DSCR Loan Ratios Explained: Why Florida and Chicago Investors are Pivoting Today

The landscape for real estate investment is undergoing a significant transformation as we move through May 2026. For investors navigating the high-demand markets of Florida and the complex regulatory environment of Chicago, traditional financing is often no longer the most efficient path to growth. Instead, many are turning toward a specialized financing vehicle that prioritizes the performance of the asset over the personal income of the borrower.

Debt Service Coverage Ratio (DSCR) loans have emerged as a primary tool for scaling portfolios in states like Florida, Illinois, Georgia, and Virginia. By focusing on the cash flow of the property, these loans allow investors to bypass the rigid debt-to-income (DTI) requirements that often stall progress with conventional lenders. Explore why the specific ratio of your property is now the most critical factor in your acquisition strategy.

Understanding the Core Metrics

To navigate the current market, you must first master the fundamental language of investor financing. These metrics determine not only your eligibility for a loan but also the interest rate and leverage you can expect.

Debt Service Coverage Ratio (DSCR): A financial metric used to evaluate a property's ability to cover its own debt payments using only its generated rental income.

Practical Application: Lenders use this number to ensure the property brings in enough rent to pay the mortgage, taxes, insurance, and association fees without needing your personal paycheck.

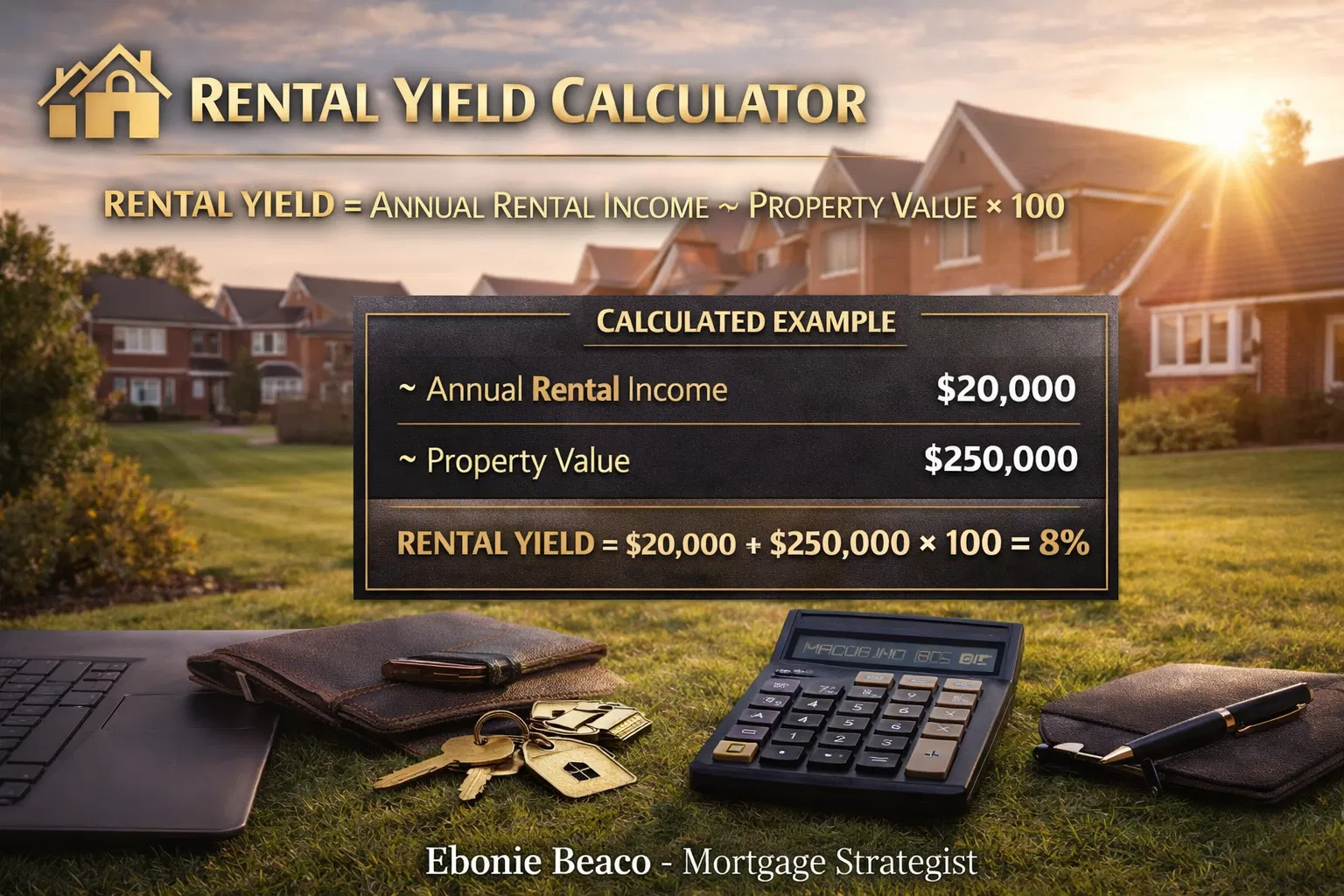

Net Operating Income (NOI): The total income generated from a property after all operating expenses are deducted but before debt service or taxes are paid.

