Chicago DSCR Loan Secrets Revealed: What Experts Don't Want You to Know

SEO Title: Chicago DSCR Loan Secrets Revealed: Your Investor Guide

Meta Description: Discover the hidden strategies of Chicago DSCR loans. Learn how Cook County property taxes affect your borrowing power and how to qualify without personal income.

URL Slug: chicago-dscr-loan-secrets-revealed

Featured Image Recommendation: A professional landscape photo of the Chicago skyline at sunset with a financial dashboard overlay and the website URL prominently displayed.

SEO Alt Text: Chicago real estate investment property with DSCR loan calculation overlay and website URL.

Social Media Excerpt: Planning to invest in Chicago real estate? DSCR loans are the "secret" to scaling your portfolio without tax returns. But watch out for Cook County taxes! Here is what you need to know.

SEO Tags: Chicago DSCR Loans, Real Estate Investing Chicago, Landlord Loans, Cook County Property Taxes, DSCR Calculation, Mortgage Strategies.

Chicago real estate offers some of the most consistent opportunities for wealth building in the country. From the high-demand rentals in the West Loop to the classic multi-unit "two-flats" in Logan Square, the market is built for investors. However, traditional financing often slows down your growth. If you have been told your debt-to-income ratio is too high or your tax returns do not show enough income, you are likely looking at the wrong loan programs.

The "secret" many high-scale Chicago investors use is the Debt Service Coverage Ratio (DSCR) loan. This program bypasses the traditional red tape and focuses on what actually makes a deal work: the property itself.

What is a Chicago DSCR Loan?

Debt Service Coverage Ratio (DSCR): A financial metric used by lenders to measure a property's ability to cover its monthly mortgage payments using only its rental income.

Application: In Chicago, investors use this ratio to qualify for financing without providing personal W-2s, pay stubs, or tax returns.

Principal, Interest, Taxes, and Insurance (PITI): The four basic components of a monthly mortgage payment.

Application: Lenders compare your total PITI to the gross monthly rent to determine if the property qualifies for a DSCR loan.

Jump in and explore how these loans operate differently from traditional financing. Unlike a conventional loan that scrutinizes your personal lifestyle and spending, a DSCR loan treats your investment like a business. If the rent covers the mortgage, the deal is often a go.

Start a Free Trial to access our AI-powered deal analysis tools.

Secret 1: The "No-Doc" Reality for Self-Employed Borrowers

Many entrepreneurs and self-employed investors in Chicago struggle to get conventional loans. This happens because high-quality CPAs often find legal ways to reduce taxable income, which inadvertently lowers your borrowing power.

DSCR loans solve this. Lenders do not look at your personal tax returns. They do not care about your DTI (Debt-to-Income) ratio. Instead, they focus on the property's income potential. This allows you to scale your portfolio as fast as you can find profitable deals, rather than waiting for your tax returns to catch up.

Secret 2: Navigating the Cook County Property Tax Trap

While DSCR loans are powerful, Chicago investors must be wary of the "Cook County Tax Trap." Property taxes in Cook County are notoriously high and can fluctuate significantly. Because taxes are a part of the PITI calculation, a sudden jump in property taxes can lower your DSCR ratio and reduce your maximum loan amount.

Compare the tax rates in different Chicago neighborhoods before you commit. For example, a property in a high-tax ward might require a much higher rent to achieve the same 1.20 DSCR as a similar property in a more tax-friendly area.

Access our AI Market Analysis to see neighborhood-specific data.

Secret 3: Using STR and Airbnb Income to Qualify

Experts often keep quiet about how they use Short-Term Rental (STR) income to qualify for DSCR loans. In popular Chicago tourist areas like River North or near Wrigley Field, Airbnb income can be double or triple what long-term market rents would be.

Some DSCR lenders will allow you to use "short-term rental projections" (often from tools like AirDNA) to qualify for the loan. This means a property that might fail a standard rental check could pass with flying colors as a vacation rental, unlocking higher leverage and better terms.

