Buying Your First Home with Down Payment Assistance

Saving up for a down payment is often cited as the biggest obstacle for people looking to transition from renting to owning. In high-demand markets like Chicago, Illinois, or the coastal regions of Florida and California, coming up with a 3.5% or 5% down payment on top of closing costs can feel like a mountain that is impossible to climb.

However, many first-time buyers are unaware that there are hundreds of programs designed to bridge this gap. Down payment assistance (DPA) acts as a financial boost, helping you secure a home sooner than you thought possible. Whether you are looking for your primary residence or planning to eventually turn that first home into your first rental property, understanding how these programs function is a critical step in your wealth-building journey.

What is Down Payment Assistance?

Down payment assistance is a generic term for various programs offered by state housing authorities, local governments, and non-profit organizations. These programs provide funds to help eligible homebuyers cover the initial costs of purchasing a home.

Explore the most common forms of these programs:

- Grants: These are funds provided to the buyer that do not have to be repaid. They are essentially a gift from the program to the homeowner.

- Forgivable Loans: These are second mortgages that have a 0% interest rate. The balance is forgiven over a specific period, such as five or seven years, provided you stay in the home.

- Repayable Loans: These act as a second lien on the property. You might have to pay them back monthly or in a lump sum when you sell or refinance the home.

Accessing these funds often requires meeting specific income limits and credit score requirements. For many, these programs are the difference between continuing to rent and finally building equity. You can learn more about the initial steps of the loan process to see how DPA fits into the timeline.

Popular Assistance Programs for 2026

The landscape for home financing is constantly evolving. In 2026, several programs have become mainstays for buyers in states like Michigan, Virginia, and Georgia.

Communities First Down Payment Assistance

This program is highly sought after because it often functions as a grant rather than a loan. It typically provides 3%, 4%, or 5% of the purchase price. A significant benefit here is that income limits are usually based only on the borrower's income, not the entire household. This flexibility allows more families to qualify even if they have a multi-income household.

OHFA Your Choice!

Commonly used in the Midwest, this program allows borrowers to select either 2.5% or 5% of the home's purchase price to be used for down payments or closing costs. While it is a loan, it is often forgiven after seven years if you do not sell or refinance. This is a strategic way to get into a home with very little of your own capital.

FHA 100% Financing Options

Some programs combine a standard FHA first mortgage with a 3.5% second mortgage to cover the entire down payment. This effectively creates 100% financing. For a buyer in a market like Virginia or Indiana, this means the only out-of-pocket costs might be the appraisal and home inspection.

