Calculating ARV for a Fix and Flip: Illinois Edition

If you are stepping into the world of real estate investing in Illinois, specifically within the fast paced markets of Chicago, Aurora, or Joliet, you have likely heard the term ARV tossed around constantly. After Repair Value, or ARV, is the North Star for fix and flip investors. It is the estimated market value of a property after all planned renovations and repairs are completed.

Without an accurate ARV, you are essentially flying blind. You might overpay for a distressed property, underestimate the renovation budget, or find yourself stuck with a house that will not appraise for what you need to break even. For landlords and investors looking to scale, understanding this number is the difference between a profitable exit and a financial headache.

Why ARV is the Foundation of Your Flip

In the mortgage lending world, specifically when dealing with fix and flip loans, the ARV is what lenders use to determine how much they are willing to lend you. While a traditional mortgage focuses on the current value of a home, an investor loan looks at the future potential.

If you are looking for mortgage financing, the ARV tells the lender that the collateral (the house) will be worth significantly more than the loan amount once the work is done. It also helps you, the investor, determine your Maximum Allowable Offer (MAO).

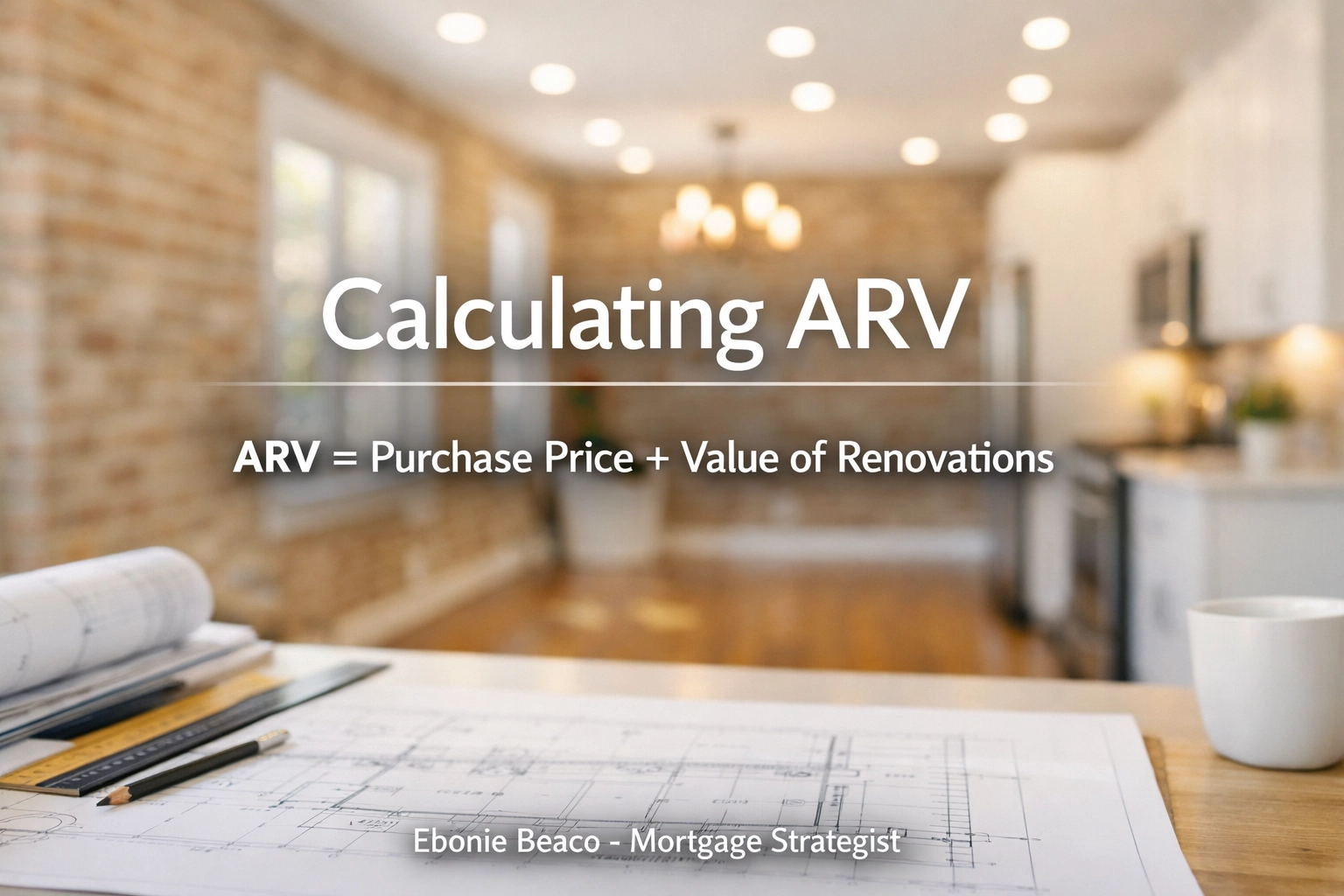

The Core Formula for Success

While there are many variables in real estate, the basic logic of ARV can be distilled into a simple visual equation. When we look at a deal, we are essentially combining what we paid with the value added through our sweat equity and construction.