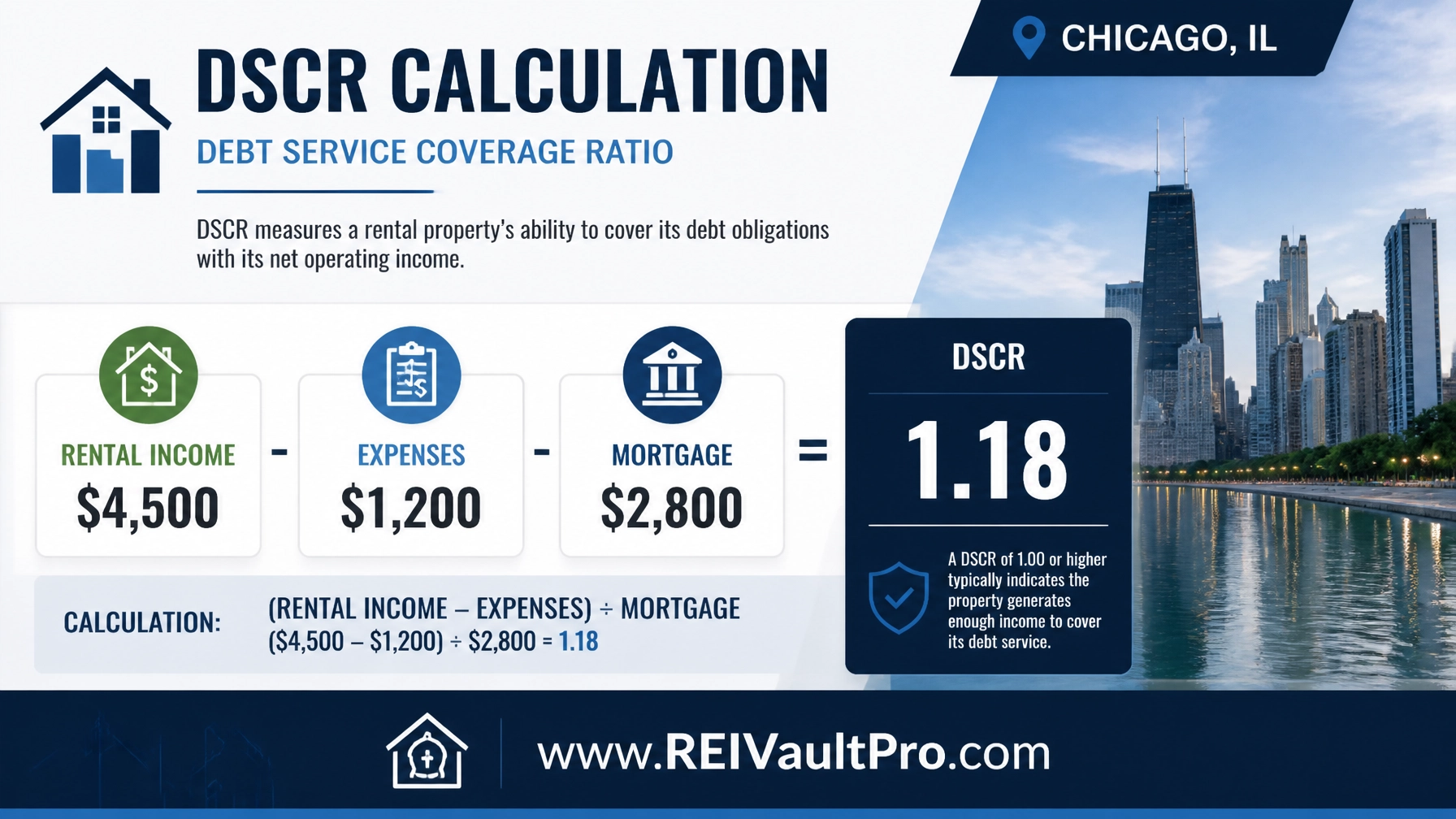

The Math: A Real Chicago DSCR Example

To understand how this works in the real world, let's look at a typical Chicago 2-unit building purchase.

