Closing Bell Update: How Today’s Treasury Yield Shift Impacts Your Mortgage Rate

As the final trades settle and the closing bell rings, the shift in Treasury yields often dictates the financial landscape for the following morning. For homeowners, real estate investors, and industry professionals across states like Florida, Illinois, and California, these daily movements are far more than just abstract numbers on a screen. They represent the primary benchmark for pricing mortgage products, from traditional home loans to specialized investor financing. Understanding the connection between the bond market and your monthly payment is a fundamental step in making informed real estate decisions.

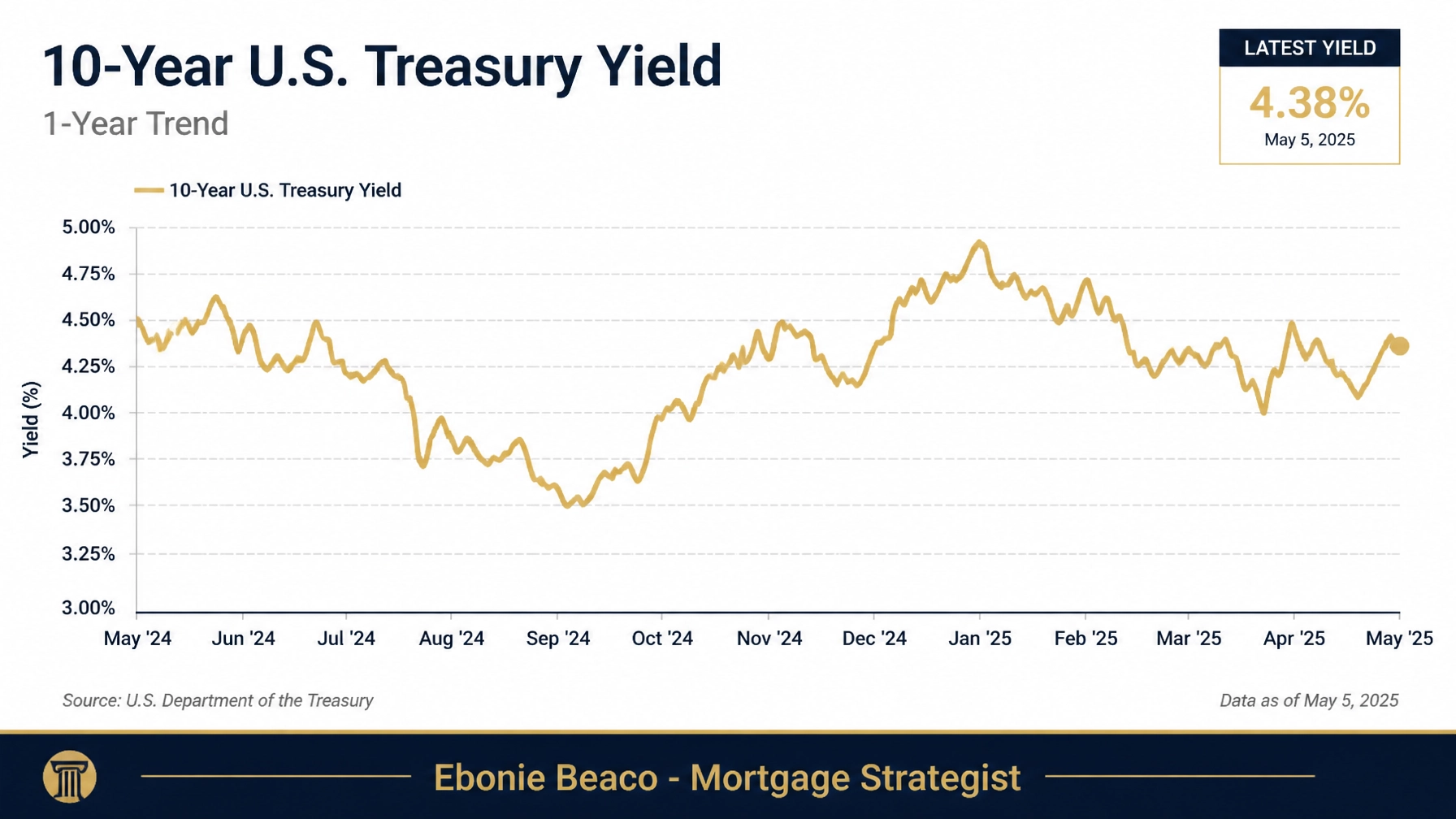

The 10-Year U.S. Treasury yield serves as the anchor for the long-term mortgage market. When investors buy or sell these government bonds based on inflation data or Federal Reserve updates, the yields fluctuate in real time. Because mortgage-backed securities (MBS) compete for the same investor capital as Treasuries, lenders must adjust their interest rates to remain competitive and manage risk. Today’s shift in the yield curve provides a clear window into where financing costs are headed for the remainder of the week.

The Direct Correlation Between Treasury Yields and Mortgage Rates

Explore the relationship between government debt and your personal financing costs by looking at the 10-Year Treasury yield. This specific bond is the most significant indicator for the 30-year fixed mortgage rate because it shares a similar expected duration. While the Federal Reserve sets short-term overnight rates, the 10-Year yield reflects the market's long-term outlook on inflation and economic growth. When yields rise, mortgage rates typically follow suit within hours or days.

Treasury Yield: The interest rate that the U.S. government pays to borrow money for a specific period. This figure acts as the "risk-free" rate that all other lending products use as a baseline for pricing.

Spread: The difference between the 10-Year Treasury yield and the average 30-year fixed mortgage rate. This gap covers the costs of mortgage servicing, credit risk, and prepayment variables that are not present in government bonds.

