Construction & Renovation: Financing Your Dream Project

Finding the perfect home in a tight market like Chicago or the coastal regions of Florida often feels like searching for a needle in a haystack. Sometimes, the best way to get your dream home is to build it or buy a "fixer-upper" and transform it. For real estate investors, renovation financing is the engine that drives the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat) or a successful fix-and-flip project in Georgia or Virginia.

Navigating the world of construction and renovation loans requires a clear understanding of how lenders view value. Unlike a traditional mortgage, these loans look at what the property will be worth once the dust settles.

Explore Renovation Financing Options

Standard mortgages typically require a property to be in "move-in condition." If a house has a hole in the roof or a non-functioning kitchen, a traditional lender will likely decline the file. Renovation loans solve this by allowing you to bundle the purchase price and the repair costs into a single loan.

Image Title: Renovation Financing Options | Ebonie Beaco - Mortgage Loan Officer

Image Title: Renovation Financing Options | Ebonie Beaco - Mortgage Loan Officer

FHA 203(k) Rehabilitation Mortgage

The FHA 203(k) loan is a popular choice for primary residents. It allows you to buy a home and include the costs of repairs in the mortgage with a down payment as low as 3.5%. This is a fantastic tool for first-time buyers in Michigan or Indiana looking to enter a neighborhood by purchasing a distressed property.

- Standard 203(k): Used for major structural repairs, additions, or projects exceeding $35,000.

- Limited 203(k): Designed for cosmetic repairs and minor updates under $35,000.

Fannie Mae HomeStyle Renovation

The HomeStyle loan is a conventional alternative that offers more flexibility than the FHA version. It is available to investors, which makes it a primary tool for those building a rental portfolio in Alabama or Arkansas. You can use it for luxury upgrades like landscaping or installing a pool, which FHA loans generally prohibit.

Freddie Mac CHOICE Renovation

Similar to the HomeStyle loan, the CHOICE Renovation program allows for a wide range of improvements. It is particularly useful for homes located in high-cost areas or for borrowers looking to improve a home's resilience against natural disasters, a common concern for property owners in California or Florida.

Compare these programs by visiting our Mortgage Basics page to see which aligns with your credit profile.

The Power of After Repair Value (ARV)

In the world of real estate investing and renovation, the most critical number is the After Repair Value (ARV). This figure represents the estimated market value of a property after all planned renovations and improvements are completed. Lenders use this number to determine how much they are willing to lend you.

Investors in Illinois and Virginia use ARV to ensure they aren't over-leveraging a project. If your total investment (purchase price + renovation costs) exceeds the ARV, you are "underwater" before you even finish the project.

Calculating ARV

To find the ARV, you look at "comparables": similar homes in the same neighborhood that have already been renovated.

