Builder Confidence Rises as Rates Dip to 6.05%

It is March 16, 2026, and the pulse of the real estate market is quickening. After a period of "wait and see" from many developers and buyers, we are seeing a distinct shift in sentiment. Mortgage rates have recently dipped to 6.05%, providing a much-needed breath of fresh air for the construction industry and real estate investors alike.

When rates move, the market reacts. This specific drop has pushed builder confidence upward as we move into the spring buying season. According to recent industry reports, low mortgage rates are fueling March home builder optimism, creating a ripple effect across the housing sector. You can explore the full details of this shift via this reference link: PYMNTS - Low Mortgage Rates Fuel March Home Builder Optimism.

As a mortgage strategist, I see this as a pivotal moment. Whether you are looking at a Cash-Out Refinance in Chicago or planning a fix and flip project in Florida, the cost of capital is shifting in your favor. Let’s break down what this move to 6.05% actually means for the landscape of real estate finance.

Understanding the Builder Confidence Index

The NAHB/Wells Fargo Housing Market Index (HMI) is a gauge of builder sentiment. It measures perceptions of current single-family home sales and sales expectations for the next six months.

Housing Market Index (HMI): A weighted average of three separate surveys: present sales, expected sales, and traffic of prospective buyers. Practical Application: When the index rises, it signals that builders are seeing more foot traffic and are more likely to break ground on new projects.

In March 2026, we saw the index tick up to 38. While a score below 50 technically suggests more builders view conditions as poor than good, the upward trajectory is what is catching everyone’s attention. This movement suggests that the "floor" has been established. Builders in markets like Virginia, Georgia, and Michigan are starting to feel more secure in their pipeline projections.

Regional Performance: Where the Growth Is Happening

Not all markets are created equal. The 6.05% rate environment is hitting different regions in unique ways.

- Northeast: Leading the pack with an index of 44. The demand for inventory remains high, and builders are racing to meet it.

- Midwest: Sitting steady at 43. In cities like Chicago and Indianapolis, the stability of the local economy supports steady construction.

- South: Currently at 35. While lower than the North, markets in Alabama, Arkansas, and Florida are seeing a surge in interest for new construction as migration patterns continue to favor warmer climates.

- West: At 31. This region remains the most sensitive to rate fluctuations due to higher entry prices in states like California.

If you are a real estate investor, these numbers guide your strategy. A rising index in the Midwest might signal a good time to look at DSCR rental property loans for new builds, while a lower index in the West could mean more room for negotiating with developers who are eager to move inventory.

(Image Description: A clean financial bar chart showing regional builder confidence scores. Northeast: 44, Midwest: 43, South: 35, West: 31. Text overlay: "Builder Confidence Rises with Rate Dips" at the top and "Ebonie Beaco - Mortgage Strategist" at the bottom. No money shown.)

(Image Description: A clean financial bar chart showing regional builder confidence scores. Northeast: 44, Midwest: 43, South: 35, West: 31. Text overlay: "Builder Confidence Rises with Rate Dips" at the top and "Ebonie Beaco - Mortgage Strategist" at the bottom. No money shown.)

Why 6.05% is the Magic Number for Investors

For a long time, the psychological barrier was 7%. Once we broke below that and headed toward the 6% mark, the math for Real Estate Investors began to change significantly.

When you use a DSCR Investor Loan (Debt Service Coverage Ratio), the lender looks at the property's ability to pay for itself.

DSCR Loan: A financing option for investment properties where qualification is based on the property's rental income rather than the borrower’s personal income. Practical Application: This allows investors to scale their portfolios quickly without hitting the "debt-to-income" ceiling typical of traditional loans.

At a 6.05% interest rate, the monthly debt service is lower. This means more properties now "pencil out." A property that may have had a negative cash flow at 7.5% is now likely hitting a 1.2 or 1.25 DSCR, making it a viable candidate for financing.

Real-World Example: The Chicago Multi-Unit

Imagine you are looking at a 4-unit building in Chicago.

- Purchase Price: $600,000

- Loan Amount (80% LTV): $480,000

- Monthly Rental Income: $6,000

- Estimated Expenses (Taxes, Insurance, Vacancy): $1,500

- Mortgage Payment at 6.05% (Principal & Interest): Approximately $2,893

In this scenario, your total monthly outlay is roughly $4,393. With $6,000 in rent, your net cash flow is $1,607. Your DSCR would be roughly 1.36. This is a very strong profile for a lender. At higher rates, that cash flow shrinks, and the deal becomes harder to justify.

