Commercial Real Estate Loans: Navigating the Complexities

Entering the world of commercial real estate (CRE) is a significant milestone for any investor. Whether you are eyeing a retail strip in Chicago, an apartment complex in Tampa, or an industrial warehouse in Virginia, the way you structure your debt often determines your ultimate success. Commercial financing operates on a different set of rules compared to residential mortgages. While residential loans focus heavily on your personal income, commercial loans shift the spotlight toward the property’s ability to generate revenue.

Understanding these nuances is essential if you want to scale your portfolio or transition from single-family rentals into larger assets. This guide explores the various loan types, the math behind the deals, and the strategies professional investors use to secure funding in today’s market.

Defining Commercial Real Estate Loans

A commercial real estate loan is a mortgage debt specialized for properties used for business purposes or multi-unit residential buildings.

Commercial Loan: A debt instrument secured by a lien on a commercial property rather than a residential one. Practical Application: You use these loans to acquire office buildings, shopping centers, hotels, or apartment buildings with five or more units.

Unlike residential loans that are often sold to Fannie Mae or Freddie Mac, commercial loans are frequently held by banks or packaged into securities. This means the terms can vary wildly depending on the lender's appetite for a specific asset class or geographic region.

Traditional Bank Loans

Traditional bank loans, often called permanent loans, are the bedrock of the commercial industry. These are typically issued by local, regional, or national banks for stabilized properties that already have tenants and consistent cash flow.

Permanent Loan: A long-term mortgage on a piece of commercial real estate that has reached stabilization. Practical Application: If you own a fully leased medical office in Michigan and want to lock in a steady rate for the next decade, a traditional bank loan is your primary path.

These loans usually offer competitive interest rates but come with strict underwriting. Lenders will look for a strong credit history and a proven track record of property management. You can explore more about these foundational concepts at Home Loans Network Mortgage Basics.

Government-Backed Options: SBA 7(a) and 504

For business owners who intend to occupy a significant portion of the property, the Small Business Administration (SBA) offers some of the most attractive terms available.

SBA 7(a) Loan: A versatile government-backed loan used for real estate, working capital, or debt refinancing. Practical Application: A business owner in Georgia purchasing a warehouse for their own logistics company can utilize a 7(a) loan to get a lower down payment than traditional financing.

SBA 504 Loan: A loan program providing long-term, fixed-rate financing for major fixed assets like real estate. Practical Application: This is often structured with a bank covering 50% of the cost, the SBA covering 40%, and the borrower contributing only 10%.

These programs are excellent for preserving capital, though they do require the borrower’s business to occupy at least 51% of the building.

CMBS: Commercial Mortgage-Backed Securities

CMBS loans, also known as conduit loans, are pooled together and sold as bonds to investors. These are popular for large-scale investments because they often offer non-recourse terms.

Non-Recourse Debt: A type of loan where the lender's only remedy in case of default is to seize the collateral property, not the borrower's personal assets. Practical Application: An investment group buying a $10 million apartment complex in California might choose a CMBS loan to protect their personal wealth from the risks associated with the specific project.

Conduit loans typically require a minimum loan amount of $2 million and have fixed terms, usually 5 or 10 years, with 25 to 30-year amortization schedules.

The Mathematics of Commercial Financing: LTV

One of the first things a lender will calculate is the Loan-to-Value (LTV) ratio. This figure helps the lender assess the level of risk they are taking on. In the commercial world, LTVs are generally lower than in residential lending, typically ranging from 65% to 75%.

Loan-to-Value (LTV) Ratio: A financial term used by lenders to express the ratio of a loan to the value of an asset purchased. Practical Application: LTV determines how much "skin in the game" you need to have. If a lender requires a 75% LTV on a $2,000,000 property, you must provide a $500,000 down payment.

