California HELOC Vs. Cash-Out Refinance: Which Is Better For Your Home Equity?

SEO Title: California HELOC vs. Cash-Out Refinance: Comparing 2026 Equity Strategies

Meta Description: Discover whether a California HELOC or Cash-Out Refinance is better for your home equity. Compare interest rates, terms, and investment strategies for CA property owners in 2026.

URL Slug: california-heloc-vs-cash-out-refinance-2026

Featured Image Recommendation: A professional landscape photograph of a modern California luxury home at sunset with a "www.REIVaultPro.com" overlay.

SEO Alt Text: Modern California luxury home representing high home equity for HELOC or cash-out refinance.

Social Media Excerpt: Sitting on record home equity in California? Discover whether a HELOC or a Cash-Out Refinance is the best move for your investment portfolio or primary residence in 2026.

SEO Tags: California Real Estate, Home Equity, HELOC, Cash-Out Refinance, Investment Property Loans, 2026 Mortgage Trends, California Investors

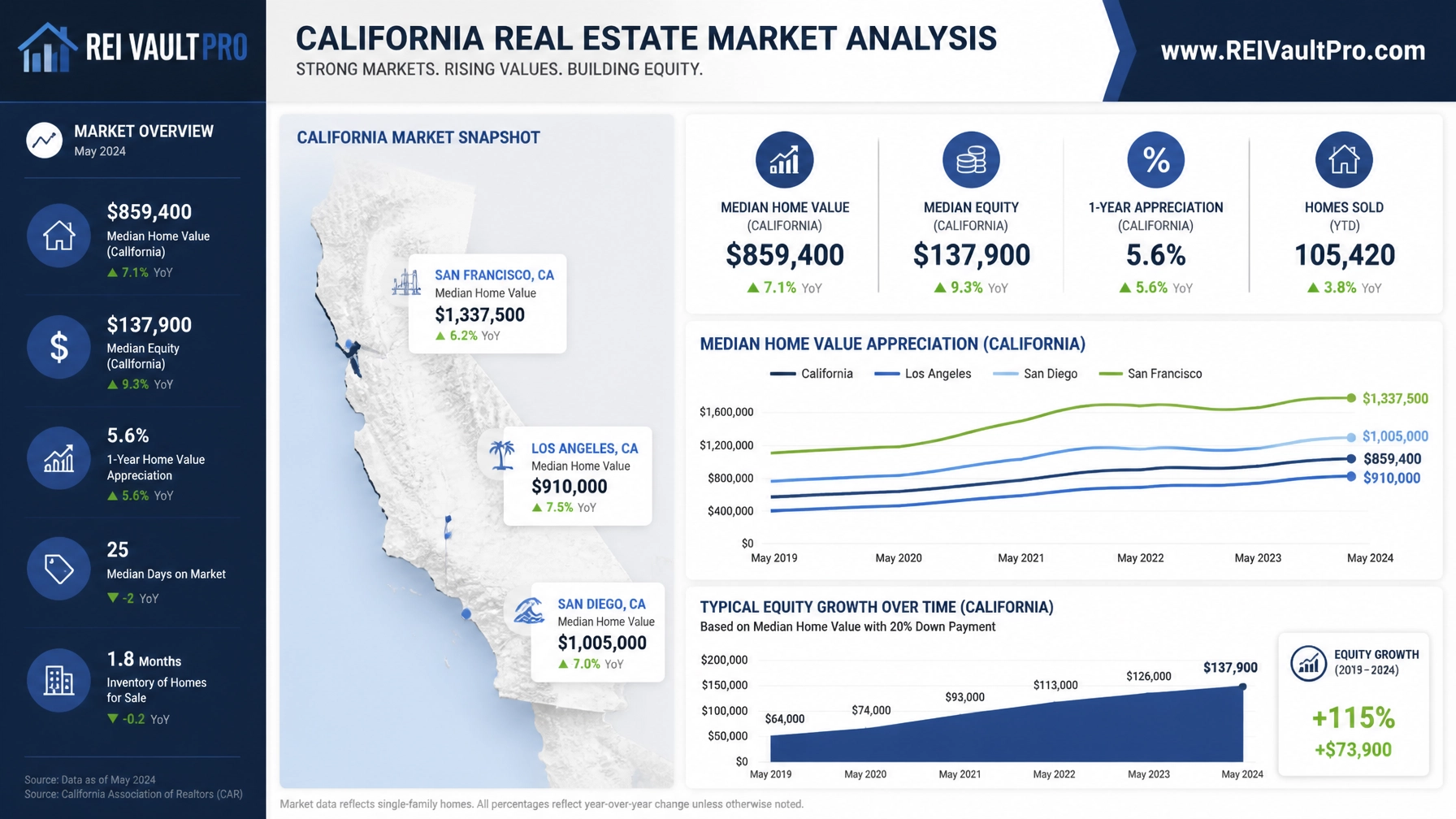

California homeowners and real estate investors are entering 2026 with substantial levels of home equity. With the statewide median home price holding steady near $905,000, many property owners in markets like Los Angeles, San Diego, and the San Francisco Bay Area are looking for the most efficient ways to access their wealth. Choosing between a Home Equity Line of Credit (HELOC) and a Cash-Out Refinance requires a clear understanding of your financial goals, your current mortgage rate, and the specific needs of your real estate portfolio.

Defining Your Equity Options

HELOC (Home Equity Line of Credit)

A revolving credit line secured by your home's equity that allows you to borrow, repay, and borrow again during a set draw period.

You use a HELOC as a flexible "war chest" for ongoing costs like property renovations or as a down payment for a new investment.

Cash-Out Refinance

A new primary mortgage that replaces your existing loan with a larger balance, allowing you to receive the difference in cash at closing.

You utilize a cash-out refinance to lock in a long-term fixed interest rate while extracting a lump sum of capital for immediate use.

The 2026 California Real Estate Landscape