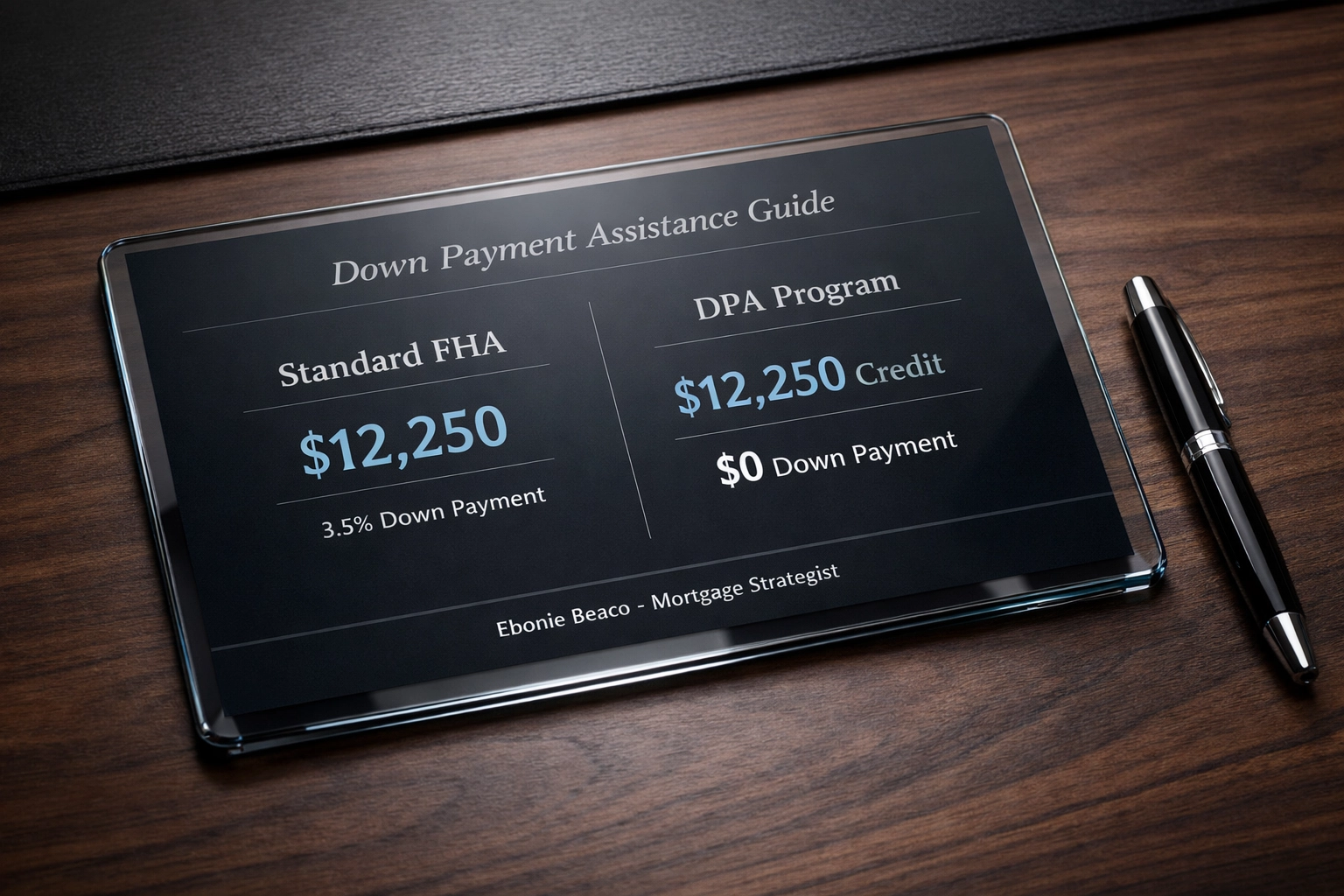

Let’s Look at the Numbers: 3.5% Down vs. Assistance Credit

Visualizing the savings is the best way to understand the impact of DPA. Let’s compare a standard FHA loan purchase against one using a 3.5% assistance grant for a home priced at $350,000.

Standard FHA Purchase:

- Purchase Price: $350,000

- Required Down Payment (3.5%): $12,250

- Total Cash Needed for Down Payment: $12,250

DPA Assisted Purchase:

- Purchase Price: $350,000

- Required Down Payment (3.5%): $12,250

- DPA Credit Applied: $12,250

- Total Cash Needed for Down Payment: $0

(Image Description: A professional financial chart titled "Down Payment Assistance Guide". It displays the calculation: Home Price $350,000. FHA 3.5% Down = $12,250. DPA Credit = -$12,250. Total Out-of-Pocket Down Payment = $0. Bottom text: Ebonie Beaco - Mortgage Loan Officer. No money or cash icons present.)

(Image Description: A professional financial chart titled "Down Payment Assistance Guide". It displays the calculation: Home Price $350,000. FHA 3.5% Down = $12,250. DPA Credit = -$12,250. Total Out-of-Pocket Down Payment = $0. Bottom text: Ebonie Beaco - Mortgage Loan Officer. No money or cash icons present.)

While you may still have closing costs (which can sometimes be covered by seller credits), removing the $12,250 down payment requirement significantly lowers the barrier to entry. For more detailed scenarios, check out our mortgage calculators.

Qualifications and Eligibility

While DPA sounds like a dream, there are rules you must follow to participate. Most programs are geared toward "first-time homebuyers," which usually includes anyone who hasn't owned a primary residence in the last three years.

Jump in and review these common requirements:

- Credit Score: Most FHA-based DPA programs require a minimum credit score of 620.

- Income Limits: Programs are often tied to the Area Median Income (AMI). If you earn too much, you may not qualify for specific grants.

- Homebuyer Education: You will likely need to complete a short online course about the responsibilities of homeownership.

- Primary Residence: You must intend to live in the home. You cannot use these specific programs for a "fix and flip" or an immediate rental property.

If you have questions about your specific situation, visiting the FAQ page can provide quick answers to common eligibility concerns.

Strategic Moves for Future Landlords

Many of the investors I work with in Alabama, Georgia, and Florida started as first-time homebuyers using DPA. This is a strategy known as "house hacking" or the initial phase of a BRRRR strategy.

By using DPA to buy a primary residence (like a duplex or a four-unit building), you can live in one unit and rent out the others. After living there for the required period (usually one to two years), you can move out, keep the property as a rental, and buy your next home.

The beauty of using DPA for your first home is that it preserves your personal savings. Instead of spending $15,000 on a down payment, you can keep that cash in a high-yield account or use it for future property renovations. For those interested in how this scales into larger portfolios, exploring DSCR investor loans for your second or third property is a natural next step once you have established your first home.

