California & Florida HELOC Secrets Revealed: What Your Big Bank Doesn't Want You to Know

The Secret Home Equity Drain: Why Big Banks Keep Your Cash Locked Up

You have worked hard to build equity in your home. Whether you are sitting on a bungalow in Tampa or a modern masterpiece in San Diego, that equity represents your financial freedom. However, if you have walked into a big retail bank lately, you might have noticed they aren't exactly eager to help you tap into it quickly or flexibly.

Big banks prefer you to take out a high-interest personal loan or a restrictive second mortgage that benefits their bottom line. They rarely highlight the true flexibility of a Home Equity Line of Credit (HELOC). At Home Loans Network, we believe in transparency. We want you to understand how to leverage your property in states like California, Florida, Georgia, and beyond without the red tape.

Accessing your equity shouldn't feel like an interrogation. Explore how a California HELOC or a Florida HELOC functions as a reusable credit limit, allowing you to draw funds, pay them back, and draw them again as needed.

Decoding the HELOC: A Modern Financial Tool

A Home Equity Line of Credit (HELOC) is a revolving line of credit secured by your primary residence, second home, or even an investment property. Think of it like a credit card with a much lower interest rate, where your house serves as the collateral.

Combined Loan-to-Value (CLTV): The ratio of all loans on a property compared to its appraised value. Practical Application: Lenders use this to determine how much total debt they will allow against your home.

Draw Period: The timeframe, typically 10 years, during which you can withdraw funds from your line of credit. Practical Application: You only pay interest on what you actually use during this phase.

The California HELOC: High Values and Wholesale Advantages

In California, property values have reached historic levels. This creates a massive opportunity for homeowners in Los Angeles, San Francisco, and San Diego to access significant capital. However, many retail banks in California have strict "overlays" or extra rules that make qualifying difficult.

A California HELOC through a wholesale lender often provides more breathing room. While big banks might cap your credit limit at a lower amount, wholesale channels can offer jumbo HELOC programs reaching $500,000 to $1 million or more.

If you are self-employed in the Golden State, you likely take substantial business deductions. Standard banks might decline you based on your tax returns. A transparent mortgage strategist can often use bank statement loans or alternative documentation to prove your ability to repay, focusing on your actual cash flow rather than just the bottom line on your 1040.

The Florida HELOC: Navigating Insurance and Property Types

Florida’s real estate market moves fast. From Miami to Orlando and up to Jacksonville, homeowners are looking for ways to fund renovations or prepare for the next investment.

A Florida HELOC comes with its own set of nuances, particularly regarding property insurance and condo approvals. Many big banks shy away from high-rise condos or properties in certain flood zones. Working with a specialist who understands the Florida market helps you navigate these hurdles.

Investors in Florida also use HELOCs to execute the BRRRR method (Buy, Rehab, Rent, Refinance, Repeat). By using a HELOC on their primary residence, they can make "cash" offers on distressed properties, renovate them, and then move into a long-term DSCR rental property loan once the property is leased.

Beyond the Coasts: Georgia, Illinois, and the Midwest

While California and Florida get a lot of headlines, equity strategies are just as potent in the South and Midwest. If you are looking for a Georgia HELOC lender, you are likely seeing the growth in Atlanta and Savannah.

In states like Illinois (specifically the Chicago metro area), Michigan, Indiana, and Missouri, property owners are using HELOCs to combat rising costs or to fund small multifamily acquisitions. Whether you are in Virginia, Alabama, Arkansas, or Kentucky, the mechanics of equity remain a powerful lever for wealth building.

Jump in and compare how these regions differ in terms of appraisal requirements and local lending limits. You can check our mortgage basics page for a deeper dive into regional standards.

