DSCR Vs. Bank Statement Loans: Which Is Better For Your Next Property?

SEO Title: DSCR Vs. Bank Statement Loans: Comparing 2026 Mortgage Strategies

Meta Description: Explore the differences between DSCR and Bank Statement loans. Learn which non-QM mortgage strategy fits your investment goals in Chicago, Florida, and beyond.

URL Slug: dscr-vs-bank-statement-loans-comparison

Featured Image Recommendation: A professional landscape image of a Chicago skyline integrated with a financial dashboard showing investment metrics and the REI Vault Pro brand logo.

SEO Alt Text: Chicago city skyline with a real estate investment financial dashboard overlay for REI Vault Pro.

Social Media Excerpt: Choosing between a DSCR loan and a Bank Statement loan? Our latest guide breaks down the math, the qualification rules, and which strategy helps you scale your real estate portfolio faster in 2026. 🏠📈 #RealEstateInvesting #DSCR #BankStatementLoans #REIVaultPro

SEO Tags: DSCR loans, bank statement loans, real estate investment financing, non-QM mortgages, self-employed mortgage, landlord loans, Chicago real estate, Florida real estate investment, REI Vault Pro.

Choosing the right financing strategy is often the difference between a stalled portfolio and rapid growth.

For real estate investors and self-employed professionals, traditional mortgage paths are frequently blocked by tax returns that show low net income.

In 2026, two powerful non-QM (non-qualified mortgage) solutions have emerged as the primary alternatives: DSCR loans and Bank Statement loans.

This guide explores the technical differences, qualification requirements, and real-world applications of both programs across markets like Chicago, Florida, Georgia, and California.

Explore these options to find the best fit for your financial profile and long-term property goals.

Understanding DSCR Loans for Investors

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its debt obligations through its own rental income.

The primary benefit of this program is that it decouples your personal income from the loan approval process.

Lenders focus almost exclusively on the asset itself rather than your W-2s or tax history.

This makes DSCR loans the preferred choice for scaling a rental portfolio in high-demand markets like Michigan and Virginia.

How DSCR Qualification Works

Qualification hinges on a simple ratio: the property's gross monthly rent divided by the total monthly debt (PITIA).

PITIA: An acronym for Principal, Interest, Taxes, Insurance, and Association dues (HOA).

If the rent exceeds the debt, the property is "cash-flow positive," and the loan is likely to be approved.

Investors frequently use the AI Market Analysis tool to verify that local market rents support the required ratio.

