Entity-Based Lending (LLC / Corp Loans)

If you are serious about building a real estate empire, you eventually have to stop signing for houses in your own name. Entity-based lending is the shift from "individual buyer" to "business owner." By closing loans in an LLC or Corporation, you unlock levels of liability protection and privacy that personal mortgages simply cannot offer. Whether you are flipping a bungalow in Chicago or holding a short-term rental in Florida, using an entity keeps your personal life and your business life in two different boxes. This strategy is essential for scaling a portfolio without hitting the personal debt-to-income walls that stop most people. It is about professionalizing your approach and treating every property like the business it truly is.

Explore your options and secure your next deal by closing in your business name.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

Scaling Your Portfolio with Entity-Based Loans

When you first start investing in real estate, buying a property in your own name feels natural. You use your personal credit, your personal bank statements, and you sign the closing papers as an individual. But as you grow from one rental to five, ten, or twenty, the risks change. Closing in your personal name puts your personal assets at risk if something goes sideways at a rental property.

Entity-Based Lending is a financing strategy where the mortgage is issued to a legal entity like an LLC, S-Corp, or C-Corp. This structure provides a layer of separation between your personal finances and your real estate investments.

In markets like Chicago, Virginia, and throughout Florida, savvy investors use this method to keep their personal debt-to-income (DTI) ratios clean. Because the loan belongs to the entity, it often does not appear on your personal credit report. This allows you to keep buying without the "too many loans" red flag from traditional banks.

Technical Definitions for the Modern Investor

Business Entity: A legal structure formed to conduct business, such as an LLC or Corporation. Closing under an entity limits your personal liability regarding the property's debts and legal obligations.

Non-Recourse Debt: A type of loan where the lender's only protection in case of default is the collateral (the property). While many entity loans require a personal guarantee, some specialized commercial programs offer non-recourse options for high-equity deals.

Personal Guarantee: A commitment by the individual owner of the entity to be responsible for the debt if the business cannot pay. Most entity-based loans for residential rentals still require this to ensure the borrower stays committed to the project.

Why Use an LLC or Corp for Your Mortgage?

The decision to move away from personal name financing is a milestone in an investor's career. It signals that you are moving from a hobbyist to a professional.

Jump in and look at the primary advantages of this lending structure:

- Asset Protection: If a tenant sues the property owner, they are suing the LLC, not you personally. This shields your personal home, savings, and other assets from the lawsuit.

- Privacy: When you buy in an LLC, your name does not appear in public property records. This is a common strategy for high-net-worth individuals and those who value discretion.

- Portfolio Scaling: Many traditional lenders limit you to 10 personal mortgages. Entity-based lending through Home Loans Network allows you to bypass these caps and grow your portfolio indefinitely.

- Partnership Flexibility: If you are buying a property with a partner, an LLC provides a clear framework for ownership percentages and management duties that a personal mortgage cannot handle easily.

The Role of DSCR in Entity Lending

Most entity-based loans are also DSCR Investor Loans. Because an LLC does not have "employment income" like a human does, lenders look at the income of the property itself.

Debt Service Coverage Ratio (DSCR): A calculation that compares the monthly rental income of a property to its monthly debt obligations. If the rent covers the mortgage, taxes, insurance, and HOA fees, the entity qualifies for the loan.

This is a game-changer for self-employed borrowers who might have plenty of cash but show low income on their tax returns due to business write-offs. We focus on the deal, not your tax returns. You can learn more about how we evaluate these deals on our FAQ page.

Visual: A chart showing a 4-unit property deal breakdown. Property Value: $600,000. Loan Amount: $450,000 (75% LTV). Monthly Rental Income: $6,500. Monthly PITIA: $4,800. DSCR: 1.35. Footer: Ebonie Beaco - Mortgage Strategist.

How to Qualify for an Entity-Based Loan

The process is more straightforward than a traditional "big bank" mortgage. Since we are not looking at your pay stubs or W2s, the documentation focuses on the property and the legal standing of your entity.

