Chicago Real Estate Secrets Revealed: What Experts Don't Want You to Know About June Rate Trends

As we enter the heart of the summer market in June 2026, many prospective homebuyers and seasoned investors in Chicago are searching for a clear signal in a complex financial landscape. While national headlines often focus on the broad strokes of economic shifts, the local reality for Illinois real estate requires a more nuanced perspective. The perceived secret among mortgage strategists is not a hidden, imminent crash in interest rates, but rather the emerging stability of the mid 6% range. Understanding how to navigate this plateau allows you to make informed decisions without the paralysis of waiting for a return to historical lows that may not arrive this season.

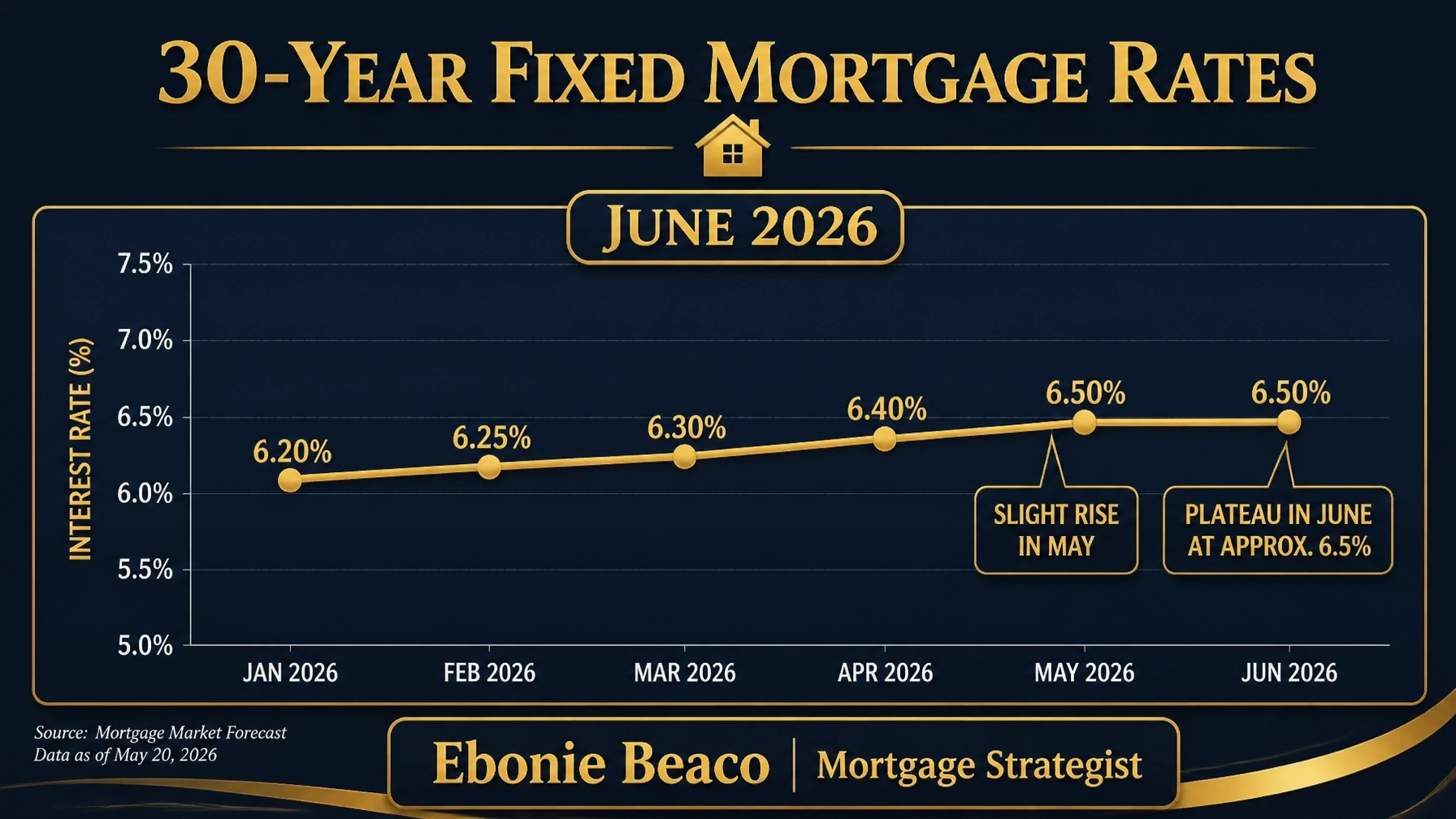

The Macro Landscape: Navigating National Mortgage Averages

Recent data from early June 2026 indicates that the 30 year fixed mortgage rate is averaging between 6.4% and 6.6% across the United States. This represents a slight increase from the previous month, driven largely by persistent inflation and a robust labor market that has caused the Federal Reserve to maintain a cautious stance. For borrowers in Alabama, Florida, and Virginia, these figures serve as a baseline for all residential financing discussions. While these rates are higher than the pandemic era lows, they are significantly lower than the peaks seen in late 2023, providing a window of opportunity for those with the right strategy.

30-Year Fixed Mortgage: A home loan with an interest rate that remains unchanged for the entire 30 year term of the debt. This product offers long term payment security and protection against future interest rate hikes.

15-Year Fixed Mortgage: A loan with a shorter duration and typically lower interest rates compared to the 30 year option. You can use this to build equity faster and reduce the total interest paid over the life of the financing.

