DSCR Loans 101: A Beginner's Guide to Mastering AI-Driven Rental Portfolio Growth

SEO Title: DSCR Loans 101: A Beginner's Guide to Mastering AI-Driven Rental Portfolio Growth

Meta Description: Learn how to grow your real estate portfolio using DSCR loans and AI-driven analysis. Understand calculations, scaling strategies, and financing for rental properties.

URL Slug: /dscr-loans-beginner-guide-ai-portfolio-growth

Featured Image Recommendation: A professional hero image featuring a modern Chicago apartment building with a digital financial overlay and REI Vault Pro branding.

SEO Alt Text: DSCR loan portfolio growth strategy with modern apartment buildings and AI deal analysis dashboard.

Social Media Excerpt: Stop letting personal income limit your growth. Our beginner's guide explores how DSCR loans and AI tools allow you to scale your rental portfolio based on property performance, not your W-2.

SEO Tags: DSCR loans, real estate investing, rental property financing, portfolio scaling, AI deal analyzer, landlord loans, cash flow management, REI Vault Pro.

Scaling a rental property portfolio often feels like a race against your own debt-to-income ratio. Traditional mortgage programs focus heavily on your personal tax returns, W-2 income, and existing debt, which can quickly stall your progress after just a few acquisitions.

DSCR Loans offer a strategic alternative by shifting the focus from the borrower’s personal income to the property’s ability to generate revenue. By leveraging this financing method alongside modern AI-driven analysis, you can evaluate deals faster and build a sustainable investment portfolio with greater efficiency.

Whether you are looking at multi-unit buildings in Chicago, short-term rentals in Florida, or single-family homes across Georgia and Virginia, understanding the mechanics of these loans is essential for long-term success.

Understanding the DSCR Loan Framework

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its own debt obligations through its generated rental income.

Practical Application: Lenders use this ratio to determine if a rental property produces enough cash flow to pay for its own mortgage, taxes, and insurance without relying on the owner's personal salary.

Unlike conventional financing, a DSCR loan is underwritten based on the cash flow of the subject property. This means you do not need to provide pay stubs or tax returns to qualify. The primary requirement is that the property "washes its own face", meaning the rent exceeds the monthly mortgage expense.

Lenders active in states like Alabama, Arkansas, and Indiana typically look for a ratio of 1.0 or higher. A ratio of 1.25 is often considered the "sweet spot" for securing the most competitive interest rates and terms.

