Credit Repair / Credit Optimization Guidance

Your credit score acts as the foundation for every real estate transaction, from your first home purchase in Chicago to scaling a rental portfolio in Florida. Credit repair and optimization involve a dual approach: identifying and disputing inaccuracies while strategically building positive history. Whether you are dealing with a thin credit file or recovering from past financial hurdles, improving your score unlocks lower interest rates and better loan terms. This guide breaks down the dispute process, the importance of credit utilization, and how to position yourself for programs like DSCR or bank statement loans. Optimization requires patience and a clear strategy, but the financial rewards are significant for long-term wealth building. Ready to elevate your borrowing power?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Defining the Path to Better Credit

Before diving into the tactics, it is important to distinguish between the two primary ways to improve your standing with lenders.

Credit Repair

Definition: The process of identifying and challenging inaccurate, outdated, or unverifiable information on your credit reports.

Practical Application: You use this strategy to remove a late payment that was actually paid on time or to delete an account that does not belong to you.

Credit Optimization

Definition: The strategic management of legitimate credit data to produce the highest possible credit score.

Practical Application: You use this to lower your credit utilization ratios or diversify your credit mix to prove financial stability to a mortgage lender.

Both strategies work together to help you qualify for mortgage basics and more advanced investment programs.

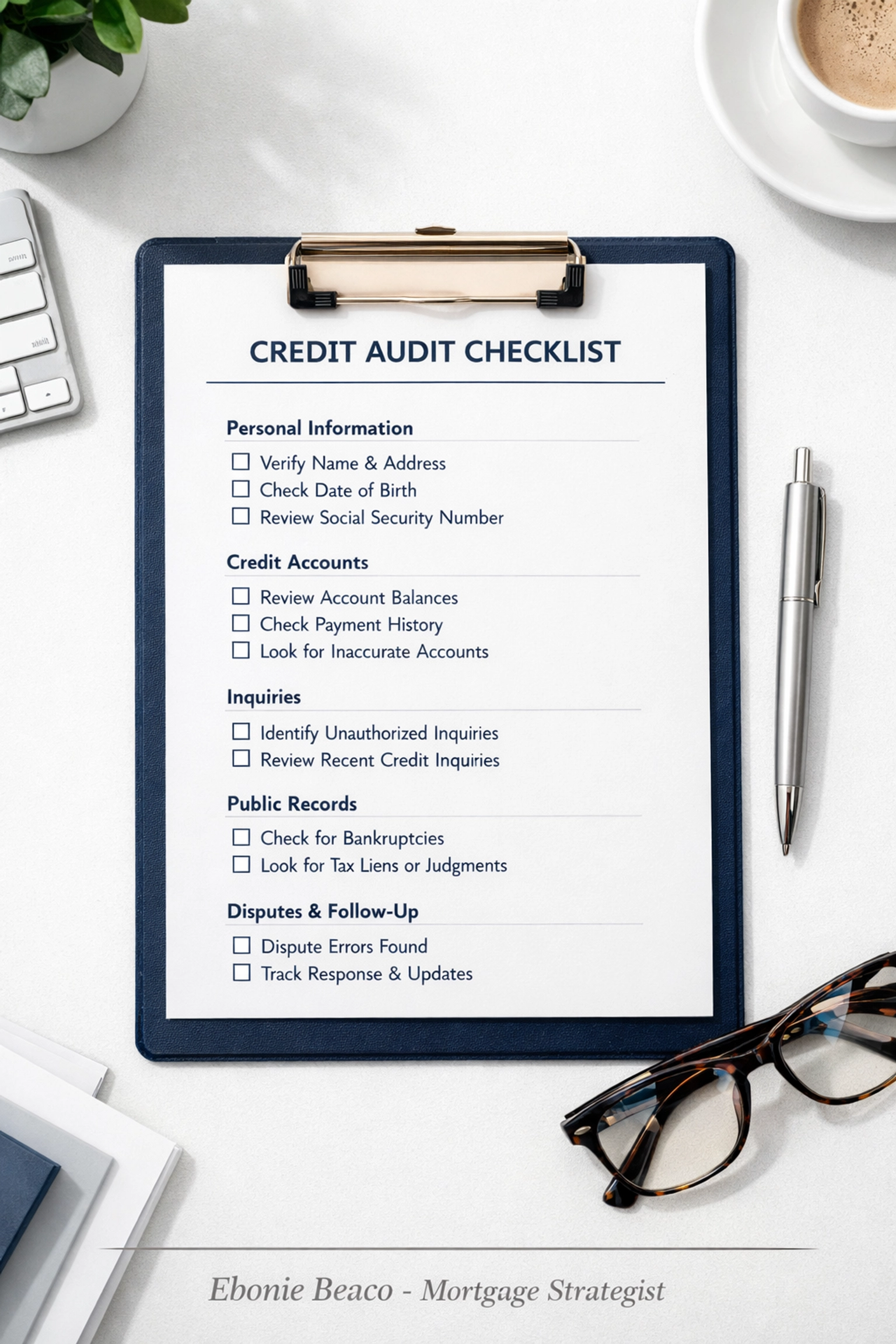

The Audit: Knowing Where You Stand

You cannot fix what you cannot see.

Accessing your credit reports from the three major bureaus: Equifax, Experian, and TransUnion: is the first step for any borrower in Alabama, Michigan, or California.

Under federal law, you are entitled to a free copy of your credit report from each bureau every twelve months. You can access these through AnnualCreditReport.com.