(Image description: A clean, professional financial graphic with the title 'Calculating ARV'. It displays the formula: 'ARV = Purchase Price + Value of Renovations'. At the bottom, it reads 'Ebonie Beaco - Mortgage Loan Officer'. No money or cash icons are present.)

(Image description: A clean, professional financial graphic with the title 'Calculating ARV'. It displays the formula: 'ARV = Purchase Price + Value of Renovations'. At the bottom, it reads 'Ebonie Beaco - Mortgage Loan Officer'. No money or cash icons are present.)

In the example above, if you purchase a property in a neighborhood like Berwyn for $150,000 and perform renovations that add $100,000 in market value, your ARV is $250,000. It is important to distinguish between the cost of renovations and the value of renovations. Spending $20,000 on a gold plated bathroom might not add $20,000 in value, whereas spending $20,000 on a functional kitchen remodel in a family neighborhood might add $40,000 in value.

Step 1: Analyze the Subject Property

Before you can determine the future value, you must have a crystal clear picture of the current state.

- Square Footage: Is there potential to add a bedroom in the basement or attic?

- Property Type: Is it a single family home, a duplex, or a four unit building?

- Condition: Are we talking about a "lipstick" flip (paint and carpet) or a full "gut" rehab (plumbing, electrical, and structural)?

Investors in Illinois often deal with older housing stock, especially in Chicago. Knowing if you are dealing with a frame house or a brick bungalow changes your renovation costs and your eventual ARV. You can research more about different property types on our site map.

Step 2: Finding True Comparables (Comps)

This is where many new investors trip up. To find the ARV, you need to look at what similar properties have actually sold for in the last 3 to 6 months. Do not look at active listings; look at closed sales.

A "Comp" should meet these criteria:

- Proximity: Ideally within a half mile radius. In dense Chicago neighborhoods, even going two blocks over can put you in a different price bracket.

- Similarity: Compare apples to apples. If your flip is a 3 bedroom ranch, do not use a 5 bedroom colonial as a comp.

- Recency: The Illinois market shifts quickly. Sales from a year ago are not reliable indicators of today's value.

- Condition: Look for properties that have already been renovated. You are looking for the "after" version of your house.