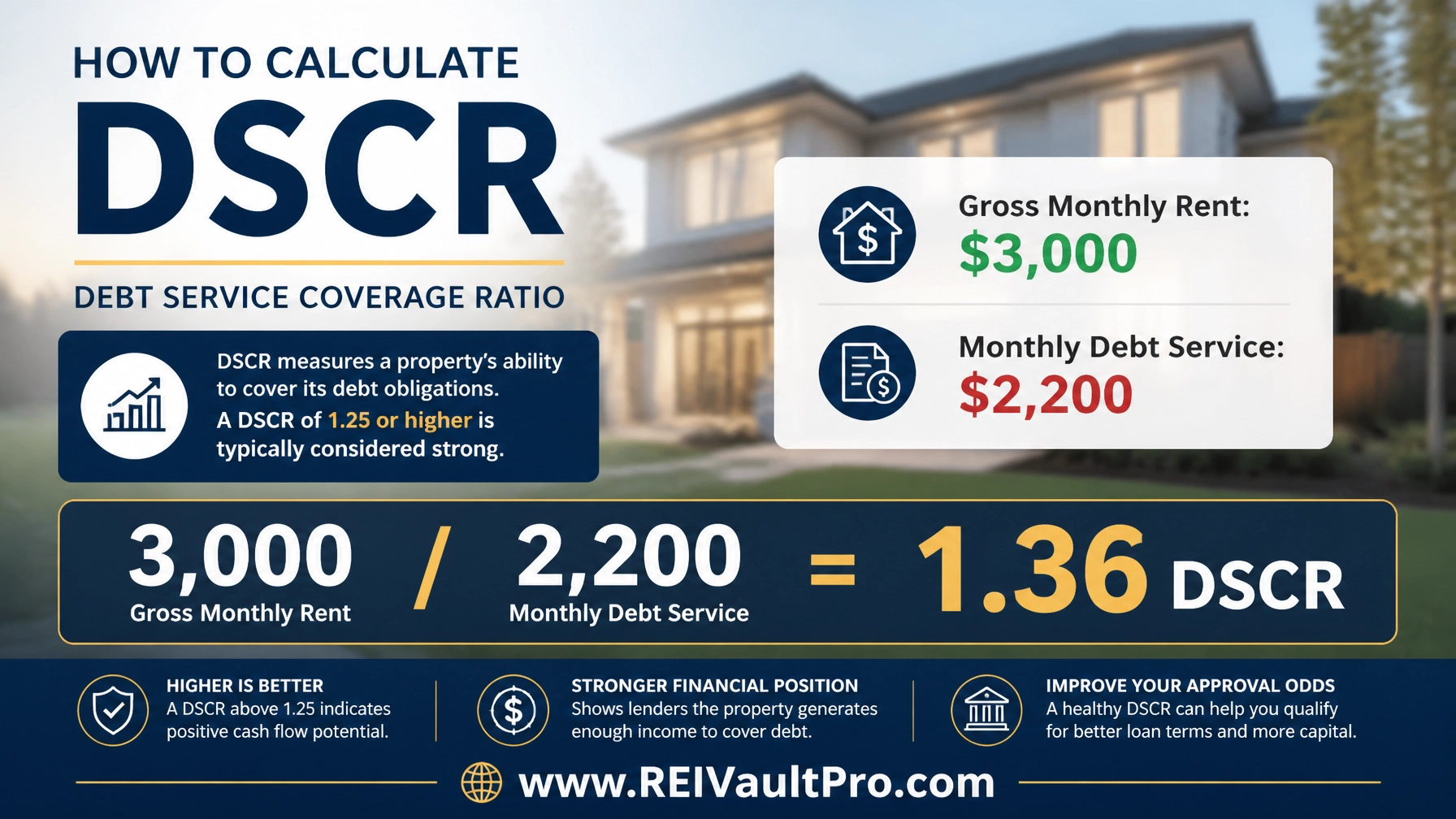

The Math Behind the Investment

To succeed with this strategy, you must be comfortable with the basic calculation. You can use the AI Deal Analyzer to automate this process, but knowing the manual steps helps you verify your targets.

The Formula:DSCR = Gross Monthly Rent / Monthly Debt Service (PITI)

Consider this real-world example for a property in St. Louis, Missouri:

- Purchase Price: $300,000

- Monthly Rent: $3,000

- Principal & Interest: $1,850

- Taxes & Insurance: $350

- Total Monthly Debt Service (PITI): $2,200

Calculation:$3,000 / $2,200 = 1.36

In this scenario, the DSCR is 1.36. Because the ratio is well above 1.0, the property is generating 36% more income than is required to pay the mortgage. This makes it an ideal candidate for a DSCR loan, likely qualifying you for better terms and faster approval.

Why DSCR is the Secret to Scaling

Traditional lending limits the number of properties you can own because every new mortgage increases your personal debt. Eventually, your Debt-To-Income (DTI) ratio becomes too high for traditional banks to approve another loan.

Scaling: The process of growing a real estate portfolio by acquiring multiple income-producing assets over a set period.

Practical Application: Using DSCR loans allows you to bypass DTI limits because the loan is tied to the property’s performance, enabling you to acquire 10, 20, or even 50 properties as long as each one meets the cash flow requirements.

For investors in high-growth markets like California or Kentucky, this flexibility is vital. You can jump in on new opportunities as they arise without waiting for your personal income to catch up to your investment goals.

Access the Investment Decision Engine to see how adding multiple properties impacts your overall portfolio health and projected wealth.

Using AI to Supercharge Your DSCR Strategy

In a competitive market, speed is a significant advantage. AI tools have transformed how investors identify and verify DSCR-eligible properties. Instead of manually searching through spreadsheets, you can now use data-driven platforms to find the best deals.

AI Market Analysis: Technology that processes vast amounts of local real estate data to identify trends, property values, and rental demand.

Practical Application: You can use AI Market Analysis to pinpoint neighborhoods in Michigan or Illinois where rental rates are rising, ensuring your target property will maintain a healthy DSCR over time.