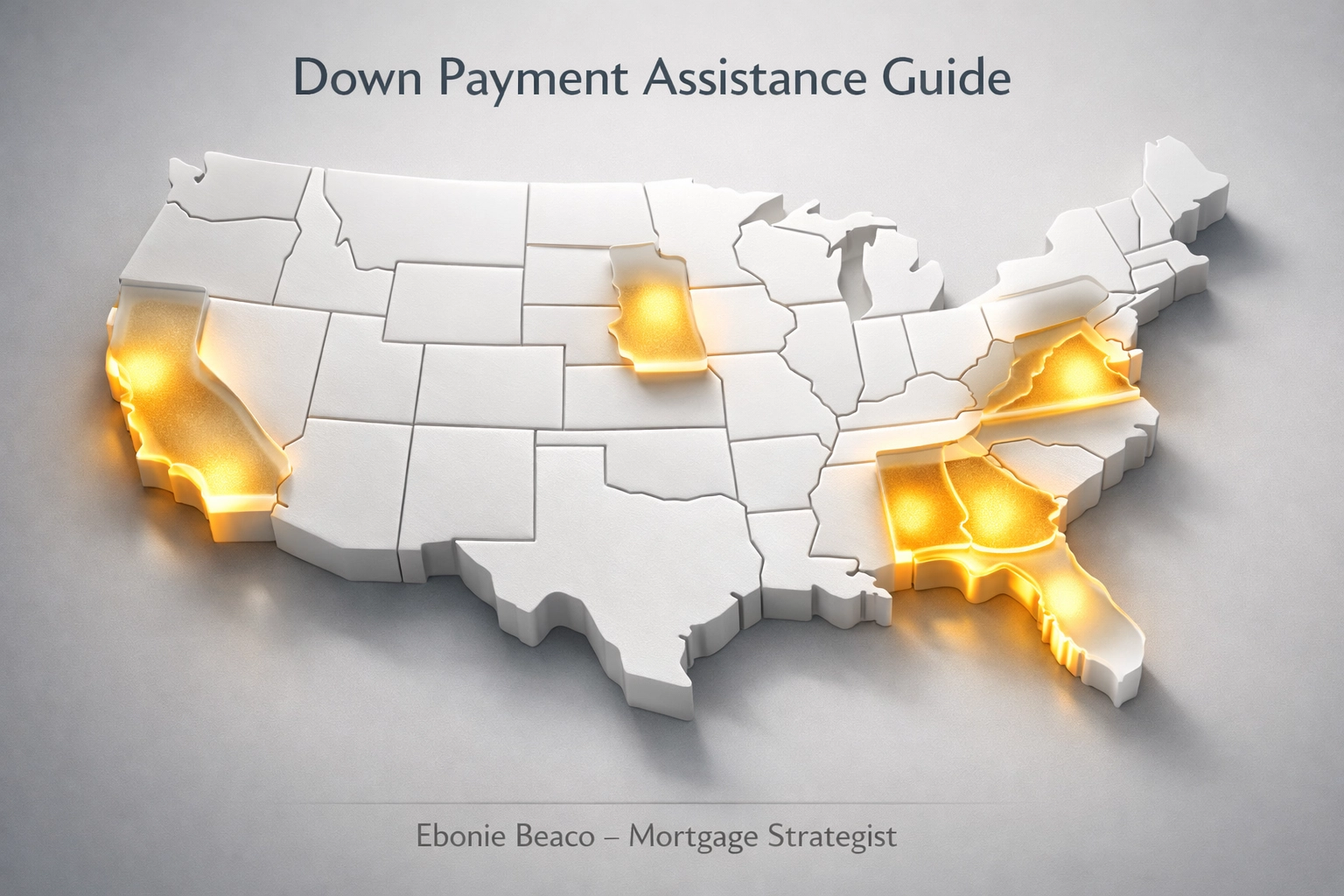

Geographic Opportunities

The availability and amount of assistance vary significantly by location.

- Chicago and Illinois: Various city-specific programs offer generous grants for buyers in targeted neighborhoods to encourage community stabilization.

- Florida: Florida offers several statewide programs that provide thousands of dollars in "silent" second mortgages that help with both down payments and closing costs.

- California: While home prices are higher, California’s assistance programs often offer larger loan amounts to match the market reality.

Whether you are in a bustling metro area or a quiet suburb in Arkansas, there is likely a program that fits your needs. You can research more about regional options on the about us page or by looking through our sitemap.

(Image Description: A clean, educational graphic titled "Down Payment Assistance Guide". It shows a map outline of various states including FL, GA, IL, and CA. Next to the map, text highlights "Available for First-Time Buyers", "Grants & Forgivable Loans", and "Up to 5% Assistance". Bottom text: Ebonie Beaco - Mortgage Loan Officer. No money or cash icons present.)

(Image Description: A clean, educational graphic titled "Down Payment Assistance Guide". It shows a map outline of various states including FL, GA, IL, and CA. Next to the map, text highlights "Available for First-Time Buyers", "Grants & Forgivable Loans", and "Up to 5% Assistance". Bottom text: Ebonie Beaco - Mortgage Loan Officer. No money or cash icons present.)

Closing the Gap

Navigating the world of mortgage financing doesn't have to be overwhelming. The goal is to move you from a position of uncertainty to a position of ownership. By leveraging down payment assistance, you aren't just buying a roof over your head; you are securing an asset that can provide long-term financial stability.

Compare your options and look at the long-term benefits. A small amount of assistance today can lead to significant equity growth over the next few years. If you are ready to see which programs you qualify for, or if you want to discuss how to eventually turn your home into a rental property using landlord loans, I am here to guide you.

Get help with your down payment. Contact Ebonie Beaco to see if you qualify.

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664