Chicago DSCR Loan Lender: How to Scale Your Portfolio Without Personal Income Verification

SEO Title: Chicago DSCR Loan Lender: Scale Your Portfolio Without Income Verification

Meta Description: Learn how to scale your Chicago real estate portfolio using DSCR loans. Access financing based on property cash flow without personal income verification or tax returns.

URL Slug: chicago-dscr-loan-lender-scale-real-estate-portfolio

Featured Image Recommendation: A landscape photograph of the Chicago skyline with professional residential rental properties in the foreground, including the brand website URL "www.REIVaultPro.com".

SEO Alt Text: Chicago skyline with residential rental properties representing DSCR loan opportunities for real estate investors.

Social Media Excerpt: Ready to scale your real estate portfolio in Chicago? Discover how DSCR loans allow you to qualify based on property rental income rather than personal tax returns. Scale faster and build wealth through real estate financing.

SEO Tags: Chicago DSCR Loans, Real Estate Investing Chicago, Landlord Loans, Scale Real Estate Portfolio, No Income Verification Mortgage, DSCR Calculation, Illinois Investment Property Loans

Scaling a real estate portfolio in a competitive market like Chicago requires access to efficient capital that does not rely on your personal debt-to-income ratio. Traditional mortgage programs often present hurdles for ambitious investors, particularly those who are self-employed or already hold multiple properties.

Explore how the Debt Service Coverage Ratio (DSCR) loan serves as a powerful tool for acquisition and refinancing. By shifting the focus from your personal tax returns to the cash-generating potential of the property, you can bypass the restrictive documentation of conventional lending.

Understanding the DSCR Loan Framework

A DSCR Loan is a type of non-QM (non-qualified mortgage) financing designed for real estate investors where qualification is based on the property’s ability to cover its own debt.

Debt Service Coverage Ratio (DSCR): A financial metric used to measure a property's ability to cover its monthly mortgage payments using its gross rental income.

Application: Investors use this ratio to qualify for loans without showing personal pay stubs or W-2 income.

Jump in to the core components that make this program a favorite for Chicago landlords and investors across Illinois, Indiana, and Michigan. Unlike traditional loans that scrutinize your personal income, a DSCR lender focuses on the PITIA (Principal, Interest, Taxes, Insurance, and HOA dues) versus the Gross Monthly Rent.

Why Chicago Investors Use DSCR Financing

Chicago is a city of neighborhoods, from the multi-unit buildings in Logan Square to the growing rental markets in South Shore and Rogers Park. Each property offers unique cash flow potential.

Eliminate Personal Income Roadblocks

Many high-volume investors and self-employed entrepreneurs find that their tax returns do not accurately reflect their ability to repay a loan due to legal deductions and business expenses. Access financing that ignores your personal DTI (Debt-to-Income) and instead analyzes the asset you are purchasing.

Accelerate Portfolio Growth

Because these loans do not count against your personal borrowing limits in the same way conventional loans do, you can theoretically hold an unlimited number of DSCR loans. This allows you to scale from a single duplex to a sprawling portfolio of 20+ units across Chicago and other states like Florida, Georgia, and Virginia.

Streamlined Documentation

The approval process for a Chicago DSCR loan is significantly faster than a traditional bank loan. You won't be asked for years of tax returns or complex business P&L statements. Focus on the appraisal and the lease agreements instead.