The California market in 2026 is characterized by stable but high home values. While the rapid appreciation of previous years has slowed to a more sustainable pace of roughly 3.6%, the sheer volume of equity remains at historic highs. For investors, this environment provides a unique opportunity to leverage existing assets to scale their portfolios.

Current mortgage rates for 30-year fixed loans are hovering in the mid-6% range. This creates a strategic crossroads. If you secured a mortgage in 2020 or 2021 with a rate below 4%, a cash-out refinance would require you to trade that low rate for today’s market rate on your entire loan balance. In this scenario, a HELOC often becomes the more attractive option as it leaves your first mortgage untouched.

Comparing the Mechanics: HELOC vs. Cash-Out Refinance

Interest Rate Structures

A Cash-Out Refinance typically offers a fixed interest rate. This provides long-term predictability for your monthly payments. In 2026, investors are using these to stabilize their debt on properties they intend to hold for 10 to 30 years.

Conversely, a HELOC usually features a variable interest rate tied to a benchmark like the Prime Rate. While HELOC rates in 2026 are competitive, they are subject to market fluctuations. If you expect to pay back the borrowed funds quickly, perhaps after completing a Fix and Flip project, the variable rate risk may be minimal compared to the benefit of flexibility.

Payment Flexibility

HELOCs often provide an "interest-only" payment option during the initial draw period, which can last 5 to 10 years. This keeps your immediate overhead low, which is vital for maintaining cash flow while a property is under renovation.

A Cash-Out Refinance is fully amortizing from day one. You begin paying back both principal and interest immediately on the full loan amount. This structure is better suited for investors who want a steady, predictable path to building equity over time without the "payment shock" that can occur when a HELOC's draw period ends.

Upfront Costs and Closing Fees

Closing costs for a Cash-Out Refinance are similar to those of a standard home purchase, often ranging from 2% to 5% of the total loan amount. Since you are refinancing the entire balance, these costs can be significant.

HELOCs generally have much lower upfront costs. Many California lenders offer HELOC programs with low or even no closing costs, provided the line remains open for a certain period. This makes the HELOC a more cost-effective tool for accessing smaller amounts of capital or for funds you only need occasionally.