Compare these numbers against your current portfolio to see where you can optimize. You can use our mortgage calculators to run these scenarios for your specific properties.

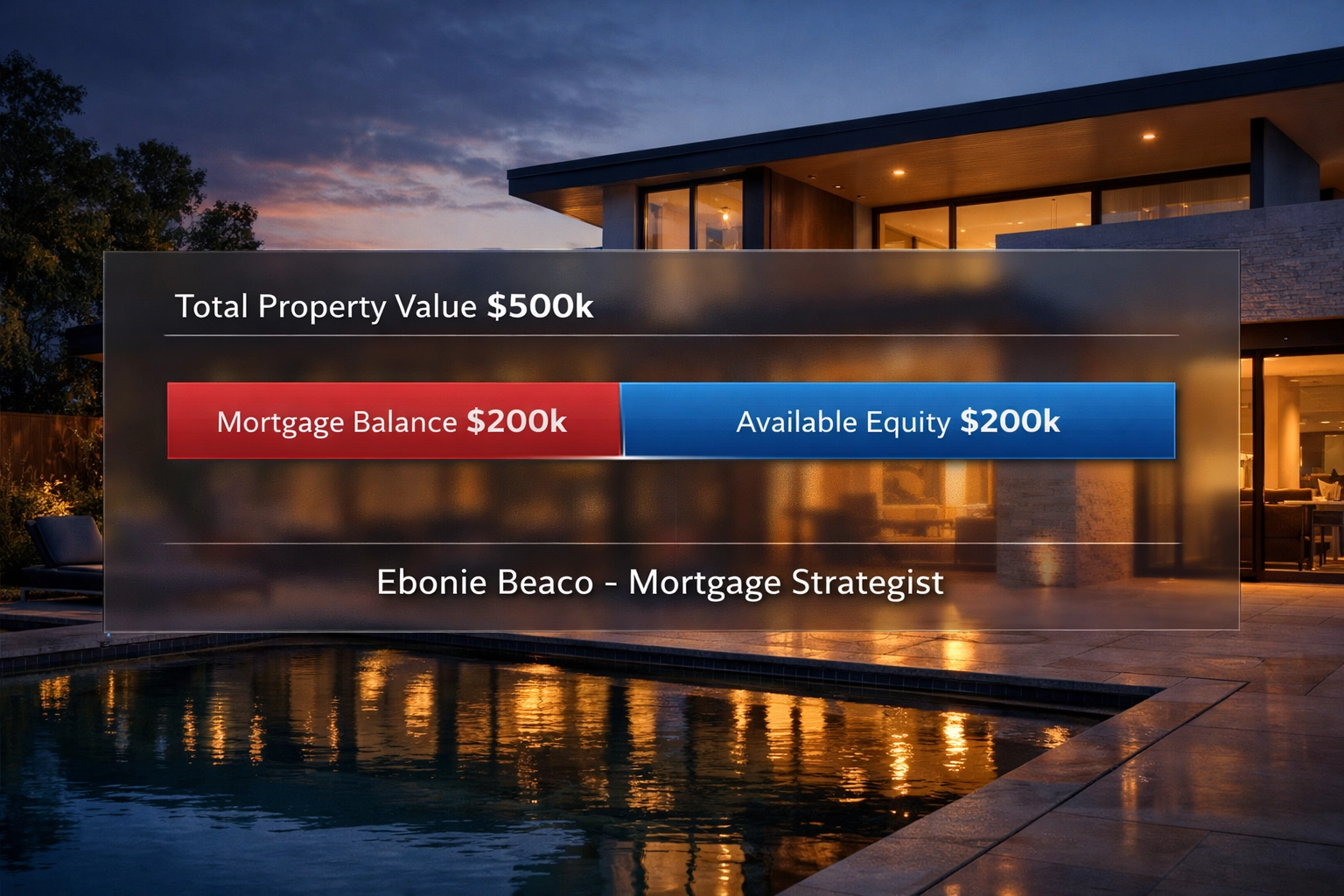

Leveraging Equity: HELOCs and Cash-Out Refinancing

Current homeowners are also watching these rate dips closely. If you bought your home years ago or have seen significant appreciation in markets like Virginia or Georgia, you are likely sitting on a mountain of equity.