Historically, the spread between the 10-Year Treasury and the average mortgage rate has stayed around 1.7 to 2.0 percentage points. However, in recent volatile markets, this spread has widened significantly, sometimes exceeding 3.0 percentage points. You can track these movements through resources like the Federal Reserve Economic Data (FRED) to see how today’s closing figures compare to historical norms. When the spread narrows, it can lead to lower rates for borrowers even if Treasury yields stay relatively flat.

Today’s Market Movement and Economic Indicators

Analyze the current economic data to understand why yields moved during today's session. Key reports such as the Consumer Price Index (CPI) and employment data often trigger rapid buying or selling in the bond market. If the data suggests that inflation is cooling, investors often flock to bonds, which pushes yields down and creates a more favorable environment for a home refinance. Conversely, strong economic growth can lead to higher yields as the market anticipates higher interest rates for longer periods.

Market activity in mid-2026 continues to react to the Federal Reserve’s ongoing efforts to balance growth with price stability. For those monitoring properties in high-growth markets like Georgia or Virginia, these daily fluctuations can mean the difference of several hundred dollars in a monthly mortgage payment. Staying informed about the closing bell results allows you to time your rate lock more effectively. Access our mortgage basics guide to learn more about how global economic news reaches your local lending office.

Regional Insights: Real Estate in Florida, Illinois, and California

Real estate trends vary significantly by geography, but the impact of Treasury yields is felt universally across all primary markets. In Florida, where the demand for short-term rentals and luxury condos remains high, investors are particularly sensitive to rate shifts. Higher yields can increase the cost of DSCR investor loans, which rely on the property’s cash flow to qualify. If the interest rate rises, the Debt Service Coverage Ratio (DSCR) might tighten, requiring a larger down payment to make the deal viable.

In the Chicago market and throughout Illinois, many homeowners are looking toward home equity as a way to fund renovations or consolidate high-interest debt. When Treasury yields dip, it often opens a window for conventional loans with lower interest rates. Similarly, in California’s competitive housing market, a small shift in yields can impact a buyer's purchasing power by tens of thousands of dollars. Whether you are in Alabama or Missouri, the national bond market sets the stage for your local transaction.

