DTI Decoded: How Much Debt Can You Really Have for a Mortgage?

When you step into the world of real estate financing, whether you are buying your first home in Chicago or expanding a rental portfolio in Florida, one acronym will follow you everywhere: DTI.

Debt-to-Income (DTI) represents the primary tool lenders use to gauge your ability to manage monthly payments and repay borrowed money. It is a simple mathematical comparison, but it carries immense weight in the mortgage approval process.

Understanding how this number works allows you to position yourself as a low-risk borrower. This transparency ensures you aren't surprised by a loan denial after you have already found the perfect property.

Defining the Core Components

Before jumping into the math, let’s establish clear definitions for the elements that create your DTI profile.

Gross Monthly Income: Your total earnings before taxes or other deductions are removed. This serves as the baseline for your borrowing capacity.

Recurring Monthly Debt: The minimum monthly payments for liabilities like auto loans, student loans, credit cards, and personal loans. This does not include utilities or groceries.

Front-End Ratio: The percentage of your gross monthly income that goes toward housing expenses specifically, including principal, interest, taxes, and insurance (PITI).

Back-End Ratio: The percentage of your gross monthly income used to cover all recurring monthly debts plus your new proposed mortgage payment.

You can explore more foundational terms in our mortgage basics section to prepare for your application.

The DTI Calculation: How the Math Works

Calculating your DTI is straightforward. Lenders take your total monthly debt payments and divide them by your gross monthly income.

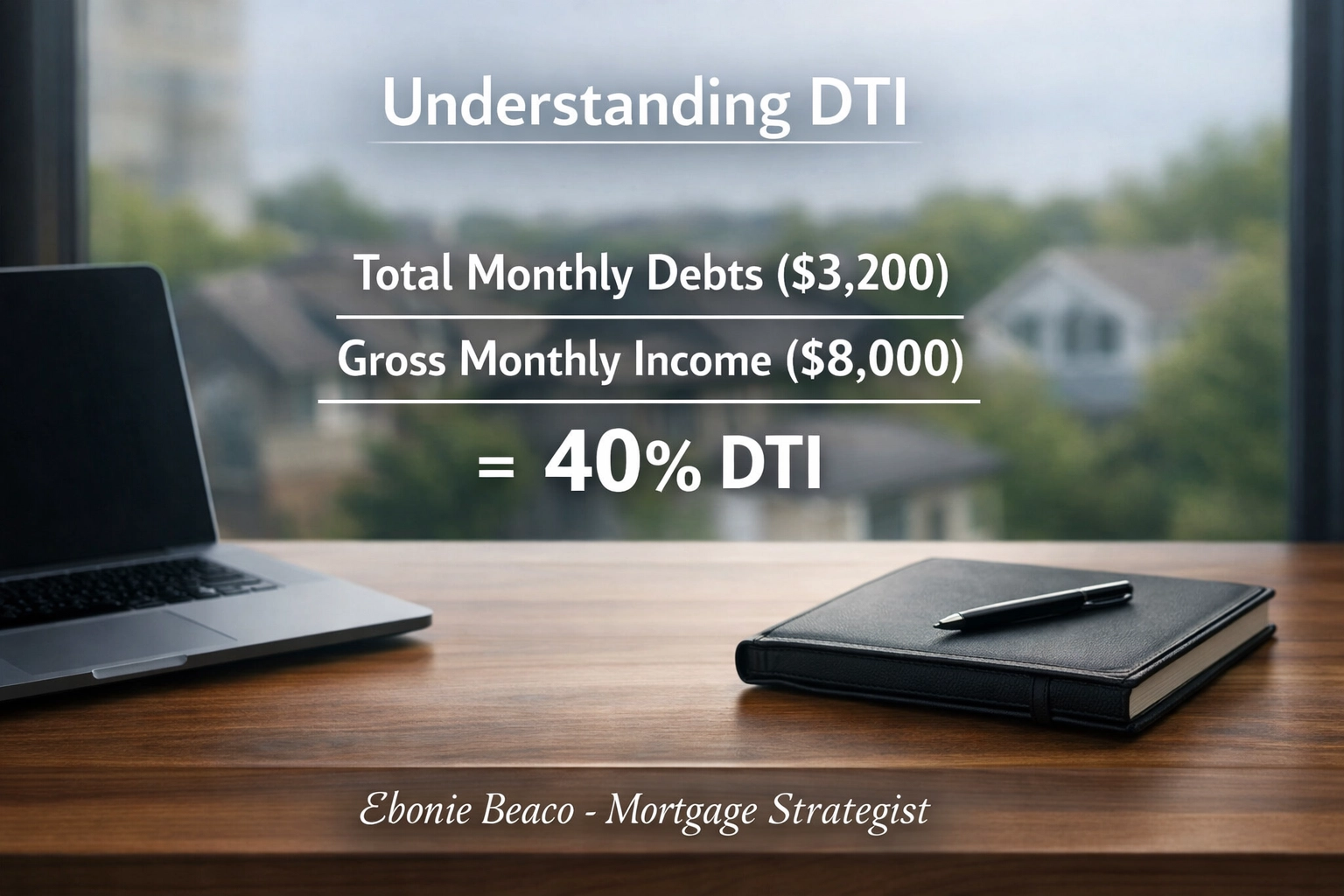

For example, if you earn $8,000 per month before taxes and your total monthly debt obligations (including your future mortgage) equal $3,200, your DTI is 40%.

