California vs. Florida Jumbo Loans: Which Is Better For Your Luxury Property Purchase?

The luxury real estate landscape is shifting rapidly as we move through 2026.

High-end buyers are no longer just looking at the aesthetic of a coastal estate or a mountain retreat.

You are likely looking at how the financing structure impacts your long-term wealth.

Whether you are eyeing a beachfront villa in Malibu or a penthouse in Miami, understanding the nuances of jumbo financing is essential.

California and Florida remain the two titans of luxury real estate, but their mortgage markets operate with distinct differences.

Explore how these regional variations influence your ability to secure high-balance funding and which state offers the most strategic advantages for your portfolio.

Defining the 2026 Jumbo Landscape

Before comparing states, you must understand what qualifies as a jumbo loan in today’s market.

Jumbo Loan: A mortgage that exceeds the conforming loan limits established by the Federal Housing Finance Agency (FHFA).

Benefit: This allows you to access capital for high-value properties that exceed the limits of standard Fannie Mae or Freddie Mac programs.

High-Cost Area: A geographic region where the median home price is significantly higher than the national average, resulting in elevated conforming loan limits.

Benefit: It allows you to use conventional financing for larger amounts before triggering jumbo requirements, which often carry stricter underwriting.

For 2026, the baseline conforming limit is $832,750.

However, in many parts of California and Florida, these limits reach as high as $1,249,125 for single-family homes.

If your loan amount exceeds these figures, you are officially in the jumbo category.

Access the Home Loans Network jumbo loans page to see current requirements for these high-balance options.

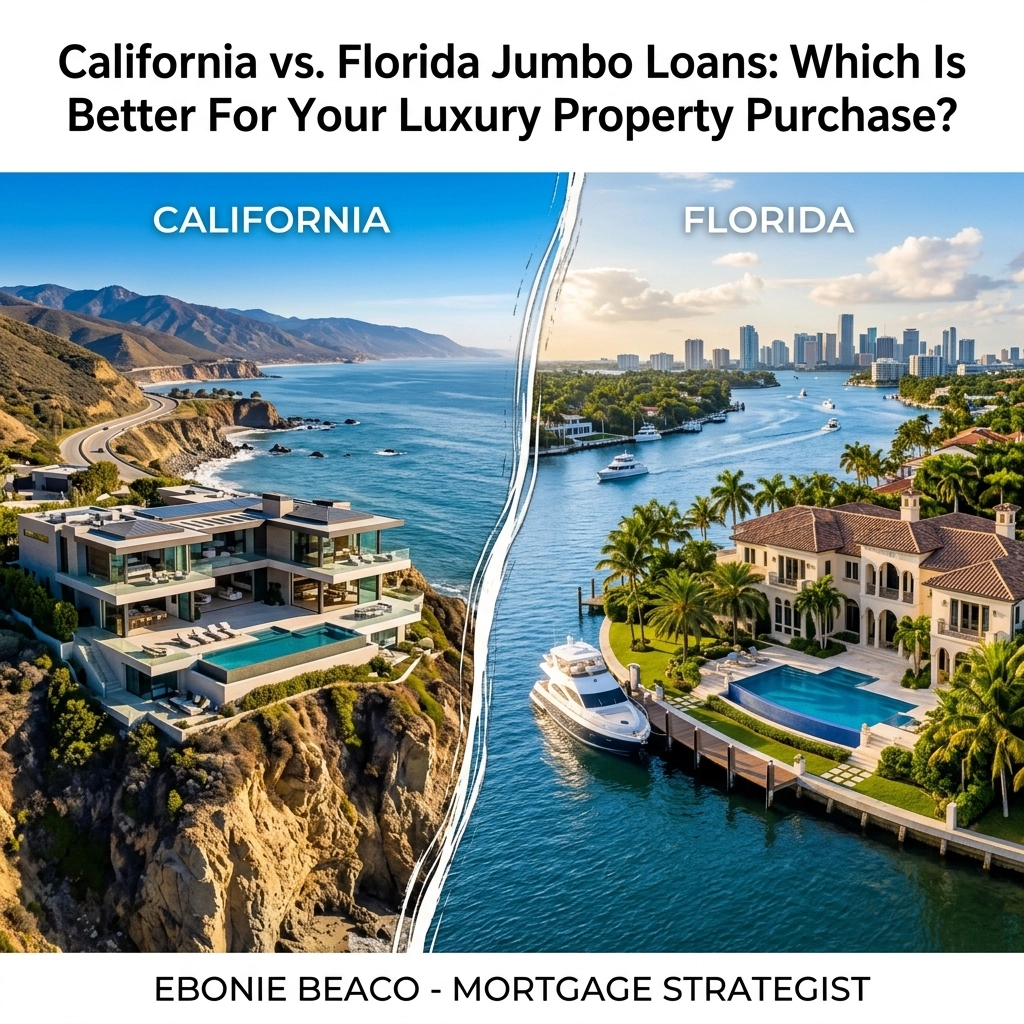

California Jumbo Loans: Navigating High-Stakes Equity

California remains one of the most expensive real estate markets in the world.

From the tech hubs of Silicon Valley to the entertainment corridors of Los Angeles, California Jumbo Loans are a standard tool for luxury buyers.

The market here is characterized by high property values and a competitive lending environment.

Lenders in California are accustomed to complex financial profiles, such as self-employed entrepreneurs or executives with significant stock options.

RSU (Restricted Stock Units): Compensation offered by an employer to an employee in the form of company stock.

Benefit: Many California lenders allow you to use vested RSU income to qualify for a larger jumbo loan amount.