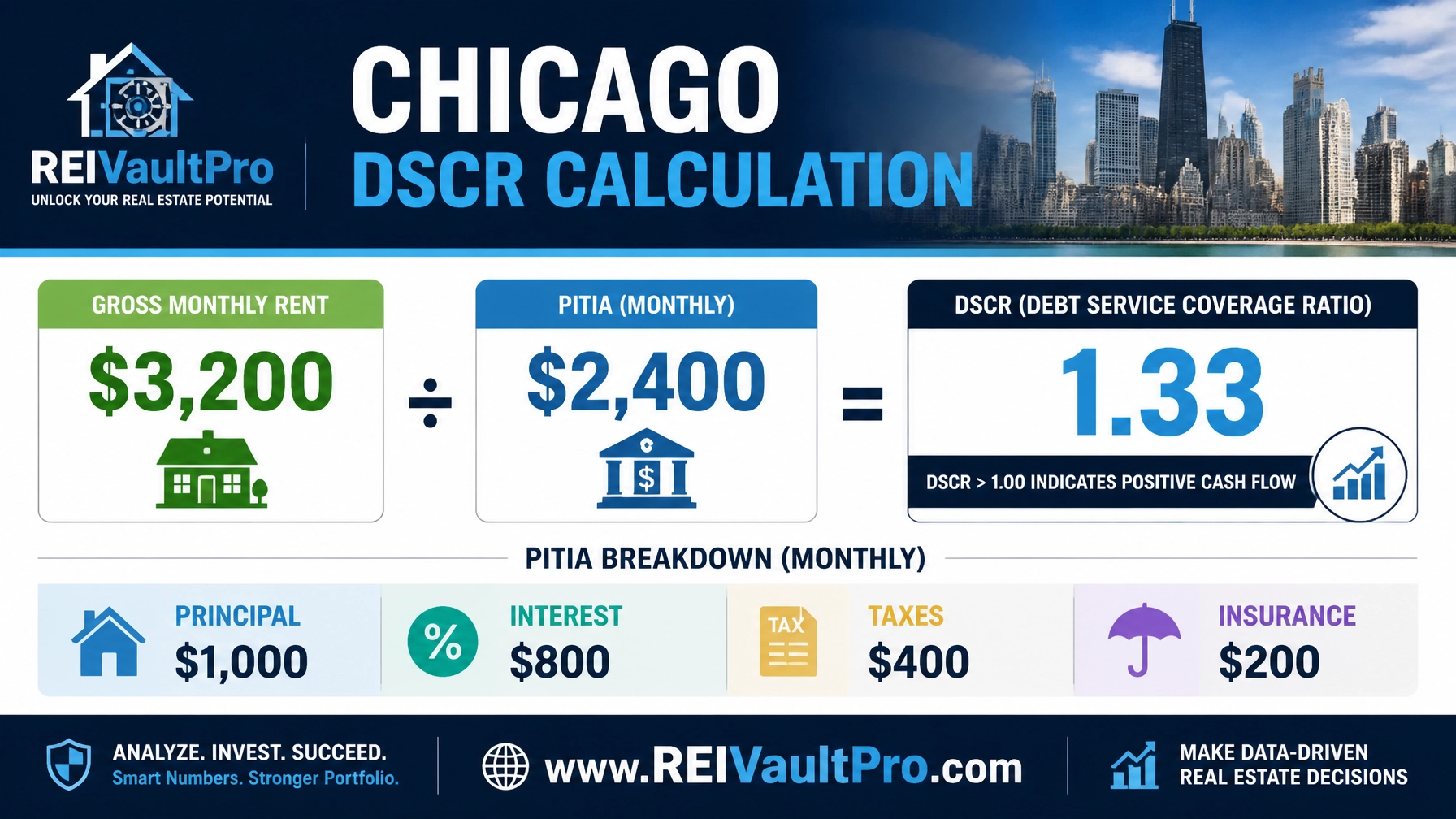

The DSCR Calculation: A Real-World Chicago Example

To understand how a lender views your deal, you must look at the numbers. Most Chicago lenders prefer a DSCR of 1.25 for the best rates, though programs exist for ratios as low as 0.75 or even "no-ratio" options.

PITIA: The sum of monthly principal, interest, taxes, insurance, and any association fees.

Application: This figure represents the "Debt Service" part of the ratio.

Gross Monthly Rent: The total income generated by a rental property before any expenses are deducted.

Application: This figure represents the "Income" part of the ratio.

Financial Scenario: Chicago 2-Unit Building

Imagine you are acquiring a classic Chicago two-flat.

- Purchase Price: $450,000

- Down Payment (20%): $90,000

- Loan Amount: $360,000

- Interest Rate: 7.25%

- Monthly Principal & Interest: $2,456

- Monthly Taxes: $450

- Monthly Insurance: $100

- Total Monthly PITIA: $3,006

Now, look at the income:

- Unit 1 Rent: $1,850

- Unit 2 Rent: $1,850

- Total Gross Monthly Rent: $3,700

The Calculation:

$3,700 (Rent) / $3,006 (PITIA) = 1.23 DSCR

In this scenario, the property generates 23% more income than the cost of the debt. This deal would be highly attractive to a Chicago DSCR loan lender, likely qualifying you for standard terms and up to 80% LTV. You can use the REI Vault Pro AI Deal Analyzer to run these numbers instantly for any property you find on the MLS or off-market.

Key Requirements for Chicago DSCR Loans in 2026

While personal income is not verified, lenders still require certain standards to ensure the security of the investment.

- Credit Score: Most programs require a minimum score of 620, though scores of 700+ unlock the most competitive interest rates and lower down payment requirements.