The Formula: (Total Monthly Debts / Gross Monthly Income) x 100 = DTI %

Lenders use this percentage to determine if you have enough "breathing room" in your budget to handle a mortgage payment reliably. If your ratio is too high, it suggests that any minor financial hiccup could lead to a missed payment.

Image Description: A professional financial graphic titled "Understanding DTI". It displays the calculation: (Total Debts / Gross Income). It shows a clean breakdown: Total Monthly Debts ($3,200) divided by Gross Monthly Income ($8,000) equals 40% DTI. The text at the bottom reads "Ebonie Beaco - Mortgage Loan Officer". No currency notes or coins are visible.

Image Description: A professional financial graphic titled "Understanding DTI". It displays the calculation: (Total Debts / Gross Income). It shows a clean breakdown: Total Monthly Debts ($3,200) divided by Gross Monthly Income ($8,000) equals 40% DTI. The text at the bottom reads "Ebonie Beaco - Mortgage Loan Officer". No currency notes or coins are visible.

Standard DTI Thresholds by Loan Type

Different mortgage programs have different appetites for debt. While a 36% back-end ratio is often cited as the "gold standard," many programs allow for much higher limits depending on your credit score and down payment.

- Conventional Loans: Typically look for a DTI of 36% or lower, but can go up to 45% or even 50% with high credit scores and significant cash reserves.

- FHA Loans: These are often more flexible, allowing ratios up to 43% naturally, and sometimes as high as 56.9% with "compensating factors" like a high credit score or a large amount of savings.

- VA Loans: Technically, the VA prefers a 41% DTI, but they are famously flexible and often approve much higher ratios if the borrower has sufficient "residual income."

- USDA Loans: Generally capped at 41%, though exceptions exist for those with strong credit profiles.

If you are curious about which path fits your current numbers, you can review our FAQ for more specifics on program requirements.

DTI for Real Estate Investors

For the landlord or investor looking to scale a portfolio in markets like Georgia or Virginia, DTI can sometimes become a hurdle. Traditional lenders count the full debt of your existing properties against you, which can quickly max out your DTI limits.

This is where specialized financing like DSCR Investor Loans (Debt Service Coverage Ratio) becomes a game-changer. Unlike traditional mortgages, DSCR loans do not use your personal DTI to qualify you.

Instead, they focus on the income generated by the property itself. If the rental income covers the mortgage payment (the "debt service"), the loan is viable. This allows investors to continue growing even when their personal DTI would technically be too high for a standard bank loan.

For those pursuing the BRRRR strategy or managing multiple short-term rentals, understanding this pivot from personal DTI to property-based income is essential for long-term growth.

How to Improve Your DTI Before Applying

If your ratio is currently sitting in the "danger zone" (above 45% for most standard programs), there are several strategies to bring it down.

Reduce High-Interest Revolving Debt: Focus on paying down credit card balances. Since lenders use the minimum monthly payment in their calculation, reducing a balance to zero removes that entire payment from your DTI.

Avoid New Large Purchases: Do not finance a new car or take out a large personal loan right before or during your mortgage application process. This will immediately spike your DTI and could kill your deal.

Increase Your Documentable Income: If you have a side hustle or seasonal income, ensure it is documented on your tax returns so it can be factored into your gross monthly income calculation.

Extend Loan Terms: Sometimes, refinancing a high-payment short-term loan into a longer-term loan can lower your monthly obligation, thereby lowering your DTI.

If you find yourself in a position where your DTI is holding you back, it might be time to look at a home refinance to consolidate debt and improve your overall financial profile.

The Role of Compensating Factors

A high DTI isn't always an automatic "no." Lenders often look for "compensating factors" that balance out the risk of a higher debt load.

Cash Reserves: Having six to twelve months of mortgage payments in a savings account shows the lender you can handle the debt even if your income is temporarily interrupted.

High Credit Score: A score above 740 tells the lender that you have a historical habit of managing debt responsibly, regardless of the ratio.

Significant Down Payment: Putting 20% or more down reduces the lender's risk and can lead to more flexibility regarding your DTI limits.

If you are ready to see where your numbers land, you can start the loan process today to get a clear picture of your borrowing power.