Underwriting Trends in the Golden State

California lenders often require substantial cash reserves.

Expect to show six to twelve months of mortgage payments (PITIA) sitting in liquid accounts.

While interest rates for California Jumbo Loans are competitive, the sheer size of the loans means that even a small rate fluctuation is significant for your monthly cash flow.

Many investors in cities like San Francisco or San Diego utilize interest-only mortgage options to keep their monthly obligations lower during the initial years of ownership.

Florida Jumbo Loans: The New Frontier of Luxury

Florida has seen a massive influx of high-net-worth individuals over the last few years.

Florida Jumbo Loans have become increasingly popular in markets like Miami, Palm Beach, and Naples.

The lack of state income tax in Florida makes it an attractive destination for luxury property purchases, but the financing side has its own set of hurdles.

Hazard Insurance: A component of homeowners insurance that protects against physical damage to the property.

Benefit: Proper coverage ensures that your high-value asset is protected, which is a non-negotiable requirement for jumbo lenders.

In Florida, insurance costs carry more weight than in almost any other state.

Lenders will look closely at your insurance premiums when calculating your Debt-to-Income (DTI) ratio.

Geographic Impact on Florida Rates

While Florida does not have a state income tax, property taxes and insurance can add up.

Lenders offering Florida Jumbo Loans may price their products differently based on the property’s proximity to the coast.

If you are buying a luxury condo in Miami, your lender might require a higher down payment: often 20% to 30%: compared to a single-family home in an inland luxury community.

Comparing the Requirements: CA vs. FL

When you compare these two markets, the fundamental requirements for jumbo financing remain similar, but the application varies.

- Credit Scores: Most jumbo programs require a minimum score of 700 to 720, though the best rates are reserved for those above 760.

- Down Payments: Expect to put down at least 10% to 20%. California luxury markets sometimes see more 10% down options, while Florida lenders often prefer 20% due to market volatility.

- Appraisals: For properties exceeding $2 million, many lenders require two independent appraisals to verify the value.

Jump in and use our mortgage calculators to see how different down payment amounts affect your jumbo loan scenario in either state.

Strategic Financing for Luxury Investors

If you are a real estate investor rather than a primary resident, the strategy changes.

In both California and Florida, luxury rental markets are booming.

Many investors are moving away from traditional jumbo loans and toward DSCR (Debt Service Coverage Ratio) Loans.

DSCR Loan: A financing option where qualification is based on the cash flow generated by the property rather than your personal income.

Benefit: This allows you to scale your portfolio without being restricted by your personal DTI or tax returns.

The Rise of Short-Term Rental Financing

Florida, in particular, is a hotspot for Airbnb and short-term rental investments.

Financing a luxury short-term rental requires a lender who understands the seasonal income patterns of markets like Orlando or the Florida Keys.

California also offers lucrative short-term rental opportunities in coastal towns, though local regulations are often stricter.

Explore our loan programs to see how DSCR and Non-QM options can fit your investment goals.

The Atlanta and Chicago Perspective

While California and Florida dominate the headlines, other markets are seeing a surge in jumbo loan demand.

Chicago Jumbo Loans are essential for buyers in the Gold Coast or the North Shore.

The Chicago market offers a lower entry price for luxury compared to Los Angeles, but property taxes are a significant factor in your qualification.

Similarly, Atlanta has become a hub for luxury real estate in the Southeast.

High-end buyers in Buckhead or Milton are increasingly seeking jumbo financing as home prices in Georgia continue to climb.

Whether you are looking at California Jumbo Loans, Florida Jumbo Loans, or financing in Atlanta, the need for a transparent and experienced lender is the same.

A Real-World Comparison: The $2.5 Million Purchase

Let’s look at a practical example of how financing might look for a $2,500,000 purchase in both states.

Scenario A: Los Angeles, California

- Purchase Price: $2,500,000

- Down Payment (20%): $500,000

- Loan Amount: $2,000,000

- Estimated Property Tax (1.2%): $30,000/year

- Reserves Required: 12 months ($150,000+)

Scenario B: Miami, Florida

- Purchase Price: $2,500,000

- Down Payment (20%): $500,000

- Loan Amount: $2,000,000

- Estimated Property Tax (1.1% + higher insurance): $27,500 + $15,000 insurance

- Reserves Required: 6 to 12 months ($120,000+)

In this scenario, while the property tax might be slightly lower in Florida, the insurance premium is nearly triple what you might pay in a non-fire-zone area of California.

Your total monthly payment could be higher in Florida despite the lower purchase tax, which is a detail many buyers overlook until they reach the loan process.

Which State Wins for Luxury Financing?

There is no single winner; the best choice depends on your specific financial profile.

California is ideal for those with high equity and complex income structures (like RSUs or business ownership).

The lending market there is highly sophisticated and can handle "out of the box" scenarios.

Florida is the clear winner for those looking to maximize their take-home pay via tax savings.

However, you must be prepared for the rising costs of insurance and a potentially more conservative appraisal environment.

If you are an investor using the BRRRR method or looking for home refinance options, both states offer robust opportunities to pull equity out of luxury assets for your next purchase.

Final Steps for Your Luxury Purchase

Securing a jumbo loan requires more than just a high income.

It requires a strategy that accounts for regional market trends, insurance fluctuations, and tax implications.

Whether you are focused on California Jumbo Loans for a primary residence or looking for a DSCR loan for a Florida vacation rental, the right guidance is vital.

Compare your options carefully.

Review the mortgage basics to ensure you have a firm grasp of the terminology before you start your application.

When you are ready to take the next step, select a loan officer who understands the intricacies of high-balance lending in your target market.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664