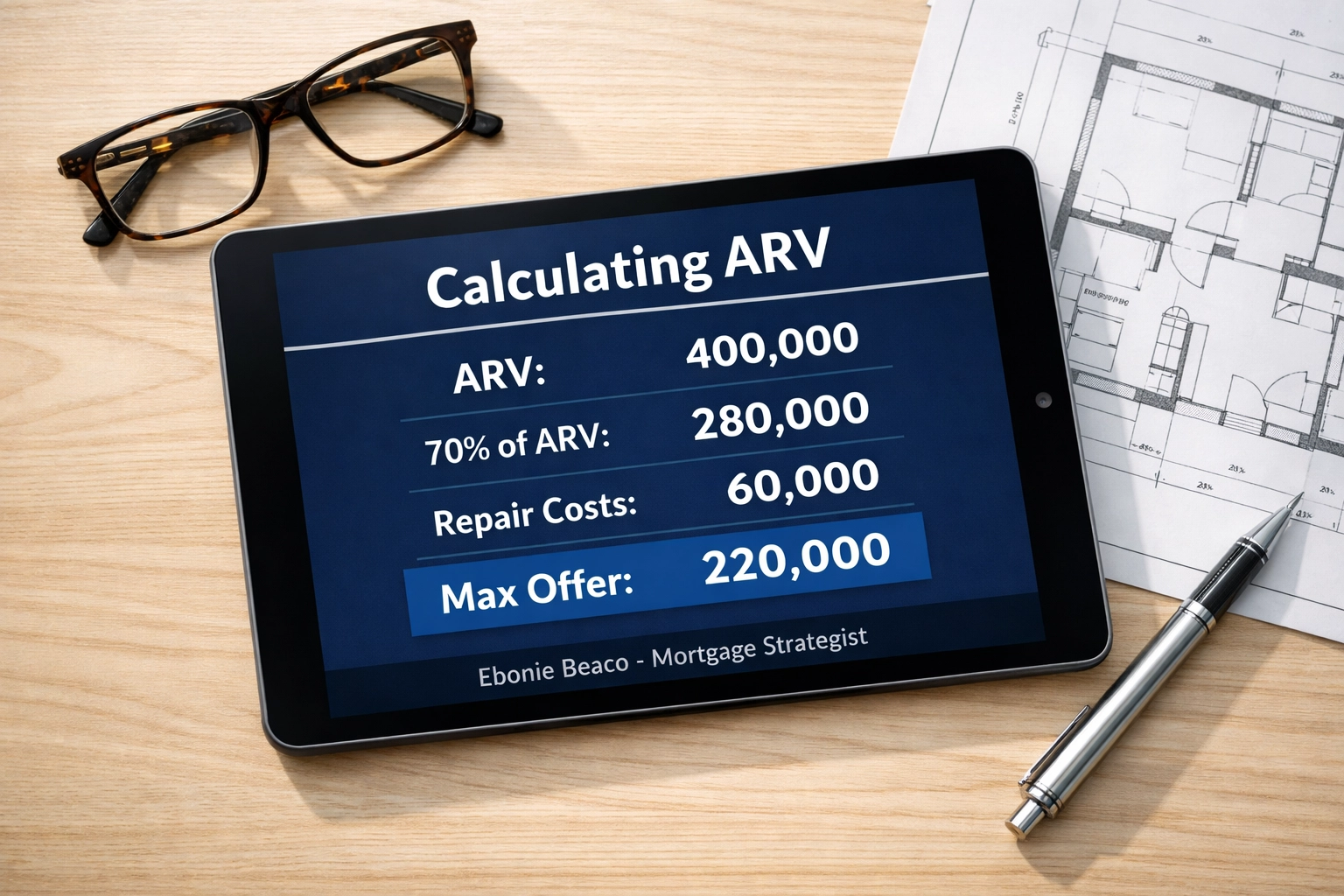

Step 3: The 70% Rule

Once you have your ARV, you need to know what to pay for the property today. Professional flippers often use the 70% Rule. This rule suggests that an investor should pay no more than 70% of the ARV of a property, minus the costs of the repairs.

The Math Breakdown: Let's say you find a distressed property in Naperville.

- Estimated ARV: $400,000

- Estimated Repair Costs: $60,000

- Calculation: ($400,000 x 0.70) - $60,000 = $220,000

In this scenario, $220,000 is your Maximum Allowable Offer. This 30% cushion accounts for your profit, closing costs, holding costs (like taxes and insurance), and the interest on your hard money loan.

(Image description: A financial breakdown chart showing the 70% Rule calculation. ARV: $400,000. 70% of ARV: $280,000. Repair Costs: $60,000. Maximum Allowable Offer: $220,000. Title: Calculating ARV. Bottom: Ebonie Beaco - Mortgage Loan Officer. No money or cash icons are present.)

(Image description: A financial breakdown chart showing the 70% Rule calculation. ARV: $400,000. 70% of ARV: $280,000. Repair Costs: $60,000. Maximum Allowable Offer: $220,000. Title: Calculating ARV. Bottom: Ebonie Beaco - Mortgage Loan Officer. No money or cash icons are present.)

Estimating Illinois Renovation Costs

In Illinois, labor and material costs can vary significantly between the city and the rural outskirts. For a realistic ARV calculation, you must have a solid grasp on local renovation rates.

- Low end rehab: $20 - $35 per square foot (cosmetic updates).

- Medium rehab: $40 - $70 per square foot (kitchens, baths, and some systems).

- High end/Gut rehab: $80+ per square foot (structural changes, full mechanicals).

Accurately predicting these costs is essential because if your repairs go over budget, your profit margin disappears, even if your ARV prediction was spot on. If you are unsure about these numbers, seeking mentoring can save you thousands of dollars on your first few deals.

The Role of Appraisal in ARV

When you apply for fix and flip financing, the lender will order an "As-Is" appraisal and an "After-Repaired" appraisal. The appraiser will look at your scope of work (the list of everything you plan to fix) and compare it to those sold comps we discussed earlier.

Transparency with your lender is key. Providing a detailed line item budget helps the appraiser see the value you are adding. If you plan to install quartz countertops and hardwood floors, make sure that is documented. If you are a landlord looking to transition a property into a long term rental after the flip, you might also look into DSCR investor loans which qualify the property based on its future rental income rather than just your personal income.

Common ARV Mistakes to Avoid

- Ignoring Neighborhood Boundaries: In Chicago, crossing a major street like Western Avenue or North Avenue can change the property value by $50,000 or more. Stay within the immediate pocket.

- Over-improving: Do not put a $60,000 kitchen in a neighborhood where the highest sold house only has a $20,000 kitchen. You will not get that money back in the ARV.

- Using Active Listings: Sellers can ask for whatever they want, but that does not mean they will get it. Only trust the "Sold" data.

- Forgetting Holding Costs: Every month you own the house, you are paying property taxes (which are notably high in Illinois), insurance, and interest. These eat into the 30% margin.

How Financing Fits In

Getting the ARV right allows you to leverage your capital. Many investors use bridge loans to acquire the property quickly and then refinance into a long term landlord loan once the renovation is complete and the new ARV is established. This is a core component of the BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat).

If you are a homeowner with significant equity, you might even consider a HELOC on your primary residence to fund the down payment or the renovation costs of your first flip. This strategy allows you to use your existing assets to build a new stream of income.

Moving Forward with Your Investment

Calculating ARV is a skill that takes practice, local market knowledge, and a bit of intuition. Whether you are looking to flip your first house in Cicero or you are a seasoned landlord expanding your portfolio in Rockford, having a mortgage strategist in your corner can make the process much smoother.

We provide the tools and the funding to help you navigate these calculations with confidence. From Non-QM mortgage loans for self employed investors to specialized fix and flip products, we have the resources to support your growth.

Ready to run the numbers on your next deal? Let’s make sure your ARV and your financing strategy align for maximum profit.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664

Contact Ebonie Beaco for fix and flip funding or mentoring at www.homeloansnetwork.com.