Strategies for Homeowners: Refinancing and HELOCs

Jump in and evaluate your current mortgage terms against today’s market conditions. If you currently hold a high-interest mortgage from a period of peak volatility, today’s yield shift might indicate an opportunity to lower your rate. A rate-term refinance can reduce your monthly obligation, while a cash-out refinance allows you to extract liquid capital for investment or personal use. Many homeowners in Virginia and Indiana are using these strategies to pivot from high-cost debt into more manageable mortgage structures.

For those who do not want to touch their primary low-rate mortgage, a HELOC (Home Equity Line of Credit) offers a flexible alternative. Unlike fixed-rate mortgages, HELOCs are often tied to the Prime Rate, which is influenced by the Federal Reserve’s short-term moves rather than just the 10-Year yield. Compare these options carefully to ensure you are selecting the most efficient path for your financial profile. Explore our mortgage calculators to run these scenarios yourself and see how different rates impact your bottom line.

Strategy for Investors: DSCR and Portfolio Growth

Real estate investors focus on yield and cash flow, making the "closing bell" results a critical part of their daily routine. For landlords managing multi-family properties in Michigan or Kentucky, DSCR rental property loans provide a streamlined way to acquire new assets without the need for traditional income verification. These loans are priced based on market risk, which is directly influenced by Treasury movements. When yields decrease, the profitability of a new rental acquisition often increases.

Landlord Loans: Financing specifically designed for owners of rental properties, often focusing on the income potential of the asset rather than the personal debt-to-income ratio of the borrower.

Fix and Flip Financing: Short-term bridge loans used by investors to purchase and renovate distressed properties with the intent of selling them for a profit quickly.

Portfolio investors in Arkansas and Alabama often utilize bridge loans to close deals quickly before transitioning into long-term financing when yields are more favorable. By understanding the daily shifts in the bond market, you can better predict when to shift from short-term "hard money" into permanent fixed-rate debt. This proactive approach is essential for scaling a real estate business in a shifting interest rate environment.

Example Scenario: Impact on a $500,000 Equity Strategy

To see how these numbers translate into a real-world scenario, consider a homeowner with a primary residence valued at $500,000. By analyzing the available equity, this owner can determine their potential for reinvestment into other assets. The following table illustrates a typical cash-out refinance scenario based on current market guidelines.

In this example, the homeowner has an existing mortgage balance of $300,000. Following standard industry guidelines of an 80% maximum Loan-to-Value (LTV) ratio, the total loan amount allowed is $400,000. After paying off the original $300,000 mortgage, the homeowner is left with $100,000 in available funds. These funds can be used for a down payment on a new rental property, a renovation of the existing home, or as a cash reserve for future investment opportunities.

A 0.50% shift in the interest rate on that $400,000 loan can change the monthly interest payment by approximately $166. Over a 30-year term, that seemingly small difference in today’s closing yields could cost or save you nearly $60,000 in total interest. This is why tracking the bond market is not just for Wall Street traders: it is for every property owner looking to protect their wealth.

Navigating the Market in 2026

The real estate market in 2026 requires a more strategic approach than in previous years. With a wide range of products available, including non-QM mortgage loans and bank statement loans for the self-employed, borrowers have more flexibility than ever before. These programs often have different pricing structures compared to conventional loans, but they still feel the ripple effects of Treasury yield changes. If you are an entrepreneur in California or a small business owner in Illinois, your financing options are directly linked to these global trends.

Collaboration between buyers, realtors, and mortgage strategists is the most effective way to navigate these shifts. When a realtor understands how a 10-year yield movement affects their client's qualification, they can better structure offers and manage expectations. Access the loan process details to see how we guide you from the initial scenario analysis to the final closing.

Actionable Steps for Borrowers Today

Stay ahead of the market by taking proactive steps as soon as you see a favorable shift in yields. If today's closing bell showed a decline in the 10-Year Treasury, it may be the ideal time to initiate a conversation about a new loan. Review your credit profile and gather your documentation so you are ready to lock in a rate when the window of opportunity opens. Markets move fast, and those who are prepared often secure the best terms.

Explore your options and resolve your uncertainty today.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664