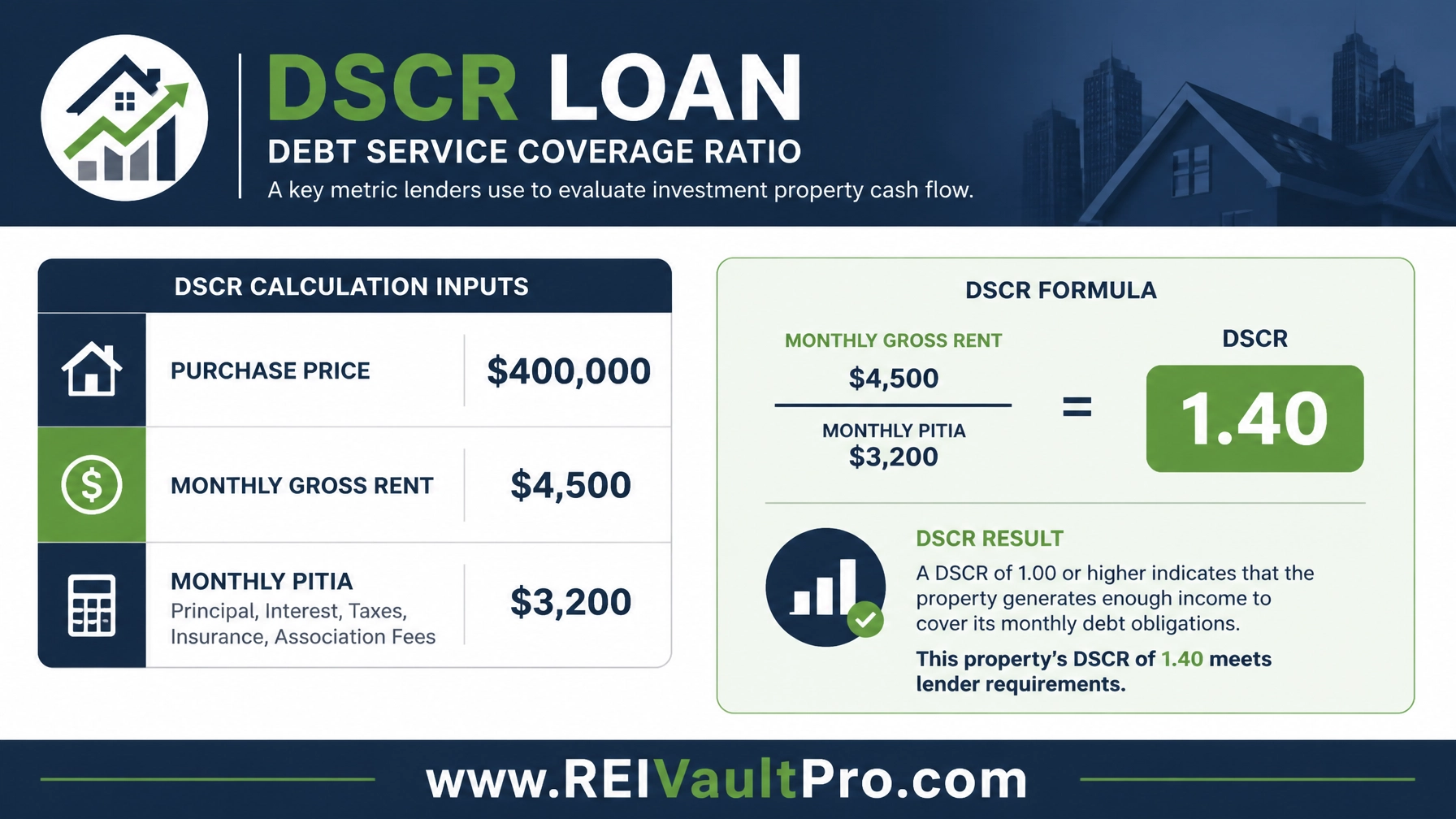

Real-World DSCR Example: Chicago Duplex

Imagine you are purchasing a duplex in Chicago for $400,000.

You intend to use it as a long-term rental property.

- Purchase Price: $400,000

- Monthly Gross Rent: $4,500

- Monthly PITIA: $3,200

To find the ratio, we divide $4,500 by $3,200, resulting in a DSCR of 1.40.

A ratio of 1.40 is considered very strong, as most lenders only require a minimum of 1.00 to 1.25.

Access the AI Deal Analyzer to run these numbers for your next acquisition.

Understanding Bank Statement Loans for the Self-Employed

Bank Statement Loan: A mortgage program that uses a borrower’s average monthly bank deposits to verify income instead of traditional tax returns.

This program is specifically designed for business owners, contractors, and entrepreneurs.

In states like California and Georgia, where many professionals have complex income structures, this loan provides a path to homeownership without the hurdle of tax write-offs.

It allows you to qualify for a primary residence or an investment property based on the actual cash flow passing through your accounts.

How Bank Statement Qualification Works

Lenders typically review either 12 or 24 months of business or personal bank statements.

They apply an Expense Factor, a standardized percentage deducted from total deposits to account for business operating costs.

Expense Factor: A percentage (often 50%) subtracted from total bank deposits to estimate the net qualifying income for a self-employed borrower.

The remaining amount becomes your "qualifying income" used to calculate your DTI.

DTI (Debt-to-Income Ratio): A personal finance measure that compares an individual’s monthly debt payments to their monthly gross income.

