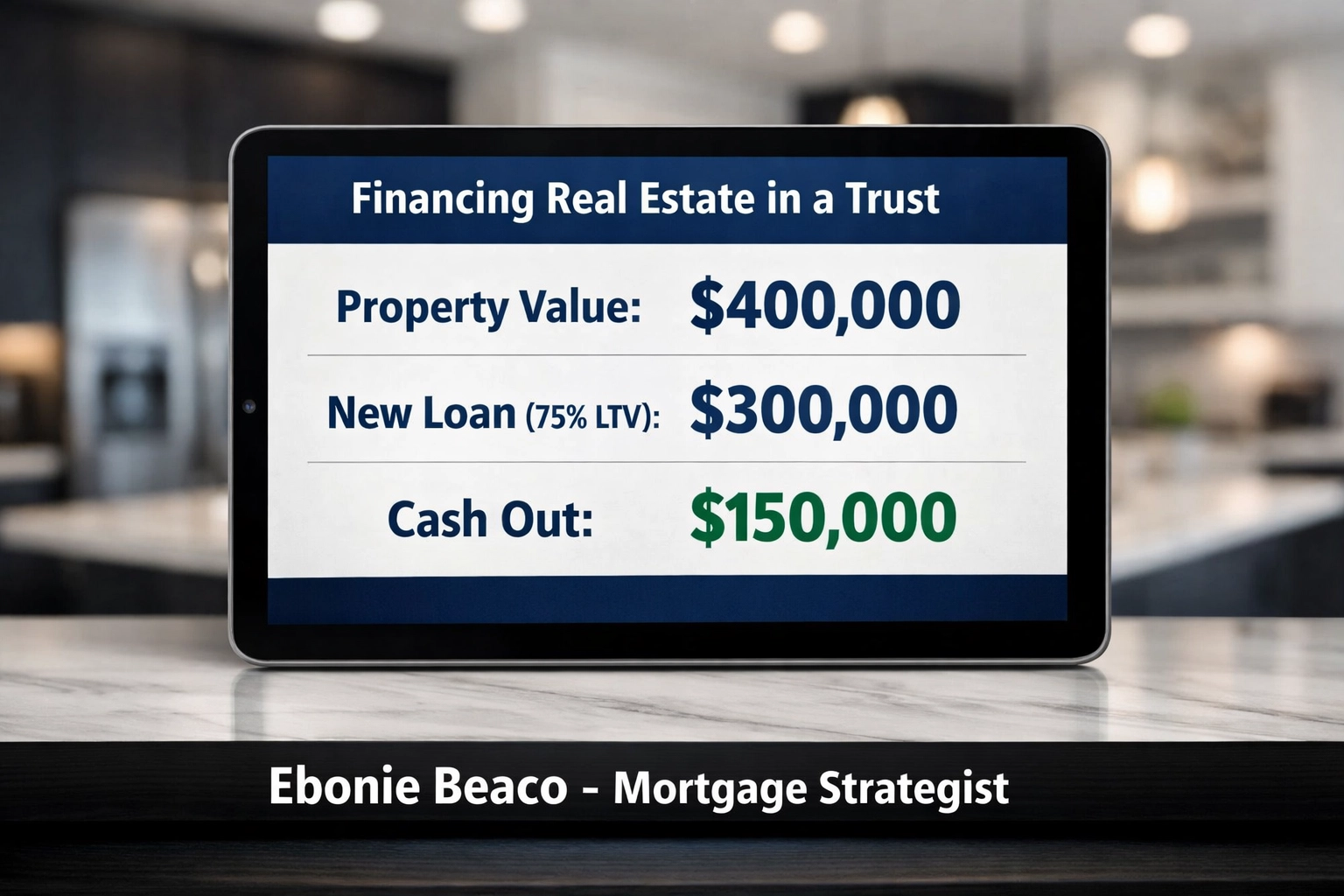

Practical Financial Example: Refinancing in a Trust

Let’s look at a real-world scenario. Imagine you own a rental property in Michigan held within a revocable living trust. The property is currently valued at $400,000, and you owe $150,000 on the original mortgage. You want to use the equity to fund a renovation on another property.

Calculation Example:

- Property Value: $400,000

- Existing Mortgage: $150,000

- Max Loan-to-Value (LTV): 75%

- New Total Loan Amount: $300,000

- Existing Debt Payoff: -$150,000

- Gross Cash to Trust: $150,000 (before closing costs)

In this case, the trustee (you) would sign the loan documents on behalf of the trust. The lender will require a "Certificate of Trust," which is a shortened version of your trust document that proves you have the power to take out a loan against the property.

Financial Analysis: Title 'Financing Real Estate in a Trust' showing: Property Value $400,000 | New Loan (75% LTV) $300,000 | Cash Out $150,000. Ebonie Beaco - Mortgage Loan Officer at the bottom.

Financial Analysis: Title 'Financing Real Estate in a Trust' showing: Property Value $400,000 | New Loan (75% LTV) $300,000 | Cash Out $150,000. Ebonie Beaco - Mortgage Loan Officer at the bottom.

Why Real Estate Investors Use Trusts

Investors in high-activity markets like Alabama or Georgia often use trusts for reasons that go beyond simple probate avoidance.

- Privacy: In many jurisdictions, the name of the trust appears on public records rather than your personal name. This adds a layer of anonymity for high-net-worth individuals or those with large portfolios.

- Succession Planning: If an investor passes away, properties held in a trust can be managed or sold by a successor trustee immediately, avoiding the lengthy and expensive probate court process.

- Asset Consolidation: Trusts allow an investor to group multiple properties under one umbrella, making it easier to manage the overall estate.

If you are a landlord or a fix-and-flip investor, using a trust in conjunction with Non-QM Mortgage Loans can give you the flexibility you need to grow. You can book an appointment to discuss how to structure your next deal within a trust.

Maintenance and Trustee Responsibilities

When a trust holds real estate, the trustee is responsible for the ongoing costs of the property. This includes taxes, insurance, and repairs.

Liquidate: The process of selling an asset to convert it into cash. If the trust does not have enough liquid cash to pay for a major repair (like a new roof on a Chicago multi-family building), the trustee may need to liquidate other trust assets or seek a new loan.

Encumber: To place a claim or lien against a property, such as a mortgage. The trust documents must explicitly grant the trustee the power to encumber the property. If this language is missing, you may need to amend the trust before a lender will approve your financing.

It is always a good idea to review your trust documents with a legal professional and your mortgage strategist simultaneously. This ensures that your estate planning goals and your financing goals are in total alignment.

Jump In and Secure Your Legacy

Financing real estate in a trust is a sophisticated move that protects your future while allowing you to leverage your assets today. Whether you are looking at Airbnb and Short-Term Rental Financing or simply want to move your family home into a living trust, the right guidance makes the process seamless.

Compare your options and see how different loan programs can work with your trust structure. From Bank Statement Loans for self-employed investors to traditional Home Purchase loans, there is a path forward for every scenario.

If you are ready to explore trust financing or need a mentor to help you structure your real estate portfolio, reach out for a strategy session.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

For more information on our commitment to service, feel free to review our accessibility statement or see what others are saying on our testimonials page. If you are ready to get started, you can access our online forms right now.