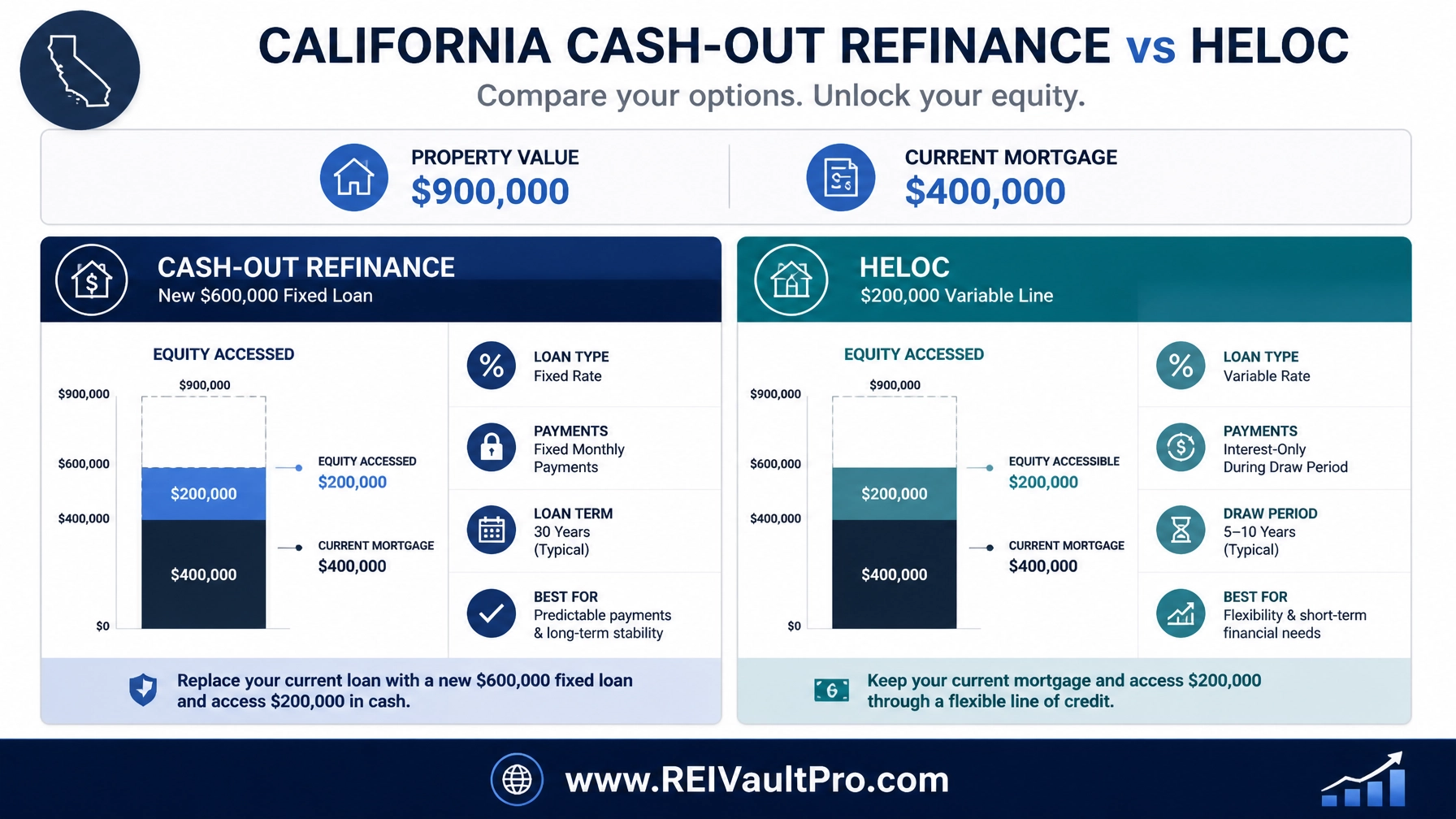

Strategic Calculations for California Investors

To understand how these tools work in the real world, consider a property in a high-demand area like Riverside or Sacramento.

The Scenario:

- Current Property Value: $900,000

- Existing Mortgage Balance: $400,000

- Tappable Equity (at 80% LTV): $320,000

If an investor wants to access $200,000 to purchase a new rental property, they have two paths:

- The Cash-Out Refi Path: Replace the $400,000 loan with a new $600,000 loan. If the new rate is 6.5%, the investor pays interest on the full $600,000 immediately.

- The HELOC Path: Keep the original $400,000 mortgage (perhaps at a 3.5% rate) and open a $200,000 HELOC. The investor only pays interest on the portion of the HELOC they actually draw.

For many, the blended interest rate of a low-rate first mortgage and a higher-rate HELOC is often lower than the rate of a single large cash-out refinance in today's market. Use a Mortgage Calculator to run these numbers for your specific property.

Visualizing California Market Equity Trends

Understanding your local market is essential when deciding how much equity to tap. In 2026, coastal California cities continue to show high demand despite affordability challenges. Investors in San Francisco and Los Angeles are frequently using HELOCs to fund ADU (Accessory Dwelling Unit) construction, adding value and rental income to their existing lots without disrupting their primary financing.