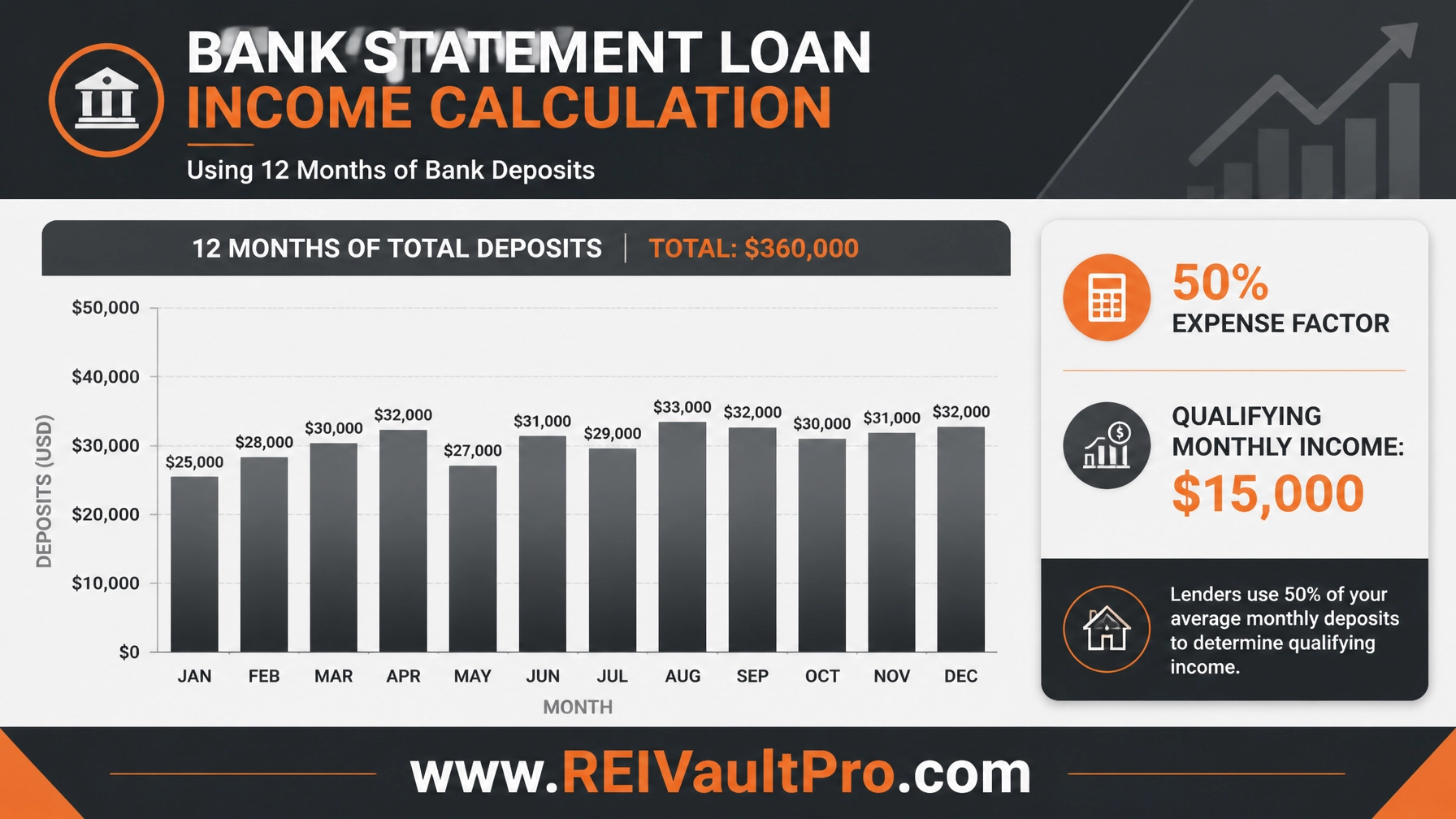

Real-World Bank Statement Example: Florida Primary Home

Consider a self-employed consultant in Florida purchasing a primary residence for $600,000.