Practical Application: This figure represents the true "earning power" of your real estate asset and serves as the numerator in the DSCR calculation.

Loan-to-Value (LTV): The ratio of the loan amount compared to the appraised value or purchase price of the property.

Practical Application: Most DSCR programs in markets like Chicago or Miami currently cap at 75% to 80% LTV, requiring a 20% to 25% down payment.

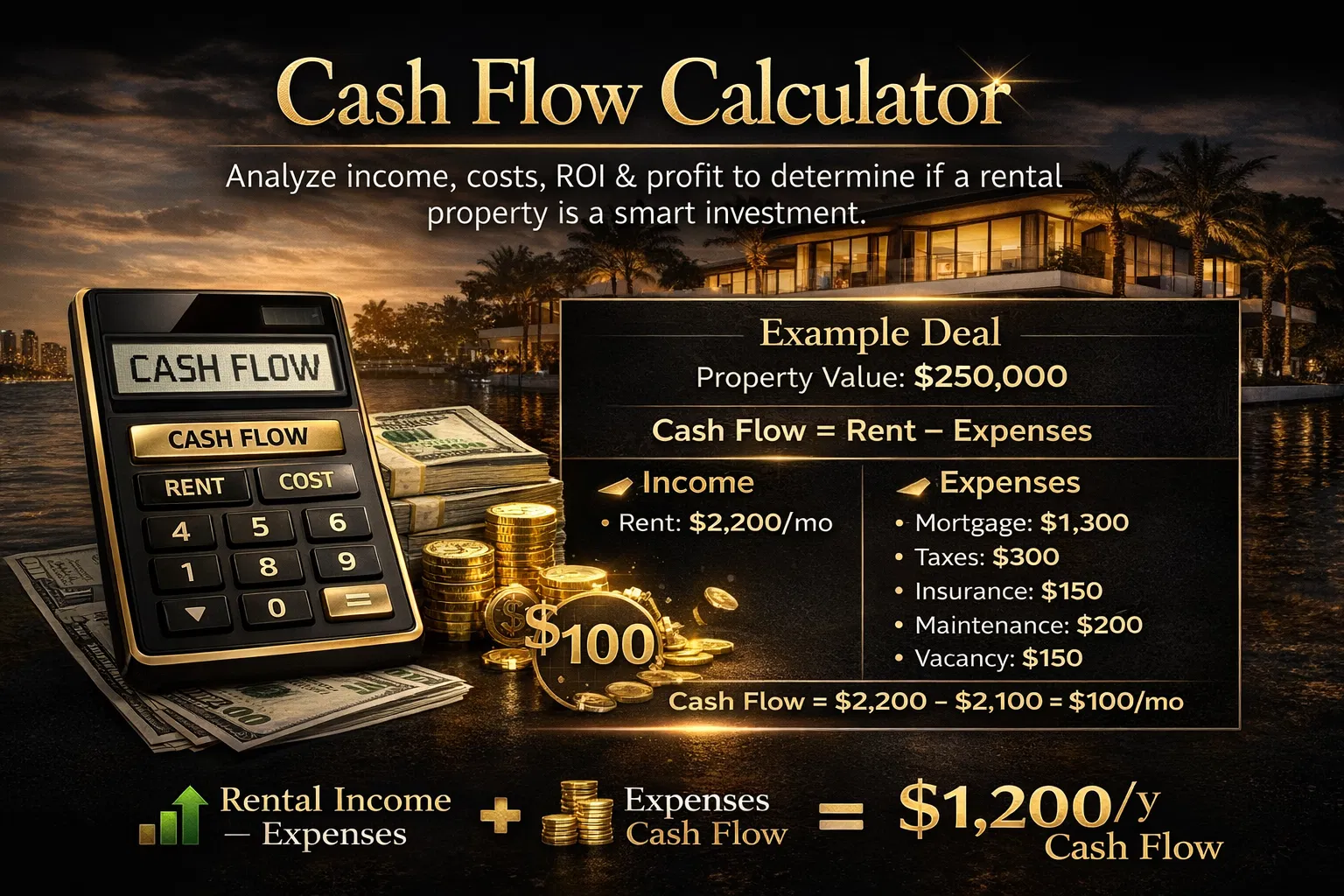

The Calculation That Governs Your Growth

The math behind a DSCR loan is straightforward but unforgiving. The formula is: Annual Net Operating Income ÷ Annual Debt Service. If your property generates $30,000 in annual net rent and your mortgage payments (including taxes, insurance, and HOA) total $24,000, your ratio is 1.25.

