California HELOC Secrets Revealed: What Your Bank Doesn’t Want You to Know About Your Equity

Most homeowners in California, Florida, and Georgia are sitting on a gold mine.

Your home equity has likely skyrocketed over the last few years.

While you see a beautiful place to live, your bank sees something else.

They see a massive cushion of safety for their loan.

What they often fail to mention is that this equity is "dead money" until you decide to put it to work.

Keeping your equity locked inside your walls might feel safe, but it often prevents you from building real wealth.

Jump in as we explore the strategies banks rarely volunteer during a standard branch visit.

The Secret Home Equity Drain: Why Sitting Still Costs You

Many homeowners believe that high equity is always a win.

In one sense, it is.

However, there is a hidden cost to leaving that equity untouched.

Inflation constantly erodes the purchasing power of your dollars.

If your home value stays flat while inflation rises, your equity effectively loses value over time.

A California HELOC allows you to tap into that value without selling your home.

By accessing a line of credit, you can pivot that equity into assets that generate actual cash flow.

Defining the California HELOC

HELOC (Home Equity Line of Credit): A revolving credit line secured by your primary residence that allows you to borrow, repay, and borrow again.

This financial tool functions similarly to a credit card but with significantly lower interest rates.

You only pay interest on the amount you actually use.

Explore how this differs from a traditional loan where you receive a lump sum and pay interest on the total balance from day one.

What Your Bank Doesn't Tell You About Your Mortgage Rate

If you bought or refinanced your home a few years ago, you likely have an interest rate below 4%.

Your bank knows this.

When you ask for cash, they often suggest a cash-out refinance.

A cash-out refinance replaces your entire mortgage with a new, larger loan at current market rates.

This means you would give up your 3% interest rate on your entire balance just to get some cash out.

A savvy Florida HELOC strategy allows you to keep your low-rate first mortgage exactly where it is.

You simply add a second line of credit on top.

This protects your primary low-interest debt while giving you the liquidity you need.

The Hidden Power of the Draw Period

Most HELOCs come with a 10-year draw period.

During this time, you usually have the option to make interest-only payments.

This keeps your monthly overhead extremely low while you use the funds for investments.

Banks don't always highlight this because they prefer you to pay down principal immediately.

For a real estate investor in Virginia or Michigan, interest-only payments are a game-changer for maintaining positive cash flow on a new rental acquisition.

Regional Insights: From California to Georgia

Equity strategies vary depending on where you live.

In high-value markets, a California HELOC can unlock hundreds of thousands of dollars.

In Georgia, working with a Georgia HELOC lender can help you capitalize on the lower property taxes and growing rental demand in suburban Atlanta.

Homeowners in Illinois and Indiana often use equity to fund renovations that significantly increase property value before a sale.

Regardless of your state: whether it is Alabama, Arkansas, Kentucky, or Missouri: the core principle remains the same.

Accessing equity creates options.