Market forecasts from reputable sources like NerdWallet confirm that while rates are unlikely to drop below 6% in the immediate future, the current environment is characterized by relative predictability. This stability is a significant advantage for Chicago homebuyers who have been sidelined by the volatility of previous years. Rather than timing the market, experts are now focusing on loan structure and property selection to offset borrowing costs. Accessing professional guidance early in your search ensures you are prepared for these fluctuating conditions.

Federal Reserve Policy and the Inflation Factor

The Federal Reserve continues to play a pivotal role in shaping the mortgage environment through its management of the federal funds rate. Currently sitting between 3.5% and 3.75%, the benchmark rate reflects the Fed’s commitment to cooling inflation without triggering a recession. For real estate professionals and investors in Michigan and Georgia, this means that the "wait and see" approach often results in missed opportunities as property prices continue to experience modest growth. Inflation remains a primary driver of mortgage pricing, and current geopolitical factors have contributed to keeping these figures above the desired target.

Federal Funds Rate: The interest rate at which commercial banks borrow and lend their excess reserves to each other overnight. This rate influences the broader economy, including the interest rates you pay on mortgages and lines of credit.

Inflation: The rate at which the general level of prices for goods and services rises, subsequently eroding purchasing power. High inflation typically leads to higher mortgage rates as lenders seek to maintain their real rate of return.

The Chicago Context: Local Market Resilience

In Chicago and its surrounding suburbs, the real estate market is demonstrating remarkable resilience despite the national rate environment. Inventory remains tight as many current homeowners choose to stay in properties with existing low rate mortgages, a phenomenon known as the "lock-in effect." This scarcity of available homes keeps property values steady in neighborhoods like Lincoln Park, Logan Square, and the West Loop. For investors looking at multi-unit buildings, the demand for rental housing remains strong, providing a solid foundation for income-producing assets.

Strategic buyers are increasingly looking at Non-QM and bank statement loans to navigate these conditions. Self-employed entrepreneurs in Illinois find that traditional W-2 requirements often fail to reflect their true financial strength. By utilizing alternative documentation, you can secure financing that aligns with your specific income structure. Exploring these specialized programs is a key part of building a successful portfolio in a competitive metropolitan market.

Real Estate Investor Strategies: Leveraging DSCR Loans

For those focused on building wealth through rental properties, the Debt Service Coverage Ratio (DSCR) loan has become a primary tool in June 2026. This program allows you to qualify for financing based on the rental income generated by the property rather than your personal income or debt to income ratio. In a mid 6% rate environment, the ability to scale a portfolio without the limitations of traditional underwriting is vital. Investors in Indiana, Missouri, and Arkansas are using these loans to acquire everything from single family homes to short term rental properties.

DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its debt payments. You calculate this by dividing the net operating income by the total debt service to determine if the property generates enough cash flow.

LTV (Loan-to-Value): The ratio of a loan to the value of an asset purchased. Maintaining a lower LTV can help you secure more favorable interest rates and reduce the overall risk of your investment.

Investors often combine DSCR loans with the BRRRR (Buy, Rehab, Rent, Refinance, Repeat) strategy to maximize their capital. According to insights from Morgan Stanley, the path to lower rates later in the decade will likely be gradual. This suggests that acquiring assets now and refinancing when conditions improve is a more effective long term strategy than waiting for a market bottom. Jump in and compare current rental property scenarios to see how the numbers work for your specific goals.

Unlocking Equity: HELOC and Cash-Out Refinance Scenarios

Many homeowners in Chicago have seen significant appreciation in their property values over the last several years. Accessing this equity can provide the necessary funds for home renovations, debt consolidation, or the purchase of additional investment properties. Whether you choose a Home Equity Line of Credit (HELOC) or a cash-out refinance, the objective is to put your housing wealth to work. Even with current rates, the strategic extraction of equity can be a powerful financial move when the funds are reinvested into higher yielding assets.

Consider a scenario where a homeowner in a Chicago suburb owns a property valued at $650,000. With an existing mortgage balance of $380,000, they have substantial equity that can be utilized for further investment. By performing a cash-out refinance at an 80% LTV, they can access approximately $140,000 in liquid capital. This amount could serve as a down payment for a new rental property or fund a major renovation that further increases the primary residence's value.

HELOC (Home Equity Line of Credit): A revolving line of credit that uses your home as collateral. You can draw from this line as needed and only pay interest on the amount you actually use, providing maximum flexibility for ongoing projects.

Cash-Out Refinance: A new mortgage that replaces your existing one for a higher amount than you owe, allowing you to take the difference in cash. This is a common method for homeowners to consolidate high interest debt or fund large scale real estate acquisitions.

Expert Guidance for Your Next Move

The "secrets" of the June 2026 market are found in the details of loan structuring and local market knowledge. While the broader economic indicators suggest a period of high stability, your personal financial profile and goals determine the best path forward. Whether you are a first time homebuyer in Virginia or a veteran investor in California, the commitment to education and personal guidance remains the most important factor in your success. Navigate the current rate trends with confidence by focusing on long term wealth building rather than short term market noise.

Explore your options today and discover how these financing strategies can work for you. Every property transaction is an opportunity to strengthen your financial position, provided you have the right strategist by your side. Compare different loan programs and access the tools needed to analyze your next deal with precision.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664