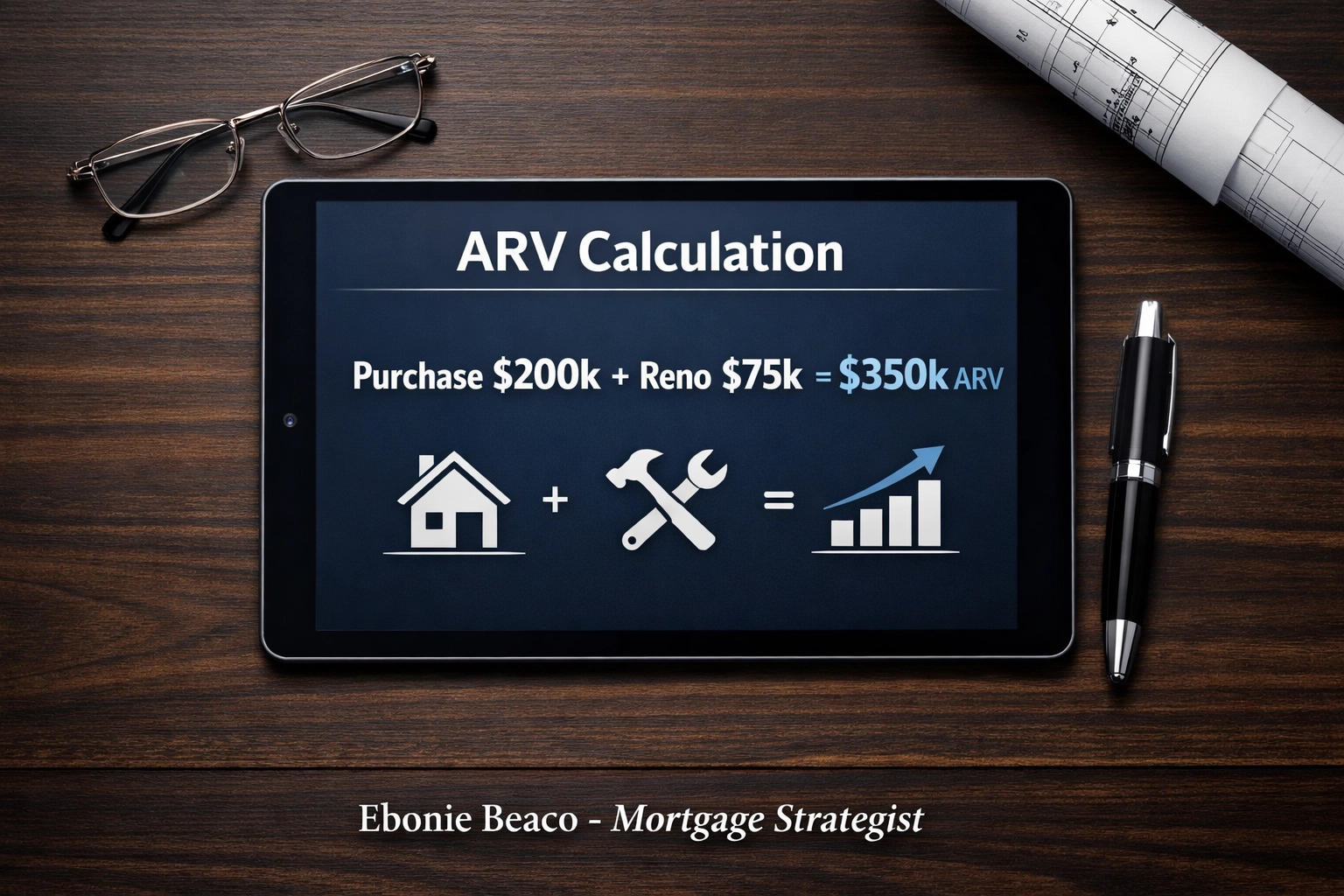

ARV Calculation Example:

- Purchase Price (As-Is): $200,000

- Renovation Budget: $75,000

- Value of Improved Comparable Homes: $350,000

- ARV: $350,000

In this scenario, your total cost is $275,000, and the property is worth $350,000. This leaves you with $75,000 in potential equity or profit.

Image Title: ARV Calculation: Purchase $200k + Reno $75k = $350k ARV | Ebonie Beaco - Mortgage Loan Officer

Image Title: ARV Calculation: Purchase $200k + Reno $75k = $350k ARV | Ebonie Beaco - Mortgage Loan Officer

Fix and Flip vs. Buy and Hold

How you finance your project depends heavily on your exit strategy.

Fix-and-Flip Investors: Usually prefer Hard Money Loans or Bridge Loans. These are short-term, interest-only loans that prioritize the asset's value over the borrower's personal income. They offer speed, which is essential when bidding on distressed properties in competitive markets like Atlanta or Miami.

Buy-and-Hold Landlords: Might start with a renovation loan to stabilize the property and then transition into a DSCR (Debt Service Coverage Ratio) Loan. A DSCR loan allows you to qualify based on the property’s rental income rather than your personal debt-to-income ratio. You can learn more about this on our FAQ page.

Financing for Current Homeowners

You don’t have to buy a new house to benefit from renovation financing. If you already own a home in Kentucky or Missouri and want to add an extra bedroom or modernize your kitchen, you have options.

Cash-Out Refinance

A Cash-Out Refinance involves replacing your current mortgage with a new, larger loan and taking the difference in cash. This is a great way to use your existing equity to fund a large-scale renovation.

HELOC (Home Equity Line of Credit)

A HELOC acts like a credit card secured by your home. You only pay interest on what you use, making it ideal for projects where costs are spread out over several months. This flexibility is a favorite for homeowners who want to manage their renovation budget dynamically.

Steps to Secure Construction Financing

- Get Pre-Approved: Before talking to contractors, you need to know your buying power. Use our Mortgage Calculators to estimate your monthly payments.

- Define the Scope of Work: Create a detailed list of every repair and upgrade you plan to make.

- Hire a Licensed Contractor: Most renovation loans require the work to be done by a professional. The lender will review the contractor's credentials and the detailed bid.

- The Appraisal: The appraiser will review your renovation plans and the current state of the house to determine the "Subject to Completion" value (the ARV).

- Closing and Draws: Once the loan closes, the renovation funds are typically held in an escrow account. As work is completed, the lender releases "draws" to pay the contractor after inspecting the progress.

Image Title: The Renovation Loan Process | Ebonie Beaco - Mortgage Loan Officer

Image Title: The Renovation Loan Process | Ebonie Beaco - Mortgage Loan Officer

Why the Right Strategist is Key

Construction and renovation loans have more moving parts than a standard purchase. You are coordinating with a lender, an appraiser, a contractor, and sometimes a consultant (required for some FHA 203k loans).

Transparency throughout this process is vital. You need to know exactly how the draw schedule works and how interest is charged during the construction phase. Whether you are a first-time flipper in California or a seasoned landlord in Florida, having a mortgage strategist who understands the nuances of the local market can save you thousands in holding costs.

Access our Loan Process guide to see how we streamline these complex transactions.

Common Pitfalls to Avoid

- Underestimating Costs: Always include a contingency fund (usually 10-20% of the budget) for unexpected issues like mold, outdated wiring, or structural surprises.

- Over-Improving for the Neighborhood: Just because you spend $100,000 on a kitchen doesn't mean the house value will increase by $100,000. Stay aligned with local "comps."

- Choosing the Wrong Loan Product: Using a hard money loan for a long-term rental might eat up your cash flow due to high interest rates. Always look at the long-term goal.

Jump in and start your project with confidence. By understanding the relationship between renovation costs, market value, and loan products, you can turn a dilapidated property into a high-value asset.

Ready to renovate? Contact Ebonie Beaco for construction and renovation financing.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664