Inland Empire and Central Valley investors, where price growth has been more volatile, often prefer the security of a Cash-Out Refinance to lock in fixed costs and insulate themselves from potential interest rate hikes in the future.

Use Cases for California Real Estate Professionals

Scaling the BRRRR Method

Investors using the Buy, Rehab, Rent, Refinance, Repeat (BRRRR) strategy often lean toward the cash-out refinance. Once a property is stabilized and appraised at a higher value, a DSCR Loan Pre-Qualification can help determine how much equity can be pulled to fund the next acquisition.

Short-Term Capital Needs

Wholesalers and fix-and-flip investors often prefer the HELOC. Having a standby line of credit allows you to make "all-cash" offers on distressed properties, giving you a competitive edge in tight California markets. You can jump in on a deal, use the HELOC for the purchase and rehab, and then pay it off once the property is sold.

Portfolio Diversification

Using equity to diversify into different property types is a common 2026 strategy. A homeowner in Orange County might use a HELOC to provide the down payment for a multi-unit building in a high-growth area of Georgia or Florida. This allows the investor to spread their risk across different geographic markets while keeping their California home as the primary engine for wealth generation.

Due Diligence and Risk Management

Before tapping into your home equity, it is critical to perform a thorough Title Review to ensure there are no existing liens or issues that could complicate your financing. Furthermore, you should analyze the local market data to ensure you are not over-leveraging in an area that may experience a price correction.

Accessing equity is a powerful way to build wealth, but it increases your total debt. Ensure your rental income or personal cash flow can comfortably support the new payments. For those managing multiple rentals, maintaining an updated Rent Roll is essential for demonstrating your property’s performance to lenders during the application process.

Related REI Vault Pro Resources

- Real Estate Deal Analyzer Suite: A comprehensive set of calculators to help you compare the ROI of different financing strategies, including HELOCs and cash-out refinances.

- AI Market Analysis Tool: Access real-time data on California sub-markets to see where equity growth is strongest before you decide to tap into your property's value.

- DSCR Loan Pre-Qualification Worksheet: Use this tool to see if your investment property generates enough income to qualify for a cash-out refinance without using your personal tax returns.

- Mortgage Assumption Worksheet: Explore alternative ways to manage existing debt when buying or selling properties with high equity.

- Title Review Red Flag Checklist: Ensure your property is ready for a new lien or refinance by identifying potential title issues early.

Conclusion

The decision between a California HELOC and a Cash-Out Refinance in 2026 depends heavily on your existing mortgage rate and your intended use for the funds. HELOCs offer unmatched flexibility and are ideal for preserving low-rate first mortgages. Cash-out refinances provide the security of fixed rates and are perfect for long-term debt restructuring.

By understanding these mechanics and analyzing your local market data, you can turn your home equity into a strategic tool for financial growth. Whether you are looking to renovate, diversify, or scale your portfolio, choose the financing option that aligns with your long-term wealth objectives.

Explore your options and take the next step toward optimizing your home equity.

Watch a Demo | Start a Free Trial | Join Now

FAQ Section

Is a HELOC or a Cash-Out Refinance better for California investors in 2026?

The best choice depends on your current interest rate. If you have a very low rate (under 4%), a HELOC is usually better because it allows you to keep that rate on your primary loan. If your current rate is 6% or higher, a cash-out refinance might be better to consolidate your debt into one fixed-rate loan.

What is the maximum LTV for a cash-out refinance in California?

Most lenders allow for a maximum Loan-to-Value (LTV) ratio of 80% for primary residences and 70-75% for investment properties. This means you must leave at least 20-30% equity in the property.

Are HELOC interest payments tax-deductible?

For primary residences, interest on a HELOC is typically only deductible if the funds are used to "buy, build, or substantially improve" the home that secures the loan. For investment properties, the rules differ. You should always consult a tax professional regarding your specific situation.

How long does it take to close a HELOC vs. a Cash-Out Refi in California?

A HELOC can often be closed in 2 to 4 weeks, as the appraisal and underwriting requirements are sometimes less stringent. A Cash-Out Refinance typically takes 30 to 45 days, as it involves a more comprehensive appraisal and full mortgage underwriting process.

Can I get a HELOC on an investment property in California?

Yes, though interest rates for investment property HELOCs are generally higher than for primary residences, and the maximum LTV may be lower. Not all lenders offer this product, so it is important to work with a specialist in investor financing.