California, Florida, and Illinois Mortgage Updates: Your 4:00 PM Daily News Recap

Welcome to your daily mortgage market summary for Sunday, June 7, 2026. As we enter the second week of June, the national housing landscape continues to stabilize following a period of geopolitical volatility earlier this year. Investors and homeowners in California, Florida, and Illinois are closely monitoring how the modest easing of mortgage rates is impacting inventory levels and purchasing power. This daily recap provides the essential data and strategic insights you need to navigate the current lending environment across our primary service states.

National Mortgage Rate Snapshot for June 2026

The national average for a 30-year fixed-rate mortgage currently sits near 6.48 percent as of this afternoon. This represents a significant shift from the higher peaks seen in late 2025, providing a slightly more favorable window for those considering a cash out refinance or a new purchase. While the path downward has been choppy due to international events, the overall trend reflects a more balanced market than we experienced two years ago. Borrowers with strong credit profiles are finding opportunities to lock in rates in the low 6 percent range, particularly when exploring conventional loan products.

Lenders are seeing increased activity in the Non-QM mortgage loan sector as self-employed borrowers and investors seek flexible alternatives to traditional financing. These programs are proving essential in markets like Georgia and Virginia, where entrepreneurial growth remains strong. By leveraging bank statement loans, many business owners are qualifying for home purchases without the traditional W-2 documentation. The current stability in the secondary market, supported by targeted federal purchases of mortgage-backed securities, is helping to keep these specialized rates competitive.

California Real Estate Dynamics and High-Balance Strategies

California markets continue to lead the nation in property value retention despite the broader national shifts in borrowing costs. As of today, the average 30-year fixed APR in California is hovering around 6.39 percent for well-qualified buyers. This slight edge over the national average is partly due to the high volume of jumbo loans and high-balance conventional financing occurring across the state. From the Bay Area down to San Diego, inventory has seen a modest uptick, giving buyers more room for negotiation than they have had in several seasons.

For California homeowners, the focus has shifted toward tapping into significant levels of equity that have built up over the last decade. Many are utilizing a HELOC (Home Equity Line Of Credit) to fund renovations or to provide the down payment for an investment property in more affordable markets like Arkansas or Missouri. This strategy allows owners to keep their existing low-rate first mortgage while accessing capital for expansion. The commitment to maintaining high property values remains a central theme for those looking to build long-term wealth through California real estate.

You can explore more about these specific state programs on our loan programs page to see how they align with your current financial goals. Understanding the nuances of California's high-cost limits is vital for anyone looking to maximize their leverage in today's environment.

Florida and the Southeast: Short-Term Rental and DSCR Opportunities

In Florida and Georgia, the narrative remains focused on investment potential and the robust demand for short-term rental properties. While standard 30-year fixed rates in Florida are clustering near the national mid-6 percent band, the real activity is in the DSCR investor loan space. These loans allow investors to qualify based on the property’s rental income rather than their personal debt-to-income ratio. This is a game-changer for individuals looking to scale their portfolios in high-demand vacation destinations like Orlando, Miami, or the Gulf Coast.

The market for Airbnb and short-term rentals in Florida has matured, with lenders offering specialized products that account for the seasonal nature of rental income. Strategic investors are also looking at bridge loans to acquire properties that need minor cosmetic updates before they are ready for the rental market. By using short-term financing to secure the deal, they can later transition into a long-term DSCR loan once the property is stabilized and producing consistent cash flow. This proactive approach is currently very popular in the rapidly growing markets of Alabama and Kentucky as well.

Illinois and Midwest Market Resilience

The Illinois market, particularly the Chicago metropolitan area, shows remarkable resilience and a steady demand for multi-family housing. Unlike the more volatile coastal markets, Chicago offers a diverse range of investment opportunities from two-unit "flats" to larger apartment complexes. Current rates for 30-year fixed loans in Illinois are tracking closely with national averages, making it an attractive time for those looking to enter the market. The availability of down payment assistance programs continues to support first-time buyers in urban centers, helping them overcome initial entry barriers.