Cash-Out Refinance: Replacing your existing mortgage with a new one for a larger amount than you owe and taking the difference in cash. Practical Application: Many investors use this to pull "dead equity" out of a primary residence to use as a down payment on a rental property.

HELOC (Home Equity Line of Credit): A revolving line of credit that allows you to borrow against the equity in your home as needed. Practical Application: Ideal for Fix and Flip investors who need quick access to funds for renovations without refinancing their entire primary mortgage.

With rates at 6.05%, the cost of accessing that equity is becoming more attractive. Instead of keeping your money locked in the walls of your house, you can Access it to fuel your next investment.

(Image Description: A graphic showing an equity extraction calculation. Total Value: $500,000. Existing Mortgage: $200,000. Available Equity for Cash-Out (at 80% LTV): $200,000. Text overlay: "Builder Confidence Rises with Rate Dips" at the top and "Ebonie Beaco - Mortgage Strategist" at the bottom.)

(Image Description: A graphic showing an equity extraction calculation. Total Value: $500,000. Existing Mortgage: $200,000. Available Equity for Cash-Out (at 80% LTV): $200,000. Text overlay: "Builder Confidence Rises with Rate Dips" at the top and "Ebonie Beaco - Mortgage Strategist" at the bottom.)

Strategies for the Fix and Flip Investor

Builders are feeling better, but the inventory of existing homes is still relatively low. This creates a massive opportunity for the Fix and Flip community.

In states like Michigan and Indiana, there are plenty of properties that need a little love to reach their full market potential. When mortgage rates dip, the end-buyer (the person who will eventually buy your flipped house) has more purchasing power.

Bridge Loan: Short-term financing used until a person or company secures permanent financing or removes an existing obligation. Practical Application: Used by flippers to buy a property quickly, renovate it, and sell it before the short-term loan matures.

Non-QM Mortgage: A loan that doesn't fit the strict criteria of Fannie Mae or Freddie Mac, often used by self-employed borrowers or those with unique financial situations. Practical Application: Great for wholesalers or full-time investors who don't have a traditional W-2.

If you are working in the Airbnb and Short-Term Rental space, particularly in vacation hubs in Florida, the 6.05% rate environment makes the "buy and hold" or "BRRRR" strategy much more effective. You can find more about these specific options on our loan programs page.

The Importance of Transparency in Today’s Market

At Home Loans Network, we believe in being fully transparent about the market. While builder confidence is rising, there are still challenges. Labor shortages and the cost of materials remain high. This is why having a Mortgage Strategist in your corner is vital. We don't just give you a rate; we help you structure a deal that accounts for the "real world" variables of construction and investing.

Whether you are a seasoned landlord or an aspiring investor looking to jump in, understanding the nuances of the loan process is the first step toward success. You can learn the mortgage basics on our website to ensure you are prepared for your next move.

Looking Ahead: What to Watch For

As we move further into 2026, keep a close eye on the following:

- Inventory Levels: Will the rise in builder confidence lead to a significant increase in housing supply?

- Fed Policy: Will the Federal Reserve continue to hold or further lower rates?

- Regional Shifts: Keep watching the Northeast and Midwest for the strongest growth signals.

The current dip to 6.05% is an invitation. It is an invitation to Compare your options, Explore new markets, and Jump in to the opportunities that arise when the cost of borrowing becomes more manageable.

Real estate is a long game. The strategies you implement today: whether it's a DSCR rental property loan in Kentucky or a HELOC in California: will define your financial trajectory for years to come.

(Image Description: A flowchart illustrating the BRRRR strategy: Buy, Rehab, Rent, Refinance, Repeat. Text overlay: "Builder Confidence Rises with Rate Dips" at the top and "Ebonie Beaco - Mortgage Strategist" at the bottom.)

(Image Description: A flowchart illustrating the BRRRR strategy: Buy, Rehab, Rent, Refinance, Repeat. Text overlay: "Builder Confidence Rises with Rate Dips" at the top and "Ebonie Beaco - Mortgage Strategist" at the bottom.)

If you have questions about how these rate changes affect your specific portfolio or your plans to purchase a home, don't stay in the dark. We have an extensive FAQ section that covers everything from credit scores to closing costs.

Ready to see how the math works for your next project?

Schedule a 1 on 1 at https://calendly.com/homeloansnetwork

Ebonie Beaco Mortgage Strategist | Senior Loan Officer Home Loans Network powered by Loan Factory Inc. NMLS #2389954 HomeLoansNetwork.com 312-392-0664