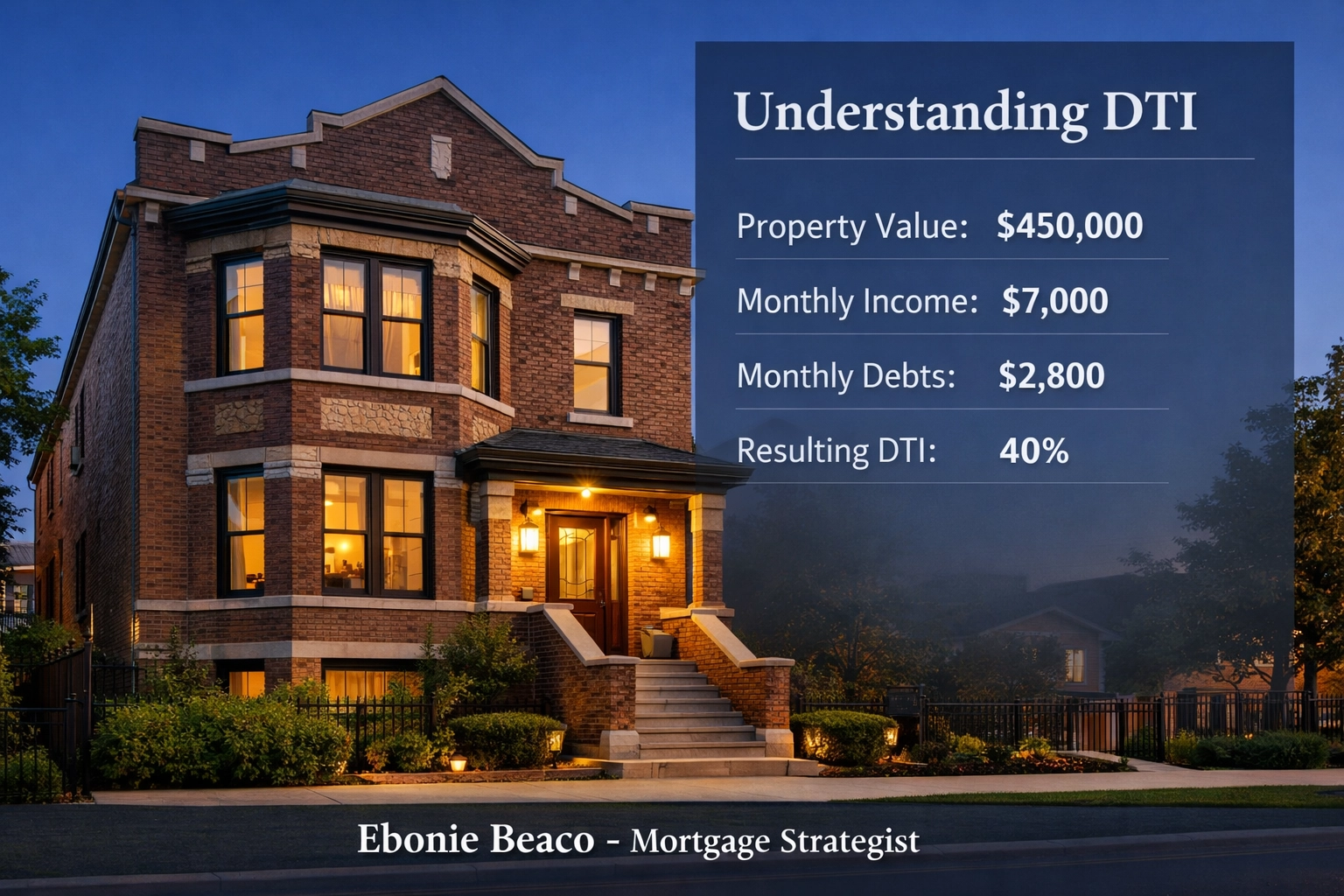

Real-World Scenario: The Chicago Homebuyer

Imagine a homebuyer in Chicago looking at a property valued at $450,000.

Gross Monthly Income: $7,000 Existing Car Payment: $400 Student Loan Payment: $200 Proposed Mortgage Payment (PITI): $2,200

Total Monthly Debt = $2,800 DTI Calculation: $2,800 / $7,000 = 40%

In this scenario, the buyer sits comfortably within the range for an FHA loan and is likely eligible for a Conventional loan depending on their credit score. This transparency allows the buyer to shop with confidence.

Image Description: A professional real estate deal breakdown titled "Understanding DTI". It shows a case study for a $450,000 property. Income: $7,000. Debts: $400 car, $200 student loan, $2,200 mortgage. Total Debt: $2,800. Final DTI: 40%. The text at the bottom reads "Ebonie Beaco - Mortgage Loan Officer". The visual uses professional charts without any cash or money icons.

Image Description: A professional real estate deal breakdown titled "Understanding DTI". It shows a case study for a $450,000 property. Income: $7,000. Debts: $400 car, $200 student loan, $2,200 mortgage. Total Debt: $2,800. Final DTI: 40%. The text at the bottom reads "Ebonie Beaco - Mortgage Loan Officer". The visual uses professional charts without any cash or money icons.

Final Thoughts on DTI

Your Debt-to-Income ratio is a snapshot of your financial health in the eyes of a lender. It is a vital metric, but it is not the only one.

Whether you are a seasoned investor in Alabama or a first-time buyer in Michigan, knowing your numbers puts you in the driver’s seat. By calculating your DTI early, you can take the necessary steps to improve it, explore home purchase options, or pivot toward investor-specific loan products that bypass personal DTI altogether.

Compare your options and gain clarity on your specific financial situation before you start your property search.

Need help lowering your DTI? Contact Ebonie Beaco for mortgage financing.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664