Investors in the Midwest are frequently utilizing fix and flip loans to revitalize older housing stock in areas like Michigan and Indiana. These short-term interest-only loans provide the necessary capital for both the purchase and the renovation costs. Once the project is complete, the investor can either sell for a profit or use a "refinance to rent" strategy to hold the property as a long-term asset. This cycle of investment is a key driver of neighborhood revitalization and wealth creation across the region.

For detailed information on the Chicago market specifically, you may find the Chicago neighborhoods market reports useful for identifying high-growth corridors.

Strategic Financial Analysis: The DSCR Advantage

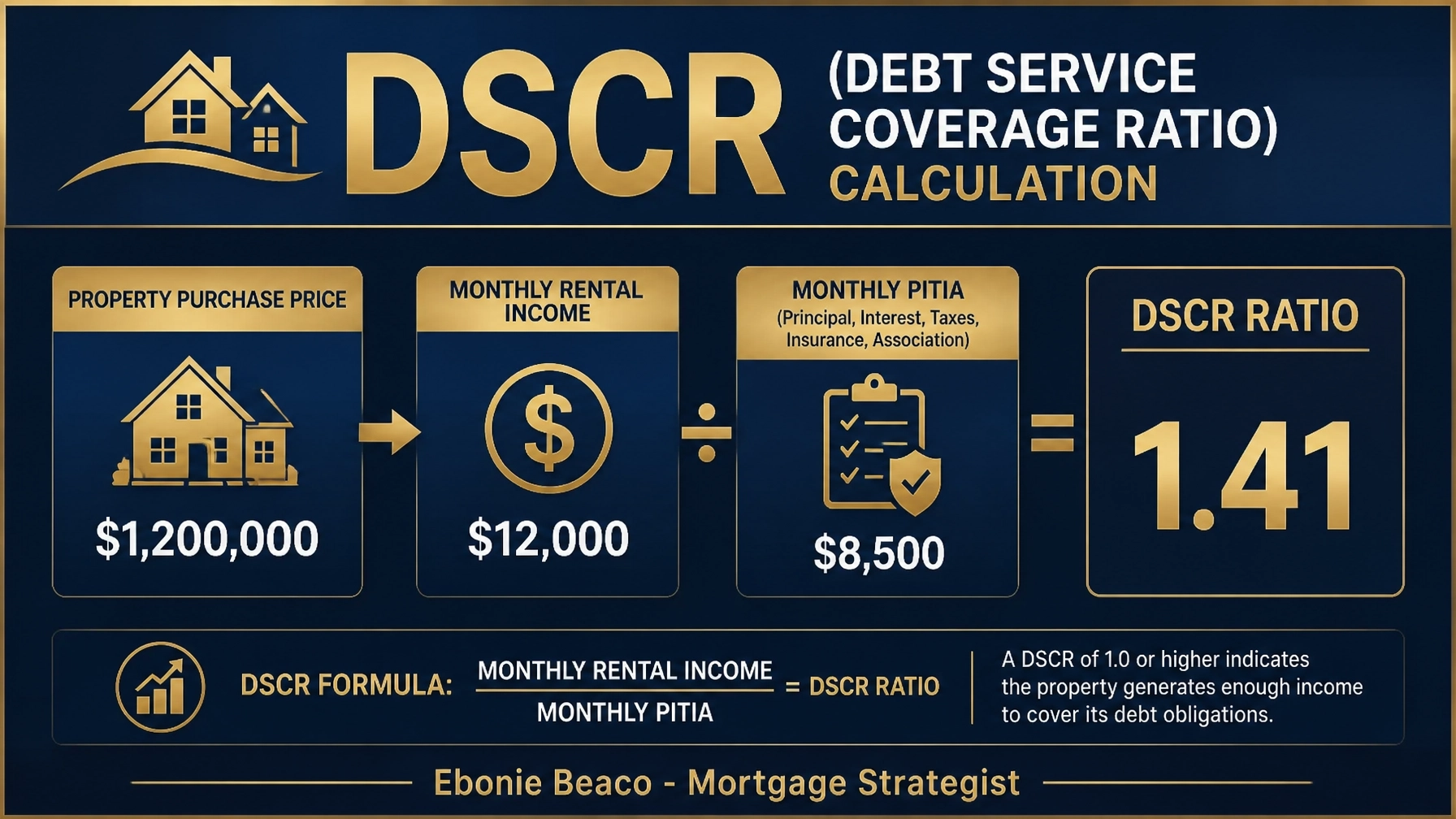

To understand how these financing tools work in a real-world scenario, let us look at a common investment play involving a multi-unit property. Suppose an investor is looking at a four-unit building in a stable Chicago neighborhood. The ability to qualify for financing based on the property's performance rather than personal income is what makes the DSCR investor loan so powerful. Below is a breakdown of how the numbers might look for such a transaction in the current June 2026 market.

Investment Scenario: Chicago 4-Unit Acquisition

- Property Purchase Price: $1,200,000

- Down Payment (25%): $300,000

- Loan Amount: $900,000

- Gross Monthly Rental Income: $12,000

- Monthly PITIA (Principal, Interest, Taxes, Insurance, Association): $8,500

- Debt Service Coverage Ratio (DSCR): 1.41

In this example, the DSCR of 1.41 indicates that the property generates 41 percent more income than is required to cover the monthly debt obligations. Lenders typically look for a ratio of 1.20 or higher, making this an excellent candidate for financing. This surplus cash flow provides a safety net for the investor and demonstrates the viability of the asset.

Essential Technical Definitions for Today's Market

Navigating mortgage news requires a clear understanding of the terminology used by industry professionals. Here are dictionary-style definitions of the key concepts mentioned in today’s recap:

- DSCR (Debt Service Coverage Ratio): A financial metric used by lenders to measure a property's ability to cover its debt payments based on its net operating income. You use this ratio to qualify for investment property loans without using your personal tax returns.