Explore the typical requirements for closing in an LLC name:

- Articles of Organization: The legal document filed with the state to create your LLC.

- Operating Agreement: A document outlining how the entity is managed and who has the authority to sign for loans.

- EIN (Employer Identification Number): The "Social Security Number" for your business, issued by the IRS.

- Certificate of Good Standing: A document from the state confirming your entity is active and has paid its fees.

- Credit Score: While we don't use your DTI, your personal credit score is still used to determine the interest rate and down payment requirement.

Access our loan process guide to see how we move from application to closing efficiently.

Entity Lending in Major Markets

We see massive activity for entity-based lending in specific regions where the rental market is booming.

In Chicago, investors use LLCs to manage multi-unit properties (2-4 units) while protecting their primary residences. The city’s complex landlord-tenant laws make the liability protection of an LLC even more vital.

Throughout Florida and California, high-value short-term rentals (Airbnb/VRBO) are almost exclusively financed through entities. This allows investors to manage these properties as independent business units.

In Virginia and Georgia, we help many BRRRR (Buy, Rehab, Rent, Refinance, Repeat) investors transition from hard money bridge loans into long-term entity-based financing once the renovation is complete.

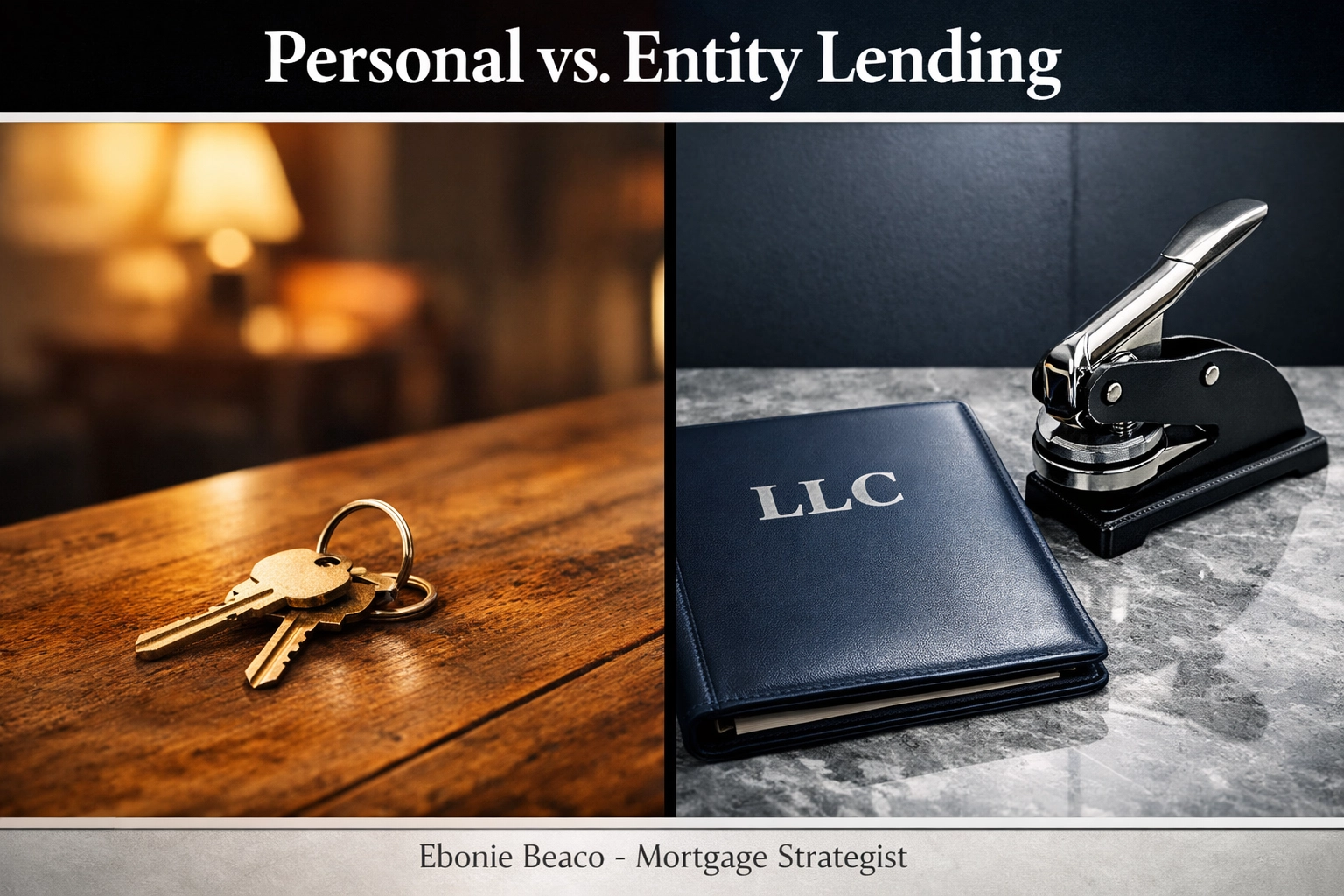

Comparing Personal vs. Entity Lending

| Feature | Personal Name Loan | Entity-Based Loan (LLC) |

|---|---|---|

| Liability | Personal assets are exposed | Limited to entity assets |

| Income Verification | W2s, Pay stubs, Tax returns | Property rental income (DSCR) |

| Privacy | Name on public record | Entity name on public record |

| Reporting | Appears on personal credit | Usually does not appear on credit |

| Loan Limits | Subject to agency caps (Fannie/Freddie) | No hard limit on number of loans |

Visual: A comparison table showing the differences between Personal Name Loans and Entity-Based Loans. Title: Personal vs. Entity Lending. Footer: Ebonie Beaco - Mortgage Strategist.

Strategic Advantages for Self-Employed Borrowers

If you run your own business, you know the struggle of trying to get a mortgage. You make great money, but your accountant is excellent at finding deductions. On paper, it looks like you barely make enough to cover groceries.