- Purchase Price: $500,000

- Down Payment (20%): $100,000

- Loan Amount: $400,000

- Monthly Gross Rent (Total): $4,800

- Monthly PITI (Mortgage, Taxes, Insurance): $3,600

To find the DSCR, you divide the income by the debt service:

$4,800 / $3,600 = 1.33 DSCR

A 1.33 DSCR is considered a very strong deal. Most lenders look for a 1.20 or 1.25. If the ratio is above 1.0, the property is "cash flow positive" in the eyes of the bank. If it falls below 1.0, you may still qualify, but you might need a larger down payment or a slightly higher interest rate.

Use our DSCR Calculator to run your own numbers.

Comparing Conventional vs. DSCR Loans

| Feature | Conventional Investor Loan | Chicago DSCR Loan |

|---|---|---|

| Income Verification | Full Tax Returns & W-2s | No Personal Income Required |

| Debt-to-Income (DTI) | Limits your personal debt | DTI is not calculated |

| Loan Limits | Restricted by Fannie/Freddie | Often no limit on total loans |

| Speed to Close | 30-45 Days | 21-30 Days |

| Property Type | Strict (Residential) | Flexible (STR, Multi-family, LLC) |

Why LLC Vesting is a Game Changer

In Chicago, savvy investors rarely close in their personal names. Closing in an LLC provides a layer of asset protection and privacy. Conventional lenders often make it difficult to close in an LLC, but DSCR loans are designed for it.

Closing in an entity allows you to keep your personal credit report cleaner and protects your personal assets from property-related liabilities. It also makes it easier to bring on partners for larger deals in the future.

Strategies for the Chicago Market

Explore these common strategies used by local pros:

- The BRRRR Method: Buy, Rehab, Rent, Refinance, Repeat. Use a Bridge Loan or Hard Money to buy and fix, then refinance into a long-term DSCR loan once the property is leased and the value is up.

- House Hacking Refi: If you live in one unit of a 4-unit building, you can eventually move out and refinance the entire building into a DSCR loan to free up your personal DTI for your next home purchase.

- Portfolio Consolidation: If you have several properties with high-interest debt, you can use a DSCR loan to wrap them into a single portfolio loan, simplifying your monthly payments.

Watch a Demo to see how we track these strategies.

Related REI Vault Pro Resources

- AI Deal Analyzer: This tool helps you quickly calculate the DSCR and potential ROI for any Chicago property. It allows you to see if a deal is worth pursuing before you even talk to a lender.

- AI Rent Analyzer: Crucial for DSCR qualifying, this resource pulls real-time rental data for specific Chicago zip codes to ensure your income projections are accurate.

- AI Rehab Estimator: If you are doing a BRRRR deal, use this to estimate renovation costs. Accurate estimates prevent you from over-leveraging and hurting your final DSCR ratio.

- AI Market Analysis: Stay ahead of Cook County property tax trends and neighborhood shifts with deep-dive market insights.

Conclusion

Chicago DSCR loans are not just for the elite. They are a practical tool for anyone looking to build a real estate empire without the constraints of traditional banking. By focusing on property performance and understanding the nuances of the local tax landscape, you can scale your portfolio faster and with more confidence.

Join REI Vault Pro today to access the full suite of investment tools.

FAQ Section

How much down payment do I need for a Chicago DSCR loan?

Most programs require a 20% to 25% down payment. However, if you have a high credit score and the property has an excellent DSCR (1.50+), some lenders may allow for as little as 15% down.

Can I get a DSCR loan for a 10-unit apartment building in Chicago?

Yes. While many DSCR loans focus on 1-4 unit residential properties, there are commercial DSCR programs specifically for larger multi-family buildings and apartment complexes.

Does my personal credit score still count?

Yes. While the lender does not look at your income, they will check your credit score. Higher scores (typically 720+) will net you the best interest rates and higher leverage (LTV).

Are interest rates higher for DSCR loans?

Generally, yes. Because these loans carry more risk for the lender (due to no income verification), the interest rates are typically 1% to 2% higher than a conventional owner-occupied loan.

Can I use a DSCR loan to buy a fix-and-flip?

Usually, no. DSCR loans are designed for "buy and hold" properties that are already tenant-occupied or ready to be rented. For a property in need of major repairs, a Fix and Flip Loan or Bridge Loan is more appropriate.