Cash-Out Refi vs. Selling: What’s Better for Your Growth?

Deciding whether to sell a property or perform a cash-out refinance is one of the most significant crossroads a real estate investor or homeowner will face. Both paths lead to liquidity, but the long-term impact on your wealth and portfolio growth differs significantly.

If you are sitting on a property in Chicago, a vacation rental in Florida, or a growing portfolio in Virginia, you likely have a substantial amount of equity tied up in bricks and mortar. The question is: do you want to keep the asset and leverage it, or do you want to cash in your chips and walk away?

At Home Loans Network, we believe in transparency. There is no one-size-fits-all answer. Your choice depends on your current cash flow, your tax situation, and your ultimate goals for your real estate journey.

Explore the Cash-Out Refinance

Cash-Out Refinance A mortgage transition where a borrower replaces their existing home loan with a new, larger mortgage, receiving the difference between the two loans in cash at closing. Practical Application: Use this strategy to extract equity for property improvements, debt consolidation, or the down payment on a second investment property while retaining ownership of the original asset.

When you opt for a cash-out refinance, you are essentially betting on the future. You are choosing to keep your property because you believe it will continue to appreciate or provide steady rental income. In markets like California or Florida, where home values have seen consistent upward trends, holding onto an asset while pulling out capital can be a powerful wealth-building move.

How a Cash-Out Refinance Works in the Real World

Let's look at a typical scenario for a homeowner or investor. Imagine you own a property in a high-demand area of Michigan.

- Current Property Value: $400,000

- Existing Mortgage Balance: $150,000

- Maximum Loan-to-Value (LTV) for Refinance: 80%

- New Loan Amount: $320,000

- Estimated Closing Costs: $9,000

- Cash to You: $161,000

Visual: A deal breakdown chart showing: Property Value ($400k), Existing Loan ($150k), New Loan at 80% LTV ($320k), and Net Cash to Borrower ($161k after costs). Title: 'Cash-Out Refi Calculation' with 'Ebonie Beaco - Mortgage Loan Officer' at the bottom.

Visual: A deal breakdown chart showing: Property Value ($400k), Existing Loan ($150k), New Loan at 80% LTV ($320k), and Net Cash to Borrower ($161k after costs). Title: 'Cash-Out Refi Calculation' with 'Ebonie Beaco - Mortgage Loan Officer' at the bottom.

In this example, you walk away with $161,000 to invest in your next deal, yet you still own the original property. You can learn more about how this looks for your specific situation by visiting our home refinance page.

Compare the Benefits of Selling

Selling a property is the ultimate way to access the full value of your equity. While a refinance generally limits you to 75% or 80% of the home's value, selling allows you to walk away with almost everything (after commissions and taxes).

Property Liquidation The process of selling a real estate asset to convert equity into liquid cash. Practical Application: Sell when a property has reached its peak appreciation or when the neighborhood dynamics no longer align with your investment strategy.

For investors in Alabama or Arkansas who have seen a property double in value, selling might provide the large lump sum needed to move into commercial real estate or a larger multifamily complex. Selling is also a clean break. You no longer have to manage tenants, maintain the roof, or pay property taxes on that specific address.