Entity-based lending solves this. By using the property’s cash flow to qualify, your "paper income" is no longer a hurdle. We offer specialized Bank Statement Loans and P&L Loans for those who prefer to keep their investments in their own name, but for most professional landlords, the LLC path is the cleanest.

Compare these options by using our mortgage calculators to see how the numbers shift based on your entity structure.

Closing the Deal: What to Expect

When you are ready to move forward, the "select loan officer" phase is crucial. You need someone who understands the nuances of corporate resolutions and operating agreements.

At Home Loans Network, we guide you through the transition. We ensure your entity is structured correctly to meet lender requirements so there are no surprises at the closing table.

Compare the speed of an entity loan to a traditional one. Without the need for a manual underwrite of your entire personal financial history, these deals can often close faster, frequently in 21 to 30 days.

Common Questions About LLC Loans

Can I transfer my current property into an LLC?

Yes, this is a common strategy. However, most traditional mortgages have a "due on sale" clause that could be triggered by a transfer. Refinancing into an entity-based loan is often the safer way to move title while maintaining a compliant mortgage.

Do I need a separate bank account for the LLC?

Absolutely. To maintain the "corporate veil" and protect your personal assets, the LLC must operate as a separate financial unit. This means rent goes into an LLC account and the mortgage is paid from that same account.

Does the LLC need to be "old"?

No. Many of our programs allow for "newly formed" entities. You can literally create the LLC on Monday and apply for the loan on Tuesday, provided the rest of the deal makes sense.

Take the Next Step in Your Investment Journey

The transition to entity-based lending is one of the most significant steps you can take to protect your future. It moves the burden of the debt from your shoulders to the property itself.

Whether you are looking at a fix-and-flip in Michigan or a portfolio of rentals in Alabama, the structure of your loan is vital to your long-term success.

Schedule a 1 on 1 to discuss your entity structure and loan scenario.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664