LTV Calculation Example

Let’s look at a real-world scenario for an investor in Illinois:

- Property Value: $2,000,000

- Loan Amount requested: $1,500,000

- The Math: ($1,500,000 ÷ $2,000,000) = 0.75

- LTV Percentage: 75%

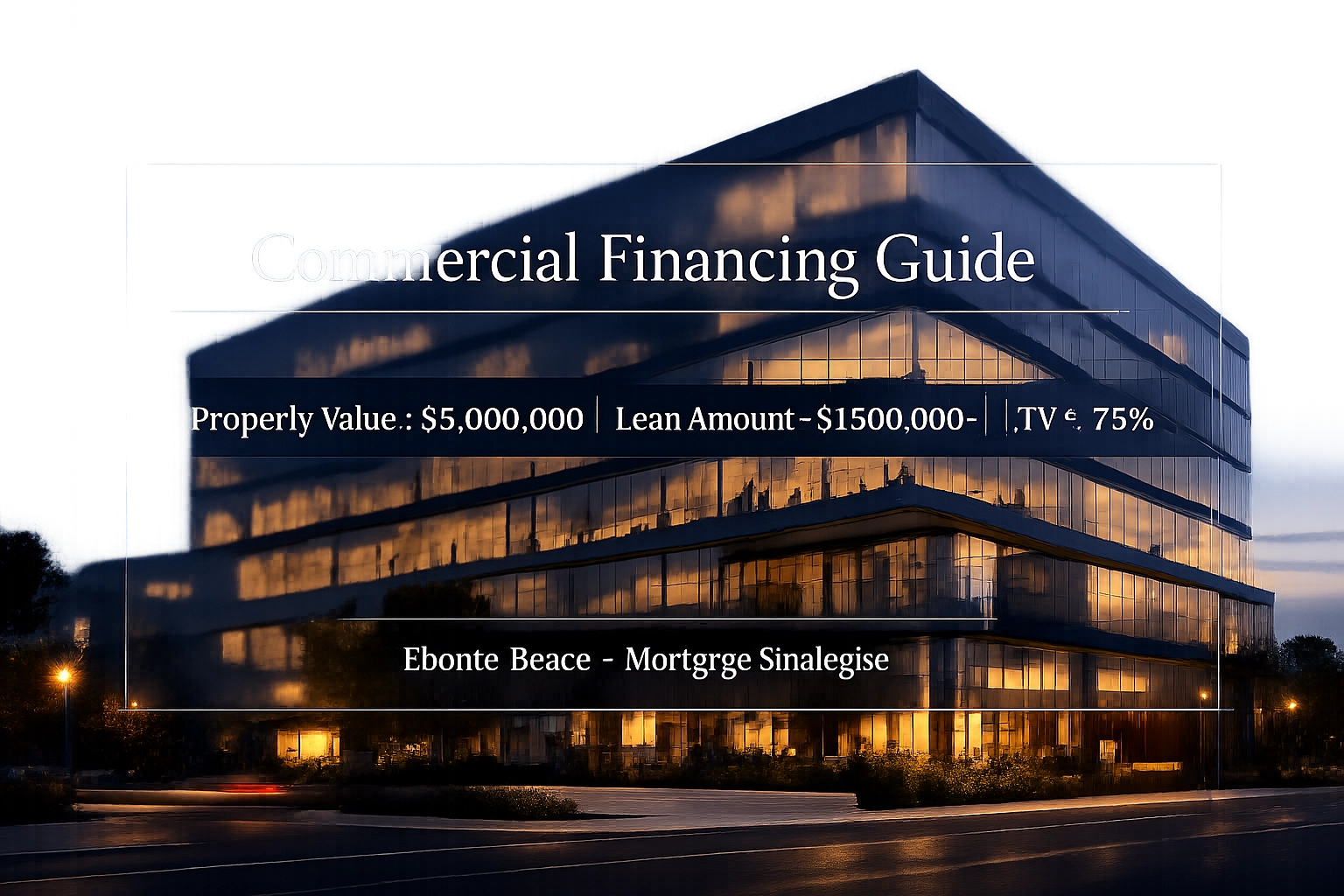

Title: Commercial Financing Guide

Calculation: Property Value $2,000,000 | Loan Amount $1,500,000 | LTV = 75%

Ebonie Beaco - Mortgage Loan Officer

Title: Commercial Financing Guide

Calculation: Property Value $2,000,000 | Loan Amount $1,500,000 | LTV = 75%

Ebonie Beaco - Mortgage Loan Officer

DSCR: The Key to Approval

While LTV measures the asset's value, the Debt Service Coverage Ratio (DSCR) measures the asset's ability to pay the mortgage. This is arguably the most vital metric in commercial lending.

Debt Service Coverage Ratio (DSCR): A measurement of a property's available cash flow to pay its current debt obligations. Practical Application: Lenders typically want to see a DSCR of 1.25 or higher. This means the property generates 25% more income than is required to pay the mortgage, providing a safety net for vacancies or repairs.

If you are looking at a multi-family property in Indiana, you can use the Home Loans Network Mortgage Calculators to start running your own preliminary numbers.

Bridge Loans and Hard Money

Sometimes, a property isn't ready for a traditional bank loan. It might need renovations, or you might need to close the deal faster than a bank can move. This is where bridge and hard money loans come into play.

Bridge Loan: A short-term loan used until a person or company secures permanent financing or removes an existing obligation. Practical Application: You find a distressed office building in Florida. You use a bridge loan to buy and renovate it, then "bridge" over to a traditional loan once the building is stabilized.

Hard Money Loan: An asset-based loan where a borrower receives funds secured by real property, typically issued by private investors or companies. Practical Application: Hard money is often used by fix-and-flip investors who need to close a deal in days rather than weeks.

These options carry higher interest rates but offer the speed and flexibility that traditional institutions lack.

Exploring Regional Opportunities

The commercial landscape varies significantly across the states we serve. In cities like Chicago, the focus might be on mixed-use developments and retail. In Florida and California, the demand for multi-family housing continues to drive high-leverage financing requests.

