California HELOC Secrets Revealed: What Your Bank Doesn’t Want You to Know About Your Home’s Value

California homeowners sit on a gold mine of equity. With property values in cities like Los Angeles, San Diego, and San Francisco reaching historic highs, the temptation to tap into that wealth is stronger than ever. Banks and credit unions are flooding mailboxes with Home Equity Line of Credit (HELOC) offers, promising easy access to cash with flexible terms.

However, there is a side to the California HELOC that lenders rarely discuss in their colorful brochures. Beyond the low introductory rates and the promise of a "safety net" lies a complex financial instrument with specific legal and structural risks.

Explore the hidden mechanics of home equity lending. Jump in to understand how these loans actually function in the California market and why your bank might be keeping certain details under wraps.

The Secret Home Equity Drain: Daily Balance Interest

Most homeowners assume their HELOC interest is calculated similarly to their primary mortgage. This is a common misconception that costs borrowers thousands of dollars over the life of the loan.

Average Daily Balance: A method where interest is calculated based on the balance of the loan at the end of every single day. Practical Application: Making multiple small payments throughout the month or paying early reduces the daily balance faster than a single payment at the end of the month, lowering your total interest cost.

Banks typically charge interest on your average daily balance. While a standard mortgage interest charge is set once a month, a HELOC is more like a credit card. If you draw $50,000 for a renovation and wait until the 30th to make a payment, you pay interest on that full $50,000 for all 30 days.

If you are looking to maximize your equity, understanding this timing is vital. You can find more about these mechanics on our mortgage basics page.

The California Protection Myth: Anti-Deficiency Laws

California is famous for its borrower-friendly "anti-deficiency" laws. Many homeowners believe that if the market crashes and they lose their home to foreclosure, the lender cannot come after their personal assets for the remaining balance.

Deficiency Judgment: A court order allowing a lender to collect the remaining balance if a foreclosure sale does not cover the full loan amount. Practical Application: Knowing whether your loan is "purchase money" or "recourse" determines if your personal savings and wages are at risk during a default.

Here is the secret: Most HELOCs in California are NOT protected by standard anti-deficiency laws. These protections generally apply only to "purchase money" loans used to buy your primary residence. Since a HELOC is typically taken out after you already own the home, it is often classified as a recourse loan.

If the California housing market dips and your home is sold at a loss, the HELOC lender may have the legal right to sue you for the difference. This is a massive risk that banks rarely highlight during the application process.

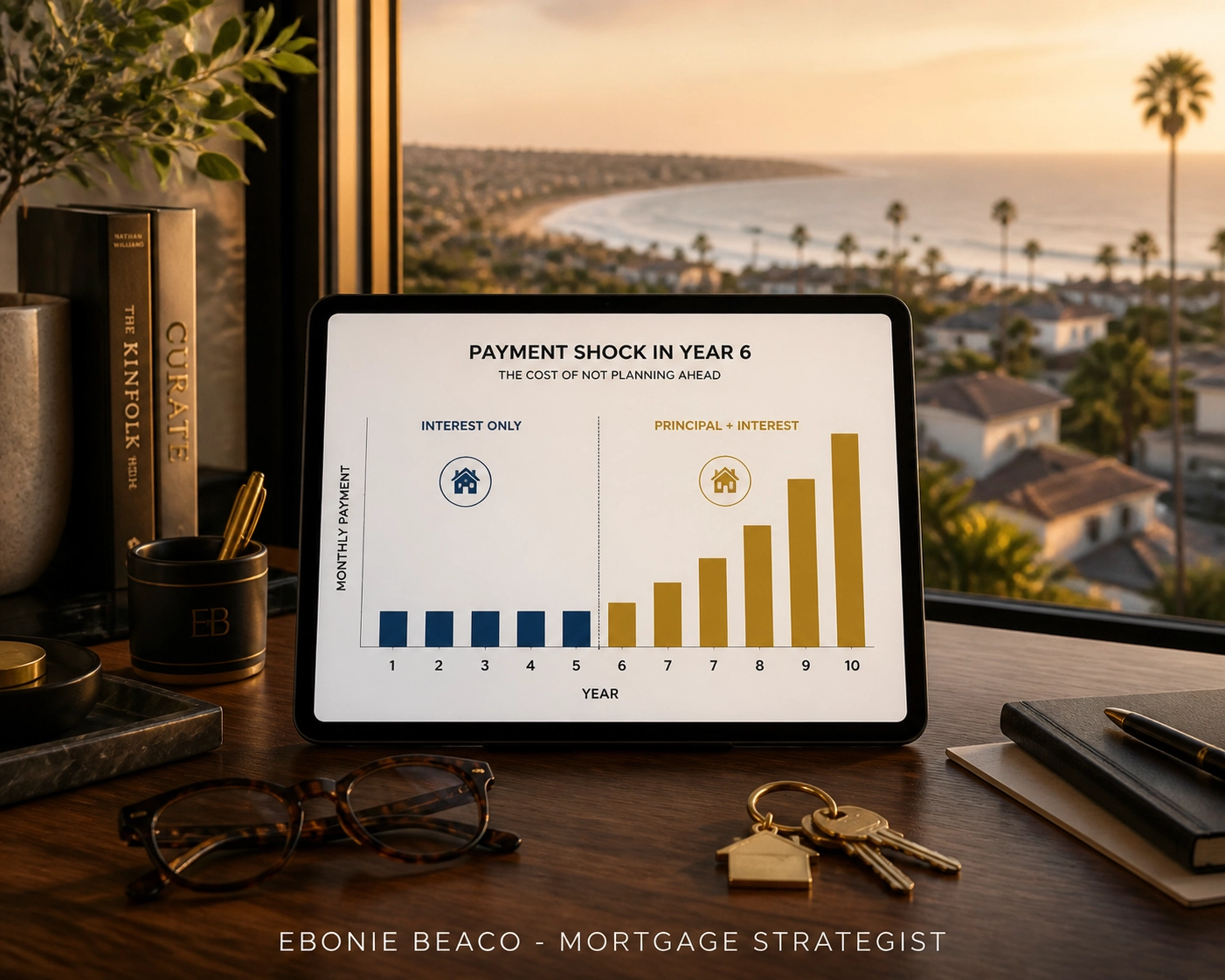

The Repayment Cliff: The Draw Period vs. Repayment Period

Lenders love to market the "low monthly payments" of a HELOC. What they are actually marketing is the interest-only payment option available during the draw period.

Draw Period: The initial phase of a HELOC (usually 5 to 10 years) where you can borrow money and often only pay interest. Benefit: Provides maximum cash flow flexibility during the early years of the loan.

Repayment Period: The second phase (usually 10 to 20 years) where you can no longer borrow money and must pay back both principal and interest. Benefit: Ensures the debt is eventually retired, though it significantly increases monthly costs.

The "secret" here is the payment shock. In California, where HELOC balances can easily reach $200,000 or $300,000, the jump from an interest-only payment to a fully amortized principal and interest payment can be devastating. Thousands of homeowners find themselves unable to afford the new payment once the draw period ends, forcing them into a home refinance they might not qualify for if interest rates have risen.

Visual: A chart showing the "Payment Cliff" where a $500 monthly interest-only payment jumps to a $2,100 principal and interest payment after 10 years.

Visual: A chart showing the "Payment Cliff" where a $500 monthly interest-only payment jumps to a $2,100 principal and interest payment after 10 years.

Accessing Your Equity: A Real World California Example

Let's look at how a typical equity strategy works for a homeowner in a high-value market. Imagine a homeowner in Orange County who wants to use their equity to fund a second investment property using a DSCR (Debt Service Coverage Ratio) loan.

DSCR Loan: A mortgage for investment properties where qualification is based on the property's rental income rather than the borrower's personal income. Benefit: Allows investors to scale their portfolios without being restricted by personal Debt-to-Income (DTI) limits.

The Scenario:

- Current Home Value: $1,200,000

- Existing First Mortgage: $650,000

- Lender's Maximum CLTV (Combined Loan to Value): 80%

The Calculation:

- Calculate total allowable debt: $1,200,000 x 0.80 = $960,000

- Subtract existing mortgage: $960,000 - $650,000 = $310,000

- Available HELOC Limit: $310,000

With this $310,000, the homeowner can provide a down payment for a multifamily property in a market like Atlanta, Georgia or Richmond, Virginia. By using the HELOC as the "bridge" for the down payment and a DSCR investor loan for the purchase, the homeowner turns their California equity into a cash-flowing asset in another state.

https://cdn.marblism.com/1LSjKKTAZun.webp

{kind=link}

The Hidden CLTV Squeeze

While many banks advertise HELOCs up to 90% or even 100% of your home's value, the reality in 2026 is much tighter. Lenders have become increasingly conservative with Combined Loan to Value (CLTV) ratios.

CLTV: The ratio of all loans on a property compared to its appraised value. Benefit: Helps you determine the maximum "safety ceiling" a lender will allow before they stop lending against your equity.

In California, if you have a high DTI (Debt-to-Income) ratio, most lenders will cap your CLTV at 75% or 80%. If your home is worth $1,000,000 and you owe $750,000, you might think you have $250,000 in equity. However, if the lender caps the CLTV at 80%, you can only access $50,000.

The bank doesn't want you to know that your "accessible" equity is often much lower than your "actual" equity. You can check your own numbers using our mortgage calculators.

Variable Rate Exposure: The Prime Rate Connection

Nearly all HELOCs are variable-rate products tied to the Prime Rate.

Margin: A fixed percentage added to the Prime Rate by the lender to determine your total interest rate. Practical Application: If Prime is 7.5% and your margin is 1.0%, your interest rate is 8.5%. The margin stays the same, but Prime can change at any time.

Many California borrowers were caught off guard when rates climbed from historical lows. Because HELOCs adjust monthly, your payment can change without warning. Banks often highlight the "teaser rate" for the first six months, but they rarely emphasize how high the "ceiling" or lifetime cap actually is: often as high as 18%.

If you are looking for more stability, you might want to compare a HELOC against a fixed-rate cash-out refinance.

Strategies for Savvy Investors and Homeowners

If you are a real estate investor or a homeowner in Michigan, Florida, or Virginia looking to leverage equity, there are better ways to play the game.

- Use it for Value-Add: Use HELOC funds for renovations that increase the property value, then perform a cash-out refinance to pay off the HELOC and lock in a fixed rate.

- The 3-Day Right of Rescission: Remember that federal law gives you three business days to cancel a HELOC after signing the closing documents. If you find a better deal or have second thoughts, use this window.

- Negotiate the Margin: Most borrowers don't realize the margin is negotiable. If you have a high credit score and low DTI, ask for a lower margin.

Accessing equity is a powerful tool for wealth building, especially when used for strategies like BRRRR (Buy, Rehab, Rent, Refinance, Repeat). Whether you are a Florida HELOC seeker or a Georgia HELOC lender client, the principles of leverage remain the same.

https://cdn.marblism.com/G5UiOoT0lXR.webp

{kind=link}

The Georgia and Florida Connection

While this guide focuses on California, the secrets of the HELOC apply across the sunbelt and the Midwest. In high-growth areas like Florida and Georgia, equity is growing at a rapid pace. Investors in these states often use HELOCs from their primary residences to fund Airbnb and short-term rental financing.

By understanding the "Daily Balance" secret and the "Repayment Cliff," investors in Alabama, Arkansas, and Virginia can avoid the traps that snare uneducated borrowers.

Access our online forms to start evaluating your specific scenario and see how much equity you can safely unlock.

Beyond the Bank’s Script

Banks are in the business of selling debt. They want you to see your home as an ATM. While your home's value is a massive asset, it is also your shelter. Using it as collateral requires a strategy that goes beyond the bank's sales pitch.

Explore your options carefully. Compare the flexibility of a HELOC with the stability of other loan programs. Every financial decision should move you closer to your goals of wealth and security, not just provide a temporary patch for expenses.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

What happens when the "unlimited" equity in the California market finally hits a ceiling? Most homeowners are prepared for a rise in value, but very few are prepared for the "freeze" that banks can implement on your credit line at a moment's notice. If the market shifts, your bank can shut down your access to funds instantly, even if you’ve never missed a payment. Are you prepared for the day your safety net disappears?