- Loan-to-Value (LTV): For purchase deals, you should plan for a 20-25% down payment. For a cash-out refinance, lenders typically cap the LTV at 75%.

- Property Type: Eligible properties include single-family homes, 2-4 unit buildings, condos, and even short-term rentals (Airbnb).

- Cash Reserves: Lenders often look for 3 to 6 months of PITIA in liquid reserves to ensure you can handle vacancies or unexpected repairs.

Compare these requirements to traditional financing, and you will see the flexibility offered to the modern real estate professional.

Scaling Your Portfolio Across Multiple States

The beauty of the DSCR model is its consistency. Whether you are looking at a multifamily building in Chicago, a vacation rental in Florida, or a fix-and-flip project in Georgia, the logic remains the same.

Portfolio Lending: A strategy where multiple properties are financed under a single loan or through a single lender relationship.

Application: Use this to simplify management and potentially lower overall interest costs as you scale.

As you build your wealth, consider diversifying your holdings. The REI Vault Pro platform provides the tools to manage these diverse assets. Access the Real Estate Investment Decision Engine to compare market trends in Illinois versus emerging markets in Alabama or Missouri.

Advanced Strategies: Cash-Out Refinance and BRRRR

Many Chicago investors use the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat). DSCR loans are the perfect "exit" strategy for this model.

- Buy: Purchase a distressed property using a bridge loan or hard money.

- Rehab: Improve the property to increase its value and market rent.

- Rent: Place a tenant to establish the gross monthly income.

- Refinance: Use a DSCR loan to pay off the short-term debt and "pull out" your initial capital.

- Repeat: Use that capital to buy the next property.

Because the DSCR lender cares about the new appraised value and the new rental income, you can often recover 100% of your initial investment if the value add was significant enough.

Related REI Vault Pro Resources

- AI Deal Analyzer: This tool allows you to input property data and instantly calculate your DSCR, cap rate, and cash-on-cash return, helping you decide if a Chicago deal meets lender criteria. Access the AI Deal Analyzer here.

- AI Deal Scoring: Use this to rank multiple potential investments in Cook County and beyond, ensuring you only spend time on the most profitable opportunities. Check out AI Deal Scoring.

- Investment Decision Engine: A comprehensive dashboard to visualize market trends and portfolio performance, essential for investors scaling across state lines. Explore the Decision Engine.

- Investor Starter Membership: Perfect for those looking to close their first DSCR deal with professional-grade tools and templates. Join as a Starter Investor.

- Core Investor Membership: For the growing landlord needing advanced analysis for 5+ properties and scaling strategies. Upgrade to Core Investor.

Conclusion

Scaling a real estate portfolio in Chicago does not have to be limited by your personal income or tax returns. By leveraging DSCR loans, you can focus on the profitability of the real estate itself. Whether you are a first-time landlord or an experienced investor looking to tap into equity through a cash-out refinance, understanding these ratios is the first step toward financial independence.

Access the tools and guidance needed to navigate the Chicago mortgage landscape with confidence. If you are ready to evaluate your next deal or refinance an existing property, start by using the analysis tools available at REI Vault Pro.

Start a Free Trial or Watch a Demo to see how professional-grade financing strategy can transform your investment journey.

FAQ Section

What is the minimum DSCR ratio required in Chicago?

Most lenders in Chicago look for a ratio of 1.0 to 1.25. A 1.0 ratio means the property breaks even. A 1.25 ratio means the property generates 25% more income than the debt payment. Some specialized programs accept ratios as low as 0.75.

Can I get a DSCR loan for a short-term rental (Airbnb) in Chicago?

Yes. Many DSCR lenders now allow for short-term rental income to be used for qualification. They may use specialized data services to estimate the "AirDNA" style potential of the property if it does not have a 12-month history.

Do I need to be a Chicago resident to get a Chicago DSCR loan?

No. DSCR loans are available to investors nationwide, as well as foreign nationals. You do not need to live in Illinois to purchase investment property in Chicago using this program.

Are interest rates higher for DSCR loans than conventional loans?

Generally, yes. Because DSCR loans carry more risk for the lender (due to lack of personal income verification), rates are typically 1% to 3% higher than a standard owner-occupied mortgage.

Is there a limit to how many DSCR loans I can have?

Most DSCR lenders do not have a hard limit on the number of properties you can finance. This makes it an ideal solution for scaling a large portfolio compared to Fannie Mae or Freddie Mac loans, which often limit borrowers to 10 financed properties.