- LTV (Loan-to-Value): The ratio of a loan to the value of an asset purchased, expressed as a percentage. A lower LTV often results in better interest rates and may eliminate the need for private mortgage insurance.

- HELOC (Home Equity Line of Credit): A revolving line of credit that allows homeowners to borrow against the equity in their home as needed. This functions similarly to a credit card but uses your home as collateral, often providing lower interest rates for major expenses.

- Non-QM Loan: A mortgage that does not meet the "qualified mortgage" guidelines set by federal agencies, often used for self-employed or high-net-worth individuals. These loans provide flexibility for borrowers with unique financial situations who do not fit into the standard lending box.

- Bridge Loan: A short-term loan used until a person or company secures permanent financing or removes an existing obligation. Investors use bridge loans to close quickly on a new property before they have sold their current one.

Market Trends to Watch This Week

As we move through the rest of June, watch for the latest inflation data releases, as these will directly influence the Federal Reserve's stance on long-term rates. While the housing inventory is improving, it remains lower than historical norms in states like Virginia and Missouri. This supply-demand imbalance continues to support property values, even as borrowing costs remain elevated compared to the previous decade.

The shift toward professionalized real estate investing is also a trend to follow. More individuals are transitioning from being casual landlords to operating structured real estate businesses using landlord loans and sophisticated portfolio strategies. Whether you are looking at your first home in Arkansas or your tenth rental in California, staying informed on these daily shifts is the best way to ensure your financing strategy aligns with the broader market reality.

If you are ready to explore how these updates impact your specific situation, jump in and compare your options today. We guide you clearly and confidently through every stage of the process to ensure your financing matches your long-term wealth goals.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco

Mortgage Strategist | Senior Loan Officer

Home Loans Network powered by Loan Factory Inc.

NMLS #2389954

HomeLoansNetwork.com

312-392-0664