While their tax returns show a low income due to business deductions, their bank statements tell a different story.

- 12-Month Total Deposits: $360,000

- Average Monthly Deposit: $30,000

- Qualifying Income (50% Expense Factor): $15,000

- Total Monthly Debt (New Mortgage + Personal Debt): $6,450

Dividing the $6,450 debt by the $15,000 income results in a 43% DTI.

This falls well within the standard 43% to 50% DTI limits for most bank statement programs.

You can compare how these income levels impact your borrowing power using the Investment Decision Engine.

Side-by-Side Comparison: Which Strategy Wins?

Comparing these two options requires looking at the property type and your specific employment status.

| Feature | DSCR Loan | Bank Statement Loan |

|---|---|---|

| Primary Goal | Property cash flow | Personal cash flow |

| Occupancy | Investment only | Primary, Second, or Investment |

| Key Metric | DSCR (Rent / Debt) | DTI (Income / Debt) |

| Income Docs | Leases / Market Rent | 12-24 Months Statements |

| Tax Returns | Never required | Never required |

| Best For | Scaling portfolios | Self-employed buyers |

Investors in Missouri and Indiana often choose DSCR loans because they do not impact their personal DTI as heavily.

However, if you are buying a primary home in Alabama or Arkansas, a Bank Statement loan is often the only viable non-QM path.

Jump in and use the AI Deal Scoring tool to see which financing structure supports a higher ROI.

Choosing the Right Loan for Your Next Move

The "better" loan depends entirely on your current situation.

If the property is a rental and the numbers are strong, a DSCR loan is usually faster and requires less paperwork.

It is an ideal fit for Airbnb and short-term rental financing where the income potential is high.

If you are self-employed and need a loan for a home you will live in, the Bank Statement loan is the standard.

Many professionals in Kentucky and Illinois use a mix of both strategies to build wealth while maintaining their personal lifestyle.

Before making a final decision, use the AI Listing Analyzer to evaluate the property’s potential performance under different loan terms.

Related REI Vault Pro Resources

- AI Deal Analyzer: This tool performs deep financial dives into any property, helping you calculate DSCR and cash flow with precision. It ensures you never overpay for an underperforming asset.

- AI Market Analysis: Access real-time data on rental rates and property values across the US. This is critical for proving market rent to DSCR lenders.

- Investment Decision Engine: A high-level strategic tool that helps you decide which financing path aligns with your 5-year and 10-year wealth goals.

- AI Deal Scoring: Quickly rank multiple potential properties based on their financing compatibility and projected ROI.

- AI Tools Showcase: Explore the full suite of REI Vault Pro technology designed to automate your underwriting and market research.

Whether you are targeting a multi-unit building in Chicago or a vacation rental in Florida, understanding these financing tools is the first step toward success.

Compare your options and secure the funding that moves you closer to your goals.

Watch a Demo to see how these tools simplify your next real estate transaction.

FAQ Section

Can I use a DSCR loan for a primary residence?

No, DSCR loans are strictly for investment properties. They rely on the property's ability to generate income, which does not apply to a home you intend to live in. For a primary residence, a bank statement loan is a more appropriate non-QM option.

How many bank statements do I need for a self-employed loan?

Most programs require either 12 or 24 months of consecutive statements. Using 24 months can sometimes help average out seasonal income fluctuations and provide a more stable qualifying income.

What is a good DSCR ratio in 2026?

While a 1.00 ratio means the property pays for itself, most lenders prefer a 1.20 or 1.25 ratio. A higher ratio often results in better interest rates and lower down payment requirements.

Do bank statement loans have higher interest rates?

Generally, yes. Because these loans carry higher risk and require manual underwriting, the interest rates are typically 0.75% to 2.0% higher than standard conventional mortgages.

Are these loans available for ITIN borrowers?

Yes, many non-QM lenders offer both DSCR and bank statement options for ITIN borrowers. These programs are vital for international investors looking to enter the US real estate market.