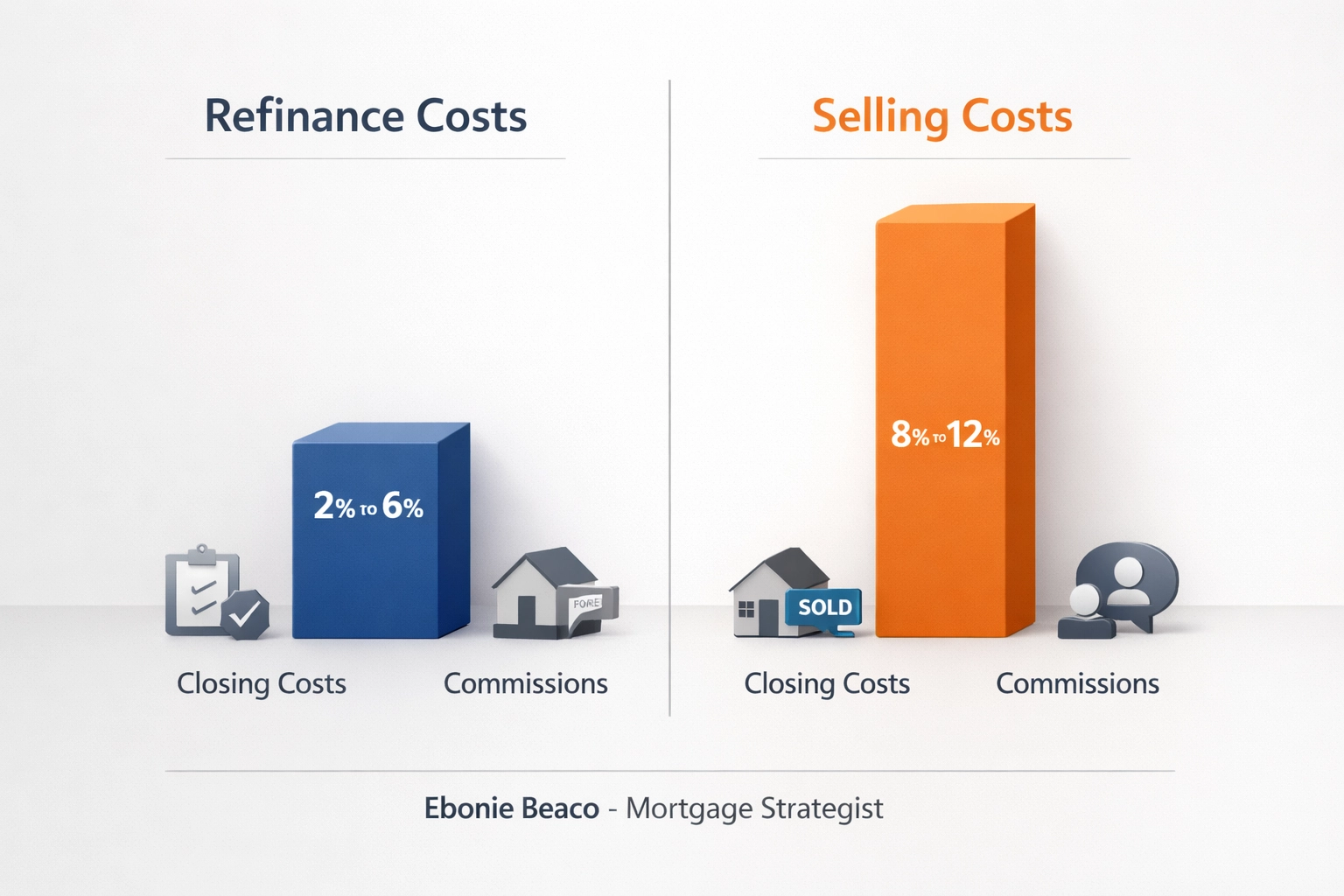

The True Cost of Selling

It is important to remember that selling isn't "free" money. You have to account for:

- Realtor Commissions: Typically 5% to 6%.

- Closing Costs: Title insurance, transfer taxes, and attorney fees.

- Capital Gains Tax: Unless you are doing a 1031 exchange or it is your primary residence (with specific exclusions), Uncle Sam will want a piece.

Visual: A comparison table showing 'Refi Costs (2-6%)' vs 'Selling Costs (8-12%)'. Title: 'The Cost of Capital Access' with 'Ebonie Beaco - Mortgage Loan Officer' at the bottom.

Visual: A comparison table showing 'Refi Costs (2-6%)' vs 'Selling Costs (8-12%)'. Title: 'The Cost of Capital Access' with 'Ebonie Beaco - Mortgage Loan Officer' at the bottom.

Growth Strategies: The Investor Perspective

For those focused on scaling a portfolio, the decision often centers on the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat). In this model, the cash-out refinance is the engine of growth. By refinancing, you pull your initial capital back out to buy the next property.