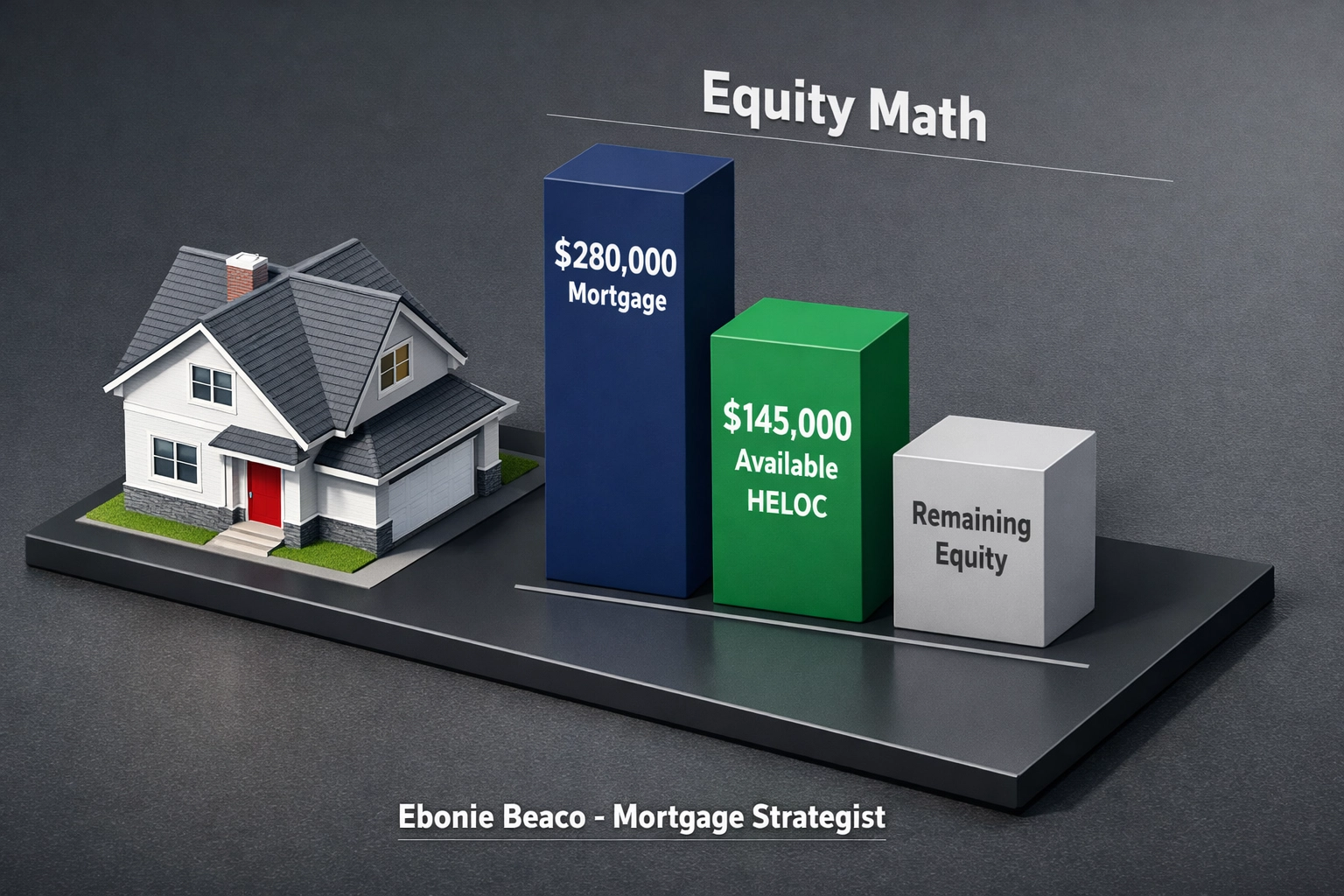

The Math Behind the Money: A Real-World Scenario

To understand how much you can actually get, you have to look at the numbers. Let’s look at a typical scenario for a homeowner in a mid-to-high value market.

Scenario: The Equity Extraction

- Property Value: $500,000

- Current Mortgage Balance: $280,000

- Max CLTV Allowed: 85%

The Calculation:

- Total Allowable Debt: $500,000 x 0.85 = $425,000

- Available HELOC Limit: $425,000 - $280,000 = $145,000

In this example, the homeowner can access $145,000 in available credit. This money can be used for kitchen remodels, debt consolidation, or a down payment on a second home in Virginia or a rental property in Alabama.

Qualification Secrets: What You Need to Know

Big banks often imply that you need perfect credit and a tiny debt load to qualify. That isn't always the case. Here is the reality of the current market:

- Credit Score: While a 740+ gets you the best rates, many programs allow for a minimum credit score of 620.

- Debt-to-Income (DTI): Most lenders look for 43% or less, but some flexible programs go up to 50%.

- Equity: You generally need to keep 15-20% equity in the home (meaning an 80-85% CLTV).

- Appraisals: Sometimes a full interior appraisal is required, but many modern HELOCs use an AVM (Automated Valuation Model) to save you time and money.

Access our online forms to see where your current profile stands.

Using a HELOC for Real Estate Investment

Investors are the primary users of the "HELOC-as-a-Deposit" strategy. If you are an Airbnb host or a landlord, a HELOC is your "opportunity fund."

Imagine a distressed property hits the market in Indianapolis or St. Louis. If you have to wait 45 days for a traditional loan, you lose the deal. If you have a HELOC already in place on your primary home, you can write a check tomorrow. Once the property is stabilized, you can transition into a fix and flip loan or a long-term landlord loan.

This strategy is especially popular among DSCR (Debt Service Coverage Ratio) investors. These loans qualify you based on the property's income rather than your personal tax returns. Using a HELOC to bridge the gap between purchase and permanent financing is a hallmark of a sophisticated investor.

Wholesale vs. Retail: The Difference is Clear

When you go to a big retail bank, you are offered one set of products. If you don't fit their specific box, you get a "no."

Working with a mortgage strategist at Home Loans Network gives you access to a wholesale network. This means we can shop your scenario across multiple lenders to find the one that has the highest CLTV, the lowest rates, or the most flexible income requirements for your specific state, be it California, Florida, or Georgia.

We maintain a transparent approach because we want you to be a client for life, not just for one transaction. You can read what others have experienced on our testimonials page.

Frequently Asked Questions

Can I get a HELOC on an investment property? Yes, though the CLTV is usually lower (around 70-75%) and the interest rate may be slightly higher than a primary residence.

How long does the process take? While a big bank might take 45-60 days, a streamlined wholesale process can often get you from application to funding in as little as 2 to 3 weeks.

Is the interest tax-deductible? According to current IRS rules, interest on a HELOC is generally only deductible if the funds are used to buy, build, or substantially improve the home that secures the loan. Always consult a tax professional.

Taking the Next Step

Your home is more than just a place to sleep; it is a financial engine. Whether you are looking to renovate, consolidate high-interest debt, or expand your real estate portfolio across the Midwest or the Sunbelt, a HELOC is one of the most versatile tools at your disposal.

Don't let your equity sit idle while the big banks profit from your inertia. Explore your options, compare the numbers, and take control of your financial trajectory.

Scedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

But wait... there is one specific trap that many homeowners fall into during the first 12 months of their HELOC that can cost thousands in unnecessary interest. Most banks won't mention it until it's too late. Do you know how to avoid the "First-Year Float" trap? We will be diving into that in our next update...