Commercial Real Estate Loans

Commercial real estate loans are the fuel for scaling your portfolio beyond simple residential flips. Whether you are eyeing a 12 unit apartment complex in Chicago or a retail strip in Florida, understanding your funding options is essential. We break down the differences between traditional bank debt, SBA programs, and private capital so you can move with confidence. At Home Loans Network, transparency is our foundation. We provide the technical insight you need to navigate high stakes transitions without the typical industry gatekeeping. Ready to expand your footprint? Explore our specialized commercial programs and see how the right leverage changes your trajectory. Jump in to find the perfect fit for your next big acquisition.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Navigating the World of Commercial Property Finance

Moving from residential properties to commercial real estate is a significant step for any investor or business owner.

The transition involves different rules, different math, and a different approach to risk.

Commercial real estate loans are mortgages used to purchase, refinance, or renovate properties specifically used for business purposes or income generation.

Unlike a standard home loan, these loans focus heavily on the income the property generates rather than just your personal bank account balance.

If you are looking to acquire an office building in Virginia or an industrial warehouse in Michigan, you need to know how lenders view these assets.

Explore the various pathways available at Home Loans Network to see which strategy fits your current goals.

Defining the Core Terms

Before we dive into the programs, let's establish a clear baseline for the terminology you will encounter.

Commercial Mortgage: A debt instrument secured by a lien on a commercial property rather than residential real estate.

This allows you to acquire high value assets that produce consistent business or rental income.

LTV (Loan to Value): The ratio of the loan amount compared to the appraised value of the property.

Lenders use this to determine how much equity you must bring to the closing table.

DSCR (Debt Service Coverage Ratio): A calculation that compares a property's net operating income to its debt obligations.

This tells the lender if the property earns enough to pay its own mortgage.

Amortization: The schedule of typical monthly payments over a set period.

Commercial loans often have shorter terms than the amortization period, leading to a balloon payment.

Access our mortgage basics page for more foundational definitions that simplify the lending process.

The Most Common Commercial Loan Programs

Every project has a specific financial requirement.

Lenders offer different structures based on whether you are an owner occupant or a pure investor.