However, if you are a "Fix and Flip" investor in Georgia or Virginia, selling is the only way you realize your profit. Your growth is built on the speed of the sale and the margin between purchase/renovation costs and the final sale price.

Accessing Equity for Rental Portfolios

Many landlords now prefer DSCR (Debt Service Coverage Ratio) loans for their cash-out refinances.

DSCR Loan A mortgage program that qualifies a borrower based on the income generated by the property rather than personal income or tax returns. Practical Application: Investors use DSCR loans to scale quickly without being limited by their personal debt-to-income (DTI) ratios.

If your rental property in Illinois generates $2,500 in rent and the new mortgage payment (including taxes and insurance) is $2,000, your DSCR is 1.25. Most lenders find this very attractive. This allows you to pull cash out based on the property's performance, which is a transparent and logical way to grow. You can check potential payments using our mortgage calculators.

Compare: Tax Implications

Taxation is a massive factor in this decision.

- Refinance Proceeds are Debt: When you do a cash-out refinance, the money you receive is a loan. It is not considered income by the IRS. Therefore, you do not pay taxes on the cash you receive at the closing table.

- Sale Proceeds are Gains: When you sell, the profit you make is generally taxable. While primary homeowners in states like California or Florida may enjoy exemptions up to $250,000 (single) or $500,000 (married), investors are often hit with capital gains taxes unless they utilize a 1031 exchange to defer those taxes into a new property.

Why Keeping the Asset Often Wins for Long-Term Growth

If you are looking for long-term generational wealth, the "Never Sell" philosophy has its merits. When you keep a property and choose a cash-out refinance:

- You continue to benefit from appreciation.

- You continue to benefit from tax depreciation write-offs.

- Your tenants continue to pay down your principal.

- You maintain an inflation hedge.

In a city like Chicago, where rental demand remains high, keeping a well-located multi-unit building while using a cash-out refinance to fund your next project in Indiana or Kentucky allows you to grow two assets simultaneously instead of just one.

Jump in: Which Option Fits You?

Ask yourself these three questions:

- Is the property still appreciating? If yes, a cash-out refinance allows you to stay in the game while getting the cash you need.

- Does the property cash flow well? If the rental income easily covers a new, higher mortgage payment, refinancing is likely the smarter move.

- Do you have a "better" place for the money? If you have a deal lined up that offers a significantly higher return than your current property, selling might be the fastest way to get there.

If you are still weighing your options, exploring our mortgage basics can provide more context on the different loan types available to you.

Summary of Differences

- Cash-Out Refi: Best for investors who want to scale (BRRRR), homeowners who want to improve their current home, and those looking to avoid immediate taxes on equity.

- Selling: Best for those ready to exit a market, investors moving into different asset classes (like commercial), or individuals needing the absolute maximum amount of cash possible from a single property.

Visual: A flowchart asking: 'Is the asset performing?' -> Yes -> 'Cash-Out Refi'. 'Is the asset performing?' -> No -> 'Sell'. Title: 'Strategy Flowchart' with 'Ebonie Beaco - Mortgage Loan Officer' at the bottom.

Visual: A flowchart asking: 'Is the asset performing?' -> Yes -> 'Cash-Out Refi'. 'Is the asset performing?' -> No -> 'Sell'. Title: 'Strategy Flowchart' with 'Ebonie Beaco - Mortgage Loan Officer' at the bottom.

Navigate Your Strategy with Confidence

Real estate is a game of math and timing. Whether you are looking at a fix-and-flip in Missouri or a long-term rental portfolio in Virginia, how you handle your equity determines how fast you can grow.

Transparency is at the heart of everything we do at Home Loans Network. We want you to have the data you need to make an informed decision for your financial future. If you need a deep dive into your specific numbers or want to see which loan programs: from DSCR to bank statement loans: fit your profile, let's talk.

Reach out for a strategy session or to explore your mortgage options.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 www.homeloansnetwork.com 312-392-0664