Investors in Arkansas and Alabama often find success in smaller-scale commercial properties, such as self-storage units or small industrial parks. Regardless of the location, having a clear understanding of the local market trends is a prerequisite for securing favorable loan terms. You can find more details about our regional focus on the About Us page.

The Commercial Loan Process

Navigating the application process requires organization and patience. Unlike a residential loan that might close in 30 days, commercial deals often take 60 to 90 days.

- Initial Review: You submit the property’s "trailing twelve" (T12) profit and loss statement and current rent roll.

- Letter of Intent (LOI): The lender provides a non-binding document outlining the proposed terms.

- Underwriting: The lender performs a deep dive into the property’s financials, your experience, and the local market data.

- Appraisal and Environmental Reports: Third-party experts verify the value and ensure there are no environmental hazards (like soil contamination).

- Closing: Final documents are signed, and funds are disbursed.

For a smoother experience, many investors review our Loan Process guide to understand the general flow of mortgage operations.

Why Work With a Mortgage Strategist?

The complexities of commercial lending mean that a "one size fits all" approach rarely works. A Mortgage Strategist understands how to position your deal to the right lender. Whether it is highlighting the upside of a vacant building in Virginia or navigating the strict requirements of a CMBS loan for a Missouri hotel, professional guidance is invaluable.

We focus on helping you compare options objectively. Instead of just looking at the interest rate, we look at the loan's impact on your long-term cash flow and scalability. If you have questions about specific scenarios, our FAQ page offers answers to common investor concerns.

Final Thoughts for Commercial Investors

Commercial real estate remains one of the most powerful vehicles for wealth creation. By leveraging the right debt structures, you can acquire assets that provide stable income and long-term appreciation. Whether you are a seasoned landlord or an individual looking to buy your first commercial property, understanding the tools at your disposal is the first step toward a successful transaction.

Financing commercial property? Contact Ebonie Beaco at Home Loans Network.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664