Predicting Rents with Precision

The most critical variable in the DSCR equation is the rent. If your estimate is too high, your loan could be denied during the appraisal process. By using the AI Rent Analyzer, you get a highly accurate prediction based on real-time local comps. This ensures your projections are grounded in reality before you even submit a loan application.

Underwriting Your Own Deals

Before speaking with a lender, you can act as your own underwriter. The AI Underwriting tool allows you to plug in property data and see exactly how a lender will view the risk. This helps you filter out bad deals quickly so you can focus your time on properties that are guaranteed to cash flow.

The Step-by-Step Path to Your First DSCR Loan

If you are ready to explore this financing route, follow these steps to ensure a smooth process:

- Analyze the Market: Use AI Deal Scoring to find properties with the highest potential for cash flow in your target area.

- Calculate the Ratio: Ensure the projected rent is at least 1.0 to 1.25 times the expected mortgage payment.

- Verify the Condition: If the property needs work, use the AI Rehab Estimator to calculate renovation costs and how they might affect your final appraised value.

- Secure Your Financing: Apply for a DSCR loan specifically designed for investors. Since these are Non-QM (Non-Qualified Mortgage) loans, the process is often much faster than traditional banking.

- Repeat the Process: Once the property is leased and performing, use the equity or cash flow to move on to your next acquisition.

Navigating Local Market Nuances

Real estate is inherently local. What works for a multi-unit building in Chicago might differ from a single-family rental in Florida.

- Florida & Georgia: These markets often see high demand for short-term rentals (STRs). Some DSCR lenders allow you to use projected Airbnb income to qualify, provided you have a strong analysis of the seasonal fluctuations.

- Midwest (IL, IN, MI, MO): These states often offer lower entry prices, making it easier to achieve a high DSCR ratio with a standard 20% to 25% down payment.

- High-Value Markets (CA, VA): In these areas, investors often use DSCR loans to acquire properties with "value-add" potential, where increasing the rent after minor renovations can significantly boost the ratio and the property's value.

Explore our Platform Updates to see the latest data integrations for these specific regional markets.

Related REI Vault Pro Resources

- AI Deal Analyzer: Instantly calculate DSCR, cap rates, and ROI for any property listing. This tool helps you determine if a deal is worth pursuing in seconds.

- AI Rent Analyzer: Access hyper-local rental data to ensure your DSCR projections are accurate and realistic for the current market.

- AI Underwriting: Pre-screen your deals through a digital underwriting lens to see how lenders will evaluate your property's cash flow.

- Investment Decision Engine: Compare different financing scenarios and see how DSCR loans impact your long-term portfolio growth compared to traditional financing.

- AI Market Analysis: Stay ahead of trends in states like FL, GA, and IL with data-driven insights into where the next rental hotspots are emerging.

Conclusion

DSCR loans provide a powerful pathway for both new and experienced investors to scale their portfolios without the constraints of traditional debt-to-income limits. By focusing on property performance and utilizing AI-driven tools to verify your data, you can build a robust real estate business with confidence.

Explore the tools designed to help you analyze, underwrite, and manage your investments more effectively.

Watch a Demo to see how AI can transform your rental property strategy today.

FAQ Section

What is the minimum credit score for a DSCR loan?

Most lenders require a minimum credit score of 620 to 680. However, higher scores often lead to more favorable interest rates and lower down payment requirements.

Can I get a DSCR loan for a primary residence?

No. DSCR loans are strictly for investment properties and are designed for non-owner-occupied rentals. Using them for a primary residence would violate the loan terms and lending regulations.

How much down payment is required for a DSCR loan?

Standard down payments typically range from 20% to 25%. Some programs may allow for lower down payments if the property's DSCR ratio is exceptionally high or if the investor has significant experience.

Do DSCR loans have prepayment penalties?

Yes, many DSCR loans include a prepayment penalty period, often ranging from one to five years. It is important to review these terms if you plan on selling or refinancing the property in the near future.

Can I use a DSCR loan for an Airbnb or short-term rental?

Yes. Many lenders now offer DSCR programs specifically for short-term rentals. They may use specialized data to estimate the property's potential income based on its performance as a vacation rental.

Is a DSCR loan considered a commercial loan?

While they are used for business purposes (investing), DSCR loans for 1-4 unit properties are typically considered residential investment loans. Properties with 5 or more units are classified as commercial.