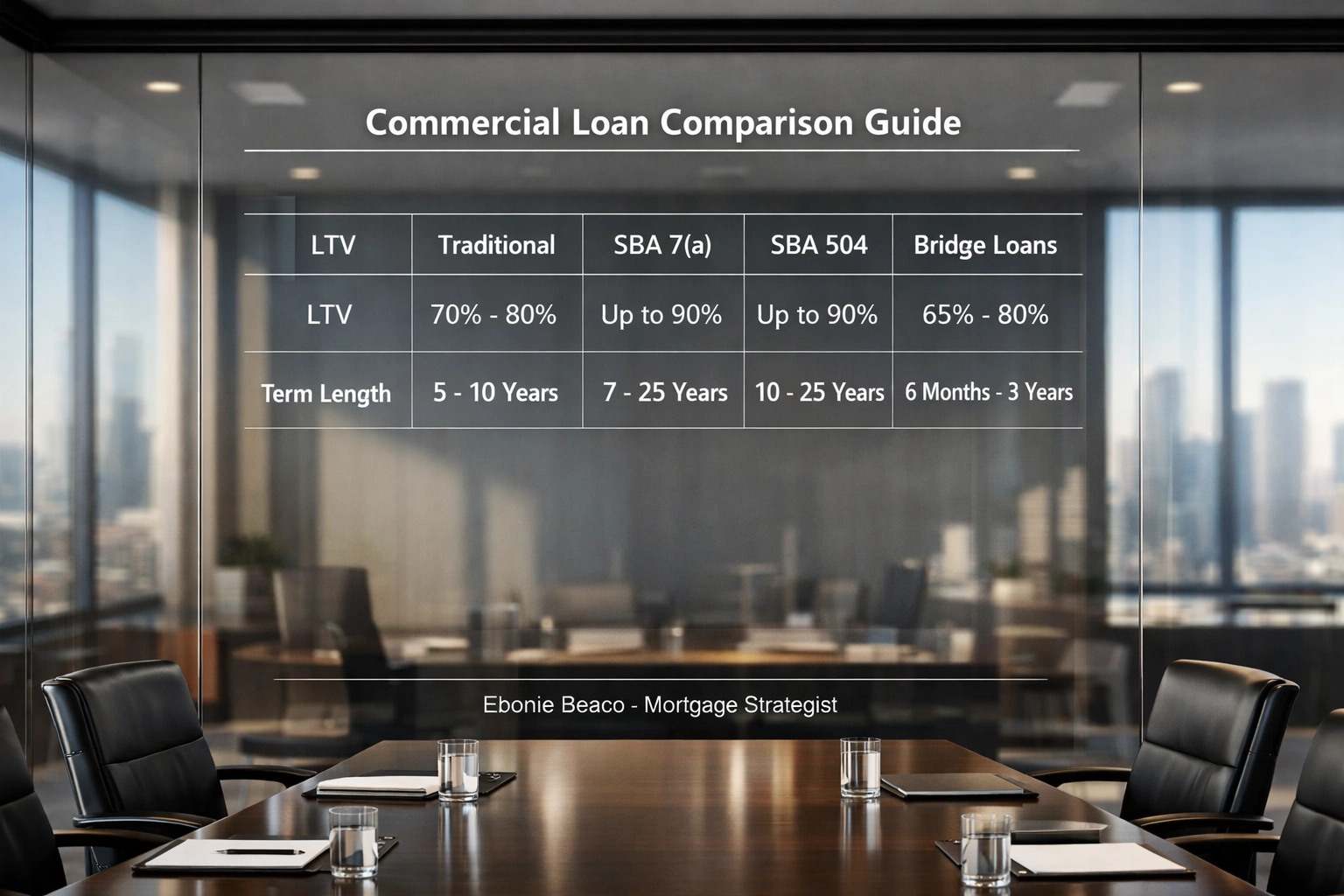

Traditional Commercial Loans

These are often provided by conventional banks and are best for "stabilized" properties.

Stabilized means the property is currently occupied and generating steady cash flow.

Traditional Loan: A fixed or variable rate mortgage with terms usually ranging from 5 to 20 years.

It offers some of the lowest interest rates for borrowers with strong credit and high equity.

SBA 7(a) Loans

The Small Business Administration (SBA) provides guarantees to lenders to encourage small business growth.

SBA 7(a): A government backed loan for business owners who plan to occupy at least 51 percent of the property.

This program offers high leverage, often up to 90 percent LTV, making it easier to keep cash in your business.

SBA 504 Loans

This is a specialized program designed for major fixed assets like land and buildings.

SBA 504: A loan structure involving a bank, a Certified Development Company, and the borrower.

It provides long term, fixed rate financing that is ideal for heavy industrial or large retail acquisitions.

Bridge Loans

Sometimes you need capital fast to close a deal before permanent financing is ready.

Bridge Loan: A short term financing solution used to cover the gap between immediate needs and long term goals.

Investors use these to acquire "value add" properties in markets like California or Florida that require quick action.

Learn more about our bridge loans and how they function as a temporary solution.

Visual: A comparison table of Commercial Loan Types. Columns: Loan Type, Typical LTV, Term Length, Best Use. Footer: Ebonie Beaco - Mortgage Strategist. Title: Commercial Loan Comparison Guide.

Financing Multi-Family and Apartment Buildings

Many investors start their commercial journey with apartment buildings.

If a property has 5 or more units, it is classified as commercial real estate.

In markets like Chicago or Atlanta, multi-family assets are highly sought after for their stability.

Multi-Family Financing: Specialized loans for residential buildings with 5 or more units.