In today's environment, a ratio of 1.25 or higher is typically the threshold for the most competitive interest rates and highest leverage. While some specialized programs allow for ratios as low as 0.75 or 1.0, these often come with higher costs or lower LTV requirements. You can access our mortgage calculators to run these scenarios for your own prospective deals.

For investors in Alabama, Michigan, and Indiana, where property prices are often lower relative to rents, achieving a high ratio is frequently easier than in high-cost coastal markets. However, regardless of the location, the focus remains entirely on whether the property "stands on its own two feet" financially.

Why Florida Investors are Adjusting Their Sails

Florida remains a powerhouse for both long-term and short-term rentals, but the "Sunshine State" faces unique headwinds that make DSCR analysis essential. Rapidly increasing property insurance premiums and rising Homeowners Association (HOA) fees have compressed margins for many landlords in cities like Tampa, Orlando, and Cape Coral.

Because DSCR lenders include insurance and HOA costs in the "Debt Service" portion of the calculation, a property that looked like a winner two years ago might struggle to qualify today. Florida investors are pivoting by targeting sub-markets with lower insurance risks or by focusing on short-term rental (STR) strategies. Many DSCR programs now allow the use of "AirDNA" or market projections for Airbnb income, which can significantly boost the calculated NOI and help you qualify for better terms.

Jump in and compare our loan programs to see how short-term rental income can be utilized to strengthen your application. This flexibility is a primary reason why Florida investors are moving away from traditional banks that often do not recognize the full potential of vacation rental income.

The Chicago Pivot: Overcoming High Property Taxes

In Chicago and the surrounding Cook County areas, the challenge is often property taxes rather than insurance. Illinois investors must account for high tax assessments that can severely impact the cash flow ratio of a multi-unit building or a single-family rental.

Chicago investors are pivoting to DSCR loans because they allow for the acquisition of properties through an LLC. This structure provides a layer of liability protection and makes it easier to manage a growing portfolio. Furthermore, as many local investors reach their "conventional limit" of 10 financed properties under Fannie Mae or Freddie Mac guidelines, DSCR loans offer an unlimited path to scaling.

Whether you are looking at a three-flat in Logan Square or a portfolio of rentals in Gary, Indiana, the property-focused underwriting of a DSCR loan simplifies the loan process. It eliminates the need for tax returns and W-2s, focusing instead on the actual performance of the real estate in the Illinois market.

DSCR vs. Conventional: Choosing the Right Path

While conventional investment loans typically offer lower interest rates, they come with a "hassle factor" and strict DTI limits that can stop an active investor in their tracks. DSCR loans are designed for speed and scalability.

- Documentation: Conventional loans require years of tax returns; DSCR loans require a lease agreement or a market rent appraisal.

- Qualification: Conventional looks at your personal debt; DSCR looks at the property's debt coverage.

- Ownership: DSCR loans are built for LLCs and corporations; conventional loans are usually restricted to individuals.

- Speed: Closing a DSCR loan can often be significantly faster because the underwriting is less invasive.

According to research from the National Association of Realtors, wealth building through real estate is most effective when investors can leverage assets strategically. DSCR loans provide that strategic edge by separating your personal finances from your business assets.

Strategies to Improve Your Ratio Today

If a property you are eyeing is falling short of the 1.20 or 1.25 ratio mark, you have several levers to pull. Improving the ratio is not just about getting the loan; it is about ensuring your investment is fundamentally sound and resilient to market shifts.

- Reduce Expenses: Shop for more competitive insurance quotes or appeal property tax assessments in high-tax jurisdictions like Illinois or Virginia.

- Increase Revenue: Implement utility bill-back systems (RUBS), add coin-operated laundry, or offer premium amenities like reserved parking to boost NOI.

- Lower the Leverage: By moving from an 80% LTV to a 70% LTV, you reduce the annual debt service, which naturally increases the DSCR ratio.

- Improve Credit: Even though DSCR loans focus on the property, your FICO score still influences the interest rate, which in turn affects your debt service.

Compare how your credit score might influence your final mortgage rate by viewing our credit score and rate visualization. Small improvements in your personal profile can lead to significant savings on the property's debt service.

{kind=link}

Navigating Today's Market with Expert Guidance

The pivot toward DSCR loans in Florida and Chicago is a response to a more sophisticated real estate environment. Investors in 2026 recognize that scalability requires specialized tools. Whether you are conducting a cash-out refinance to fund your next acquisition or purchasing your first rental property in Georgia or Missouri, understanding your debt service ratio is the first step toward success.

You should not have to navigate these complex calculations alone. A knowledgeable mortgage strategist can help you analyze the numbers and select the program that aligns with your long-term wealth-building goals. Explore your options and ensure your portfolio is built on a foundation of strong cash flow and smart financing.

Are you ready to see if your property qualifies for a DSCR loan?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664