Derby Dreams & Duplex Cash: A Louisville Case Study on Cash-Out Refinance Success

If you have spent any time in Louisville lately, you know the vibe is shifting. It is March 2026, and the air smells like blooming magnolias and cold brew. But for real estate fans, the real scent in the air is opportunity.

While the rest of the country is still rubbing its eyes and waking up, the Louisville housing market has seen an inventory surge of nearly 30% this year. With rates hovering around a steady 6%, the "wait and see" crowd is officially missing out.

Enter Big Dave.

Dave is a local legend in the Germantown neighborhood. He owns a charming, slightly crooked duplex that he bought years ago when "Germantown" was just a place you went for a cheap bratwurst. Today, it is the heartbeat of the city's rental market.

Dave had a problem, though. He had a massive attic in that duplex that was currently home to three spiders, a box of 1990s basketball cards, and a lingering sense of wasted potential. With the Kentucky Derby around the corner, Dave realized that "potential" could actually be a high-end short-term rental that would pay for his mortgage for the next six months in a single weekend.

He just didn't have the $50,000 needed to turn a dusty attic into a luxury loft.

The Strategy: Kentucky Cash Out Refinance Mortgage (Germantown, Louisville)

With Louisville inventory up about 30% in 2026 and average mortgage rates hovering near 6%, Big Dave used a refinance strategy to move fast while other buyers waited.

Dave called me up. He was worried that a Kentucky cash out refinance mortgage would be too complicated or that he’d lose his "golden" interest rate from four years ago.

I told him, "Dave, your equity is sitting in that attic doing nothing. Let's put it to work."

A cash-out refinance is when you replace your existing mortgage with a new one for more than you owe on the property. You take the difference in cash. It is one of the most practical tools for Kentucky rental property financing, especially when you are repositioning an asset for a high-demand event like the Kentucky Derby.

For Big Dave, the goal was simple: fund an attic renovation in his Germantown duplex so he could capture Derby-week pricing with a premium short-term rental.

The "Big Dave" Breakdown:

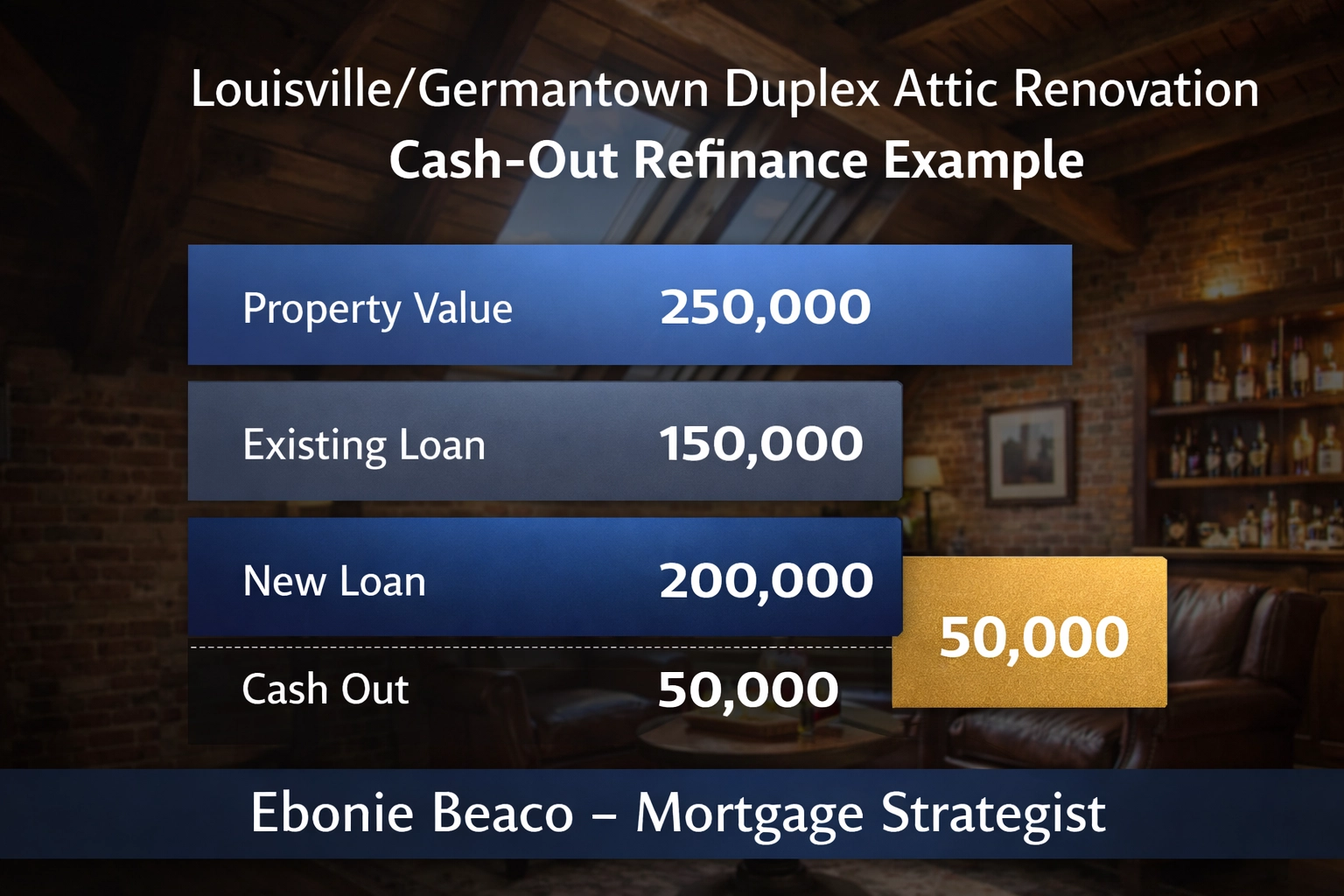

- Current Property Value: $250,000 (Germantown appreciation is real, folks).

- Current Mortgage Balance: $150,000.

- Maximum Loan-to-Value (LTV): 80%.

- New Loan Amount: $200,000.

- Cash in Dave's Pocket: $50,000 (minus some standard closing costs).

Visual Breakdown: Property Value 250k | Existing Loan 150k | New Loan 200k | Cash Out 50k. Text: Ebonie Beaco - Mortgage Strategist

Visual Breakdown: Property Value 250k | Existing Loan 150k | New Loan 200k | Cash Out 50k. Text: Ebonie Beaco - Mortgage Strategist

With $50,000 in the bank, Dave went to work. He added skylights, a sleek kitchenette, and enough bourbon-themed decor to make a distiller weep with joy.

By the time the first Saturday in May rolled around, Dave’s "Attic at the Tracks" was listed on Airbnb. He booked it for Derby week at $1,200 a night. Dave isn't just a landlord anymore; he is a hospitality mogul.

If you are looking to scale your portfolio, checking out our mortgage basics can help you understand how to leverage your current assets.

From Silicon Valley to Side Hustle: A California Cash-Out Story

While Big Dave was busy picking out paint colors in Louisville, Sarah in Sacramento was facing a different kind of crossroads.

Sarah had spent ten years in the tech world. She was tired of Zoom calls that could have been emails. She wanted to open a boutique plant shop and community space, but the "Seed Money" she needed felt more like a "Forest Amount" of cash.

In California, where equity grows faster than a backyard lemon tree, Sarah was sitting on a goldmine. She owned a bungalow in a neighborhood that had seen values skyrocket.

Why a Cash-Out Refi Beats a Business Loan

Sarah originally looked at a standard small business loan. The interest rates were double digits, and the paperwork required her to essentially sign over her firstborn child.

I suggested a different path: using a California cash out refinance.

Because mortgage rates, even at 6%, are significantly lower than unsecured business lines of credit or high-interest credit cards, Sarah could "borrow from herself."

The California Calculation:

- Home Value: $900,000.

- Existing Mortgage: $400,000.

- Cash Needed for Business: $150,000.

- New Mortgage Balance: $550,000.

Visual Breakdown: CA Home Value $900k | Current Loan $400k | New Loan $550k | Business Capital $150k. Text: Ebonie Beaco - Mortgage Strategist

Visual Breakdown: CA Home Value $900k | Current Loan $400k | New Loan $550k | Business Capital $150k. Text: Ebonie Beaco - Mortgage Strategist

Sarah took that $150,000 and secured her lease, bought her initial inventory, and hired a manager. By using her home equity, she kept her monthly overhead low enough to survive the first year of business.

She didn't just start a business; she bought her freedom.

If you are a self-employed individual or an aspiring entrepreneur in the Golden State, you might want to explore our loan programs to see which structure fits your cash flow needs.

Technical Terms You Should Know

To stay transparent (our favorite way to work at Home Loans Network), let’s define exactly what happened in these stories.

LTV (Loan-to-Value): This is the ratio of your loan amount compared to the appraised value of your home. Lenders typically allow up to 80% LTV for a cash-out refinance on a primary residence.

DSCR (Debt Service Coverage Ratio): Often used in Kentucky investment property loans, this measures the property's ability to pay its own mortgage based on rental income. You use it to compare payment risk against real rent numbers, which matters when you are underwriting Kentucky rental property financing on a duplex, multi-unit, or short-term rental setup.

Non-QM (Non-Qualified Mortgage): These are loans that don't fit the "standard" box. If you are self-employed like Sarah, a Non-QM loan using bank statements instead of tax returns can be a lifesaver.

Visual Chart: LTV vs. Equity. Labeled: 20% Equity Cushion | 80% Max Loan. Text: Ebonie Beaco - Mortgage Strategist

Visual Chart: LTV vs. Equity. Labeled: 20% Equity Cushion | 80% Max Loan. Text: Ebonie Beaco - Mortgage Strategist

Why 2026 is the Year of the Strategic Refinance

You might be thinking, "Ebonie, why would I refinance now?"

Here is the truth: The days of 2% interest rates are in the history books, right next to dial-up internet and floppy disks. But 6% is a historically healthy rate, especially when you consider that home values in places like Louisville and California have remained incredibly resilient.

A Kentucky cash out refinance mortgage isn't just about the rate; it's about the utilization of capital.

If you have $100,000 in equity, that money is effectively earning 0% interest sitting in your walls. If you pull that money out and invest it into a business or an income-producing rental, you are creating a "Return on Equity" that far outweighs the interest cost.

How to Get Started

Whether you are looking for Kentucky rental property financing to flip an attic like Big Dave or need a California investment property loan to launch your dream, the process starts with a plan.

- Check your equity: Get a professional valuation or talk to a strategist to see what your home is worth today.

- Define your goal: Are you renovating, starting a business, or consolidating debt?

- Review your credit: Even small bumps in your score can lead to better pricing.

- Analyze the math: We provide mortgage calculators to help you see the monthly impact.

Don't let your equity gather dust while the market moves forward without you. Whether you’re in the Bluegrass State or the West Coast, there is a strategy waiting for you.

Ready to see what your equity can do?

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

Visual: A checklist for Cash-Out Refinance Success. Labeled: Equity Check | Goal Setting | Rate Lock. Text: Ebonie Beaco - Mortgage Strategist

Visual: A checklist for Cash-Out Refinance Success. Labeled: Equity Check | Goal Setting | Rate Lock. Text: Ebonie Beaco - Mortgage Strategist

Frequently Asked Questions

Can I do a cash-out refinance on an investment property? Yes. Programs for Kentucky investment property loans often allow you to pull cash out of a rental to buy more properties. It is the classic "BRRRR" method (Buy, Rehab, Rent, Refinance, Repeat).

What are the closing costs like? Generally, they range from 2% to 5% of the loan amount. However, many investors roll these costs into the new loan so they don't have to pay out of pocket.

How long does it take? Most refinances close within 30 days. If you are preparing for a specific event (like the Derby!), we recommend starting at least 45 days in advance. Check our loan process page for a detailed timeline.

Is it worth it if my current rate is lower? It depends on what you do with the cash. If you pull $50k at 6% to pay off credit cards at 24%, you are winning. If you pull $50k to build a rental unit that earns $2,000 a month, you are winning even bigger.

Explore your options today. We are here to help you navigate the numbers with total transparency. Visit our FAQ for more details or reach out directly!