These programs often offer more favorable terms because housing is considered a lower risk asset class.

When evaluating these deals, the DSCR is the primary metric.

Lenders generally look for a ratio of 1.25 or higher to feel comfortable with the risk.

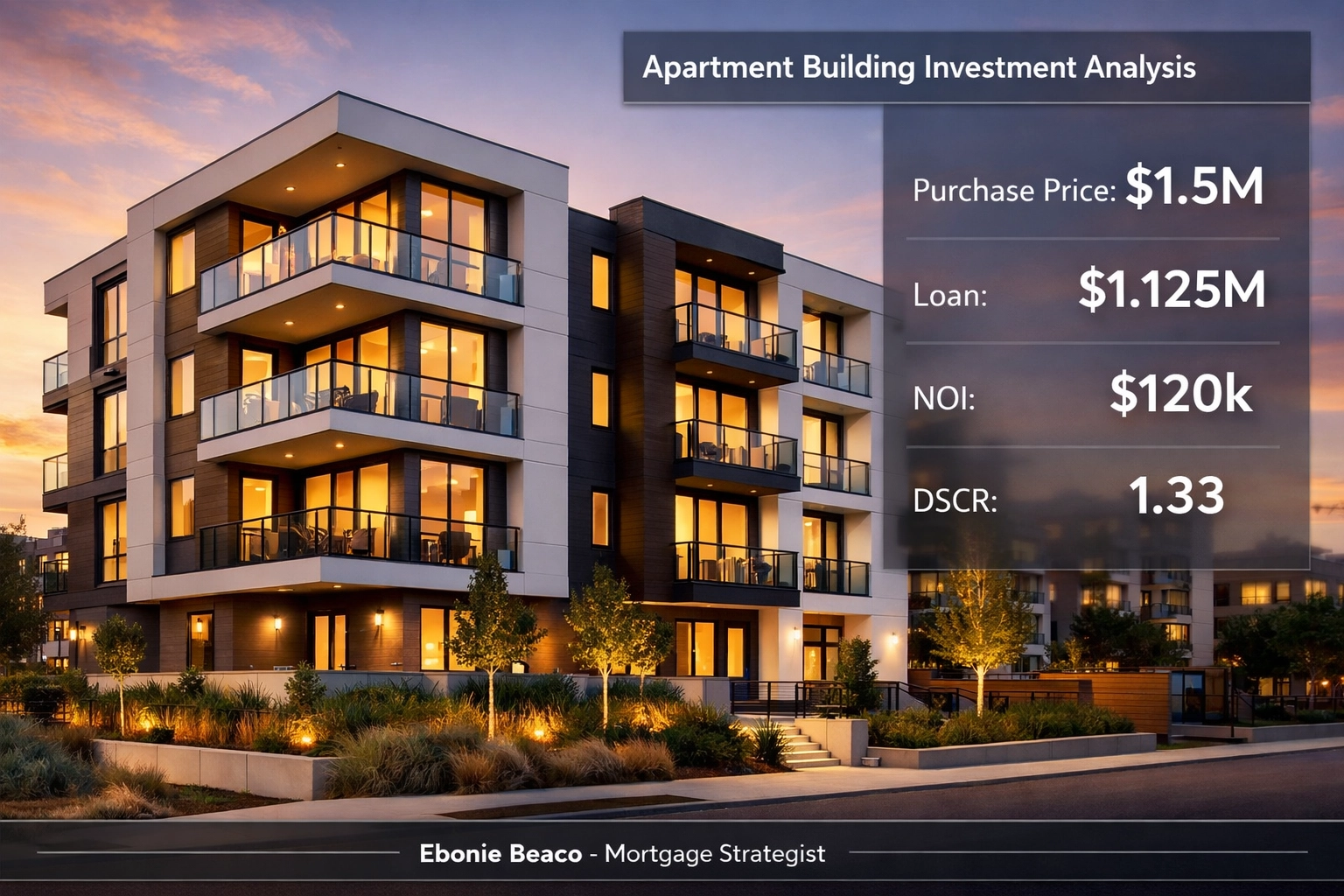

The Math Behind a 12-Unit Apartment Acquisition

Let's look at a practical example of how the numbers work in a real world transaction.