When you review these documents, look for specific red flags:

- Unfamiliar Accounts: These could be signs of identity theft or clerical errors.

- Inaccurate Payment Status: Ensure that accounts marked as late were truly delinquent.

- Incorrect Balances: High balances that have been paid down can negatively impact your score if they haven't updated.

- Duplicate Listings: The same debt appearing multiple times can unfairly tank your score.

Image Description: A professional credit report audit checklist showing categories like Personal Info, Account History, and Public Records. Footer: Ebonie Beaco - Mortgage Strategist. Title: Credit Report Audit Checklist.

The Dispute Process: Challenging Inaccuracies

If you find an error, you have the right to dispute it under the Fair Credit Reporting Act (FCRA).

The Dispute: A formal notification sent to a credit bureau challenging the validity of a specific item on a credit report.

Practical Application: Filing a dispute forces the bureau to investigate and verify the data with the original creditor.

The credit bureau generally has 30 days to investigate your claim. If the creditor cannot verify the information, the bureau must remove it.

Provide clear documentation for every dispute. This might include bank statements, canceled checks, or a letter from the creditor acknowledging an error.

For investors looking at DSCR rental property loans, a single removed error could be the difference between a 7.5% interest rate and a 6.5% interest rate.

Optimization Strategies for the Active Borrower

Sometimes, your credit report is 100% accurate, but your score is still lower than you would like. This is where optimization comes into play.

Lowering Credit Utilization

Definition: The ratio of your outstanding credit card balances to your total available credit limits.

Practical Application: Keeping your balances below 30% of your limits: or ideally below 10%: shows lenders you are not overextended.

Explore how your utilization impacts your home purchase options. If you have a $10,000 limit and a $9,000 balance, your 90% utilization suggests high risk.

Paying that balance down to $1,000 can result in a rapid score increase, sometimes within a single billing cycle.

Improving Payment History

Definition: A record of whether you have paid your bills on time over the life of your accounts.

Practical Application: Setting up autopay for the minimum amount due ensures you never miss a deadline, protecting the most influential part of your score.

Strategic Account Management

Avoid closing old credit card accounts. The length of your credit history accounts for a significant portion of your score.

Older accounts provide a "vintage" to your credit profile that reassures lenders in Virginia and Georgia that you have long term experience managing debt.

Image Description: A chart illustrating the components of a FICO score: 35% Payment History, 30% Amounts Owed, 15% Length of History, 10% New Credit, 10% Credit Mix. Footer: Ebonie Beaco - Mortgage Strategist. Title: FICO Score Components.

Credit Scores and Specific Loan Programs

Different loan programs have different requirements. Understanding where you fall helps you target the right loan programs.

- Conventional Loans: Typically require a 620 minimum, but a 740+ score secures the best pricing.

- FHA Loans: Allow for scores as low as 580 with a 3.5% down payment.

- DSCR Loans: Often require a 660 to 680 minimum for competitive investor terms.

- Bank Statement Loans: Self-employed borrowers in Indiana or Kentucky often need a 660+ score to offset the non-traditional income verification.

If you are currently below these thresholds, focus on a 90 day optimization sprint. Small changes in how you manage existing debt can lead to major shifts in eligibility.

Real World Scenario: The Chicago Refinance

Consider a homeowner in Chicago with a property valued at $450,000 and an existing mortgage of $300,000. They want a home refinance to access $50,000 for a kitchen remodel.

Their current credit score is 655.

The lender quotes an interest rate that feels a bit high.

By analyzing their credit, the homeowner realizes they have two credit cards at 85% utilization.

They use $10,000 from savings to pay those cards down to 5% utilization.

Within 45 days, their score jumps to 710.

This score improvement drops their offered interest rate by 0.5%, saving them thousands of dollars over the life of the loan.

Image Description: A comparison table showing Interest Rate vs. Credit Score. It shows how a 655 score gets one rate, while a 710 score gets a lower rate. Footer: Ebonie Beaco - Mortgage Strategist. Title: Impact of Credit Score on Interest Rates.

Managing Credit as a Self-Employed Professional

Business owners and 1099 contractors in states like Arkansas and Missouri face unique challenges.

Often, business expenses are put on personal credit cards. This can inflate your personal utilization and suppress your score, even if your business is thriving.

Jump in and separate your finances. Using business credit for business expenses keeps your personal credit report lean and optimized for a mortgage.

If you have questions about how your business debt affects your personal borrowing power, check our FAQ.

DIY Repair vs. Professional Guidance

You have the power to do everything a credit repair company does.

According to the Consumer Financial Protection Bureau, no one can legally remove accurate negative information from your report before it ages off (usually seven years).

If you choose to hire a professional, ensure they follow the Credit Repair Organizations Act (CROA).

- They must not charge upfront fees.

- They must provide a written contract.

- They must inform you of your right to cancel within three days.

Transparent guidance is the core of what we do at Home Loans Network. We prefer to educate you on the process so you can make informed decisions.

The Timeline for Improvement

Patience is a requirement.

While utilization changes can reflect in 30 to 45 days, removing inaccuracies or building a "thin" file can take six months or longer.

If you are planning to buy a home in Florida or Virginia later this year, start your credit optimization now.

Access online forms to begin the pre-approval process and see exactly where your scores land today.

Final Steps for the Savvy Borrower

Your credit score is a tool.

By focusing on the facts and ignoring the hype, you can position yourself for the best financing available in the market.

Explore your options, compare the numbers, and act with confidence.

Whether you are a first time buyer or a seasoned investor scaling a portfolio, a healthy credit profile is your most valuable asset.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664