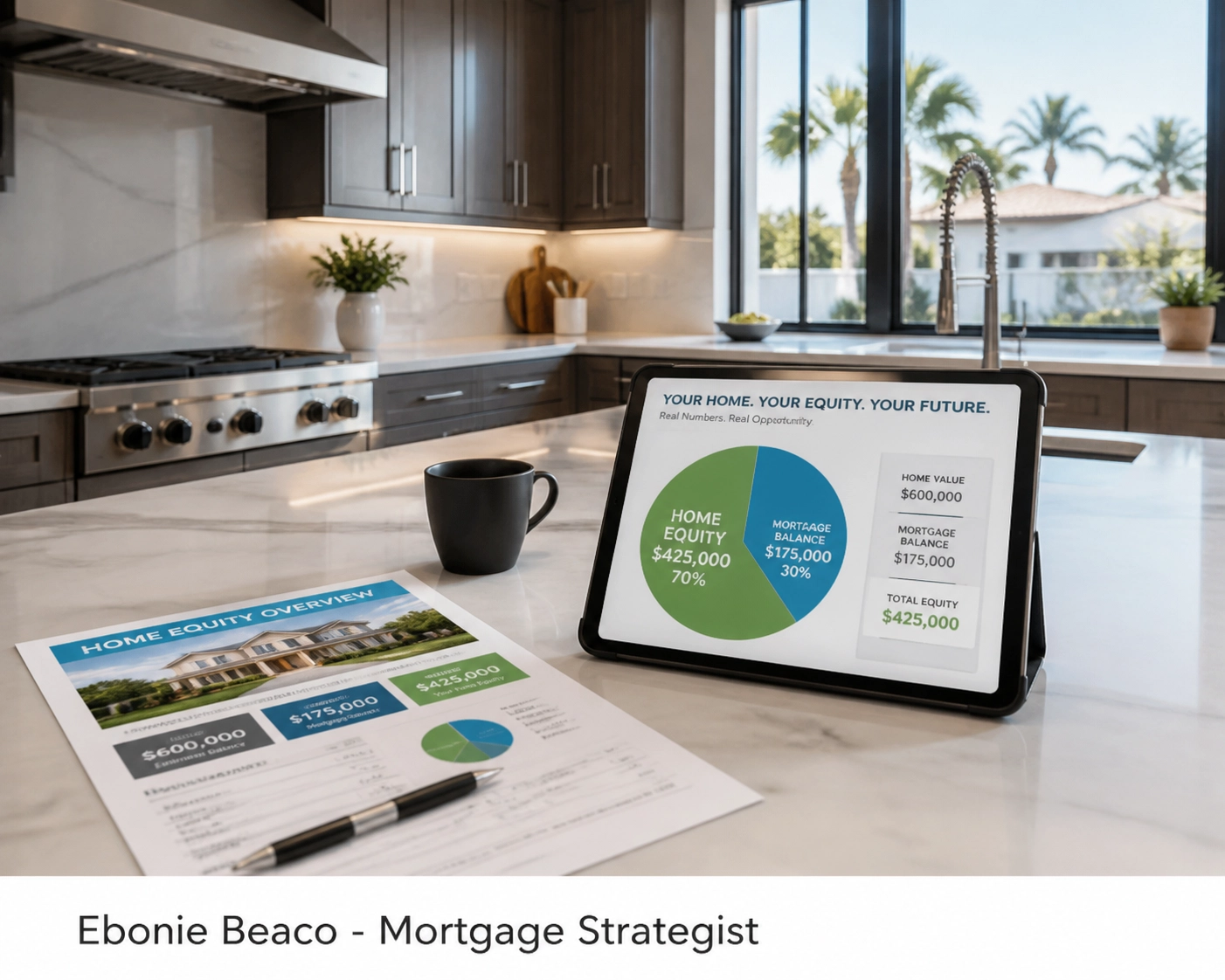

A Real-World Equity Calculation

Let's look at how the math actually works for a homeowner in a mid-to-high value market.

Imagine your home is worth $750,000.

You currently owe $400,000 on your first mortgage.

Most lenders allow you to access up to 80% or 85% of your total home value.

Calculation Breakdown:

- Property Value: $750,000

- Max Loan-to-Value (80%): $600,000

- Existing Mortgage: $400,000

- Available Equity Line: $200,000

In this scenario, you have a $200,000 safety net or investment fund ready to go.

You don't pay a dime in interest until you actually move money out of that line.

Using HELOCs for Real Estate Investment Strategy

Smart investors use their homes as a "funding machine."

Instead of saving for years to buy a rental property, they use a Florida HELOC to cover the down payment on a new investment.

DSCR (Debt Service Coverage Ratio) Loan: A mortgage for investment properties where qualification is based on the property’s rental income rather than the borrower’s personal income.

You can use your HELOC to buy a property, renovate it, and then use a DSCR loan to refinance and pay back your HELOC.

This is a classic version of the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat).

It allows you to scale a portfolio using the equity you already have.

Common Obstacles: DTI and Credit Scores

DTI (Debt-to-Income Ratio): The percentage of your gross monthly income that goes toward paying debts.

Banks often use strict DTI requirements to limit who can access a HELOC.

They want to ensure you can handle the payments if rates rise.

If your bank says no due to DTI, don't assume the door is closed.

Different lenders have different "appetites" for risk.

Some focus more on the equity in the home than your monthly paycheck, especially for self-employed borrowers or investors.

The Rate Trap: Variable vs. Fixed

Almost all HELOCs have variable interest rates.

This means your payment can change based on the prime rate.

Banks love variable rates because they shift the risk of rising interest rates onto you.

However, many HELOC programs now offer a "fixed-rate lock" option.

This allows you to take a portion of your balance and lock it into a fixed rate for a set period.

Compare these options carefully before signing.

Accessing a fixed-rate segment within a variable line of credit offers the best of both worlds: flexibility and stability.

Why Your Bank Might "Freeze" Your Line

Here is a secret they definitely won't tell you: banks can freeze your HELOC.

If the housing market in your area takes a significant dip, the bank may decide your home is no longer worth enough to secure the line.

They can stop you from taking further draws.

This is why it is critical to have your line of credit established before you actually need the money.

In a shifting economy, liquidity is king.

The "Investment Funding Machine" Checklist

If you are looking to turn your home into an investment tool, follow these steps:

- Check your equity: Use mortgage calculators to estimate your available cushion.

- Verify your credit: A higher score usually unlocks better rates and higher LTV limits.

- Identify your goal: Are you consolidating debt, renovating, or buying a rental?

- Shop local and national: A Georgia HELOC lender might have different terms than a big national bank.

- Review the fine print: Look for annual fees, inactivity fees, or early closure penalties.

Accessing your equity should feel like a strategic move, not a desperate one.

When done correctly, it is one of the fastest ways to increase your net worth without needing a massive salary increase.

Understanding the Closing Costs

Many people avoid HELOCs because they assume the closing costs are as high as a primary mortgage.

This is a common misconception.

In many cases, HELOC closing costs are minimal.

Some lenders even offer "no-cost" HELOCs where they cover the appraisal and title fees.

You should always ask for a full breakdown of fees before moving forward.

Transparency is the foundation of a good lending relationship.

Moving Forward With Confidence

Navigating the world of home equity doesn't have to be intimidating.

Whether you are looking for a California HELOC to fund a tech startup or a Florida HELOC to buy a vacation rental, the strategies remain consistent.

The goal is to move from being a "homeowner" to a "wealth builder."

You have worked hard to pay your mortgage every month; it is time for your home to start working for you.

If you have questions about how much equity you can realistically access or how to structure a deal for an investment property, let's talk.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664

The Silent Threat to Your Equity

There is one more thing your bank is hoping you don't notice.

As the draw period nears its end, your monthly payment is about to undergo a massive transformation.

If you have only been paying interest for ten years, the shift to a fully amortized principal and interest payment can be a "payment shock" that catches thousands of homeowners off guard every year.

What happens if the market shifts right as your repayment period begins?

The answer could be the difference between financial freedom and a forced sale.

Stay tuned for our next deep dive into the "HELOC Reset" and how to survive the end of your draw period.