Imagine you are purchasing a 12 unit apartment building in an emerging neighborhood in Indiana.

Purchase Price: $1,500,000

Down Payment (25 percent): $375,000

Loan Amount: $1,125,000

Annual Rental Income: $180,000

Annual Expenses (Taxes, Insurance, Utilities): $60,000

Net Operating Income (NOI): $120,000

Annual Mortgage Payments: $90,000

DSCR Calculation: $120,000 (NOI) / $90,000 (Debt Service) = 1.33

Because the ratio is above 1.25, this deal is likely to qualify for standard commercial financing.

This calculation shows that the property generates 33 percent more income than the cost of the mortgage.

Visual: A deal breakdown graphic for a 12-unit apartment. Shows Purchase Price $1.5M, Loan $1.125M, NOI $120k, Debt Service $90k, and the final DSCR of 1.33. Footer: Ebonie Beaco - Mortgage Strategist. Title: Apartment Building Investment Analysis.

Mixed-Use and Special Purpose Properties

Not every commercial building is just an office or an apartment.

Mixed-use properties are very popular in urban centers like those in Virginia and Florida.

Mixed-Use Loan: Financing for properties that combine residential units with commercial retail or office space.

This allows you to diversify your income streams within a single physical asset.

These deals can be more complex because the lender has to evaluate two different types of tenants.

The retail tenant on the ground floor carries a different risk profile than the apartment renters above.

We can help you compare options for these hybrid properties to ensure you get the best leverage.

Hard Money and Private Capital for Commercial Deals

If a property is in poor condition or "distressed," traditional banks will often decline the loan.

This is where private money comes into play.

Hard Money Loan: An asset based loan where the property value is the primary security for the debt.

This provides the speed and flexibility needed to secure distressed assets in competitive markets.

Hard money is typically used for "fix and flip" commercial projects.

You might buy an old warehouse in Arkansas, renovate it into a modern creative studio space, and then refinance into a permanent loan once the building is occupied.

Explore our fix and flip financing to see how private capital can jumpstart your project.

Why the Location of Your Project is Vital

The state and city where you buy affect your financing options significantly.

Lenders look at "market saturation" and local economic trends.

In Florida, there is high demand for short term rental commercial units and hospitality assets.

In Illinois, particularly Chicago, the focus is often on high density multi-family and industrial logistics centers.

California and Virginia see significant activity in office and mixed-use developments due to the tech and government sectors.

We provide insights across Alabama, Arkansas, Kentucky, Michigan, and Missouri to help you understand the local lending landscape.

How to Prepare for the Commercial Loan Process

Applying for a commercial loan is a document intensive process.

You should be prepared to provide more than just your personal tax returns.

- Rent Rolls: A detailed list of all tenants, their lease terms, and their payment history.

- Profit and Loss (P&L): A two year history of the property's income and expenses.

- Personal Financial Statement: A snapshot of your own assets and liabilities.

- Experience Resume: A summary of your previous real estate or business management history.

Lenders want to see that you have a plan for the property and the capability to execute it.

The loan process is smoother when you have these documents organized from day one.

Final Thoughts on Scaling with Commercial Debt

Commercial real estate loans are a powerful tool for building long term wealth.

They allow you to control larger assets and benefit from professional tenant leases.

Whether you are a seasoned investor or a business owner looking to stop paying rent, the right financing strategy is the key to your success.

Avoid the confusion of the retail banking world and work with a strategist who understands the nuances of the commercial market.

Compare your current scenarios with our mortgage calculators to see how different rates and terms impact your cash flow.

